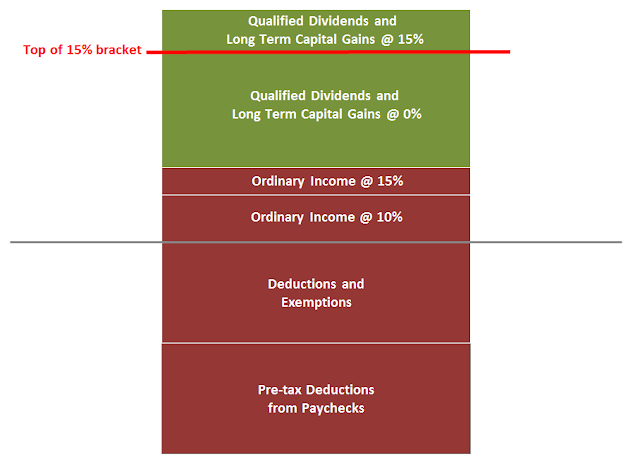

I wrote about tax-free capital gains when you are in the 15% tax bracket or lower. I created this chart to make it clearer what I’m talking about (click on the chart for a larger size).

Your gross income first goes toward the pre-tax deductions from your paychecks (401k, health care insurance premiums, flexible spending accounts). Then it fills the deductions (at least $6,100 single, $12,200 married filing jointly in 2013) and exemptions ($3,900 per person including dependents in 2013). Only the income above the gray line is taxable.

If after subtracting all those, your taxable income doesn’t quite reach the top of 15% bracket (red line in the chart, $36,250 single, $72,500 married filing jointly in 2013), the green block under the red line is your opportunity to realize long term capital gains for free.

It gets more complicated if you are receiving Social Security benefits.

If you don’t have much income outside Social Security, your Social Security benefits are tax free, and you likely won’t pay any tax. As you create more income (for instance by realizing capital gains), a part of your Social Security benefits will be taxed, but at a low rate. As a result, your overall tax rate is still very low. If you realize more gains, more of your Social Security tax will be taxed and at a higher rate. After you pass a hump, the tax rate on additional income drops back down.

Example 1: Jane and David, both 66, married filing jointly, receive $30,000 a year in Social Security benefits. They don’t have any other income or deductions besides their personal exemptions and the standard deduction. If they realize long term capital gains, how will the gains be taxed?

It depends on how much in long term capital gains they will realize. Using the online tax calculator TaxCaster, by increasing the long term capital gains (LTCG) by $1,000 at a time, I get the following results:

| Realized LTCG | Tax | Marginal Rate | Blended Rate |

| $47,000 | $0 | 0% | 0% |

| $52,000 | $423 | 8.5% | 0.8% |

| $64,000 | $423 | 0% | 0.7% |

The first $47,000 in long term capital gains is tax free. The next $5,000 is taxed at 8.5%. The next $12,000 is tax free again.

Altogether, this couple can realize $64,000 in long term capital gains on top of their $30,000 in Social Security benefits and pay only 0.7% in federal income tax on the capital gains. Isn’t that a great deal or what?

The picture changes a little bit when you add other income, for instance retirement account withdrawals.

Example 2: Jackie and Adam, both 71, married filing jointly, receive $30,000 a year in Social Security benefits and $15,000 a year in Required Minimum Distributions (RMD) from their retirement accounts. They don’t have any other deductions besides their personal exemptions and the standard deduction. If they realize long term capital gains, how will the gains be taxed?

By playing with TaxCaster again, I get these:

| Realized LTCG | Tax | Marginal Rate | Blended Rate |

| $14,000 | $0 | 0% | 0% |

| $34,000 | $1,673 | 8.5% | 4.9% |

| $37,000 | $2,034 | 12% | 5.5% |

| $49,000 | $2,034 | 0% | 4.2% |

The first $14,000 in long term capital gains is tax free. The next $20,000 is taxed at 8.5%. The next $3,000 is taxed at 12%. The next $12,000 is tax free again.

Altogether, their RMD will make it more costly for this couple to realize long term capital gains, but they can still realize $49,000 in long term capital gains on top of their $45,000 income from Social Security and retirement accounts, and they will only pay 4.2% in federal income tax on their $49,000 capital gains. 4.2% is not zero, but it’s still very low.

It’s still a great deal if you ask me. If you calculate the effective tax rate on their entire $94,000 income, it’s only 2.2%. A working couple earning $94,000 in wages will pay many times more than that.

The picture changes again when you have higher Social Security benefits and higher income from pension or retirement account withdrawals.

Example 3: Joan and Ben, both 72, married filing jointly, receive $40,000 a year in Social Security benefits and $25,000 a year in Required Minimum Distributions (RMD) from their retirement accounts. They don’t have any other deductions besides their personal exemptions and the standard deduction. If they realize long term capital gains, how will the gains be taxed?

By playing with TaxCaster again, I get these:

| Realized LTCG | Tax | Marginal Rate | Blended Rate |

| $0 | $1,058 | ||

| $7,000 | $1,653 | 8.5% | 8.5% |

| $31,000 | $4,689 | 13% | 12% |

The first $7,000 in long term capital gains is taxed at 8.5%. The next $24,000 is taxed at 13%. Gains over $31,000 will be taxed at the normal 15% rate.

This couple still gets a break on the first $31,000 in long term capital gains but the deal isn’t nearly as good as in Example 1 and Example 2. Although a blended rate of 8.5% or 12% is still better than the normal 15% rate, it may not make sense to pay tax and reset the basis higher now if they intend to hold the assets for a long time or leave the assets to their heirs for the step-up basis.

You will only know which scenario you fall into by playing with your own numbers in a tax calculator or tax software.

Say No To Management Fees

If you are paying an advisor a percentage of your assets, you are paying 5-10x too much. Learn how to find an independent advisor, pay for advice, and only the advice.

Nelz says

I receive a total of $2535 per month from social security and DIC (VA benefit do to death of my spouse). I pay no income tax on either. I would like to start drawing from my IRA and Deferred annuity of which I have approx $500K. between the two.

How do I know how much to draw and what tax bracket I will be in?

Harry says

Nelz – You can use the same tax calculator I used in this post. Try different numbers and see how your taxes change. It’s called TaxCaster.

Klaas says

This doesn’t make sense to me. When additional income starts making Social Security income taxable, it’s at 50% for a while, then 85%. If the other income is capital gains taxed at 0%, then that would make your marginal tax rate 5%, then 8.5%, then 13%, but the 13% (85% of 15%) rate would apply until you hit the 25% bracket, at which point you’d also hit the 15% capital gains bracket and your marginal rate should be 36.25%. I don’t think there’s any provision that causes the taxable amount of Social Security to stop increasing once it starts.

So I think you’ve found a bug in the TaxCaster. The other possibility, of course, is that I’m forgetting about some provision or interaction that makes what you wrote make sense. Can you (or anyone reading) point one out?

Harry says

The taxable amount of Social Security stops increasing when it hits 85% of the Social Security benefits. If there is still room in the 15% tax bracket, additional long-term capital gains are taxed at 0%.

Klaas says

Yup, there it is. Thanks!

Now I need to go back to my SSB spreadsheet and see whether it has a bug or if I just hadn’t seen cases like that because I was running it with ordinary income and higher amounts of Social Security.

Karen says

My mother, on social security, sold her condo this year due to bad health. She is now living with my husband and I. She made $116,000 after fees. Will she need to pay tax on the money from the sale? Does she have a time limit to reinvest the capital? We are looking at purchasing a larger home which she is going to invest all or part of the money from her condo sale.

Harry says

If it was her principal residence in at least 2 of last 5 years she likely won’t need to pay any tax. See IRS Publication 523.

JR says

SSDI 16,000 and sold house with a gain of 5000.

Only lived in house 6 months after buying it. How much tax would I have to pay if any?

ron says

My spouse and I make combined 78,000.00 in pensions and had 47,000.00 in long term capital gain. Paid my LTCG tax already at 15%. Am I to understand that I add 85% of my social security onto the 78,000.00 or add it to the 78,000.00 +47,000.00 to get my taxable income? That would take my whole tax rate up to 25% after already paying the capital gains tax.

Where do itemized deductions come into play? Or don’t they.

If I wasn’t taking SS, I could itemize my deductions and take that 78,000.00 down to 48,000.00. With SS, I have to add my SS benefit onto my 78,000.00 or 78,000.00+47,000 to figure my taxes? And, not be able to use my deductions?

I would be paying 35,000.00 in fed tax, + the capital gains tax I already paid. Why the heck would I want to take my SS in the first place? Please help me figure this out.

Harry says

You add “up to” 85%, not exactly 85%, of your SS to your $78k. You still take the same itemized deductions. If you have enough income already, you can suspend your SS to age 70 for a higher benefit at that time.

M.S. Francis says

We receive less than $30,000 a year in SS payments. We are both 67 and have no other income. My husband and his family have 2 houses remaining in family corporation. Have put one house up for sale for $200,000. His portion will be 17% of sale price. Will we have to pay Capital Gains tax? I

Darlene says

I am having a hard time understanding the taxing of social security benefits upon a capital gain. I just looked at the SSA site and it expressly says it does not take into account investment income, pensions or captial gains in deteriming taxation on Social Security benefits only incurred on annual WAGES EARNED (CAP) WHILE RECEIVING SS and based the amount of SS you receive each month.

Harry Sit says

Capital gains don’t count when they determine the earnings limit (reducing your benefits when you claim early while still working). They count in how much is taxable. The IRS has a whole booklet about it: Publication 915. The easiest way to figure it out would be playing with a tax calculator or software. Increase your capital gains $1,000 at a time and see what happens. See link to TaxCaster in the article under Example 1.

wm dickey says

I received around 12,300 from social security and I am 63 years old. I sold some real estate in 2014 which will add around $30,000 of long term capital gains to my tax return. I am not concerned about the tax associated with this transaction, but wonder if the long term capital gains will cause me to lose some of my social security over the next couple of years?

thanks

bill

Harry Sit says

Just play with the tax calculator TaxCaster to see how much tax you will pay with and without the capital gains.

https://turbotax.intuit.com/tax-tools/calculators/taxcaster/

Also see previous comment if you are working while receiving Social Security.

john says

I have some antiques, including furniture, that may bring me anywhere from $100 to $1,500 up to perhaps $10,000. I only have my Social Security and 2 small pension checks any haven’t had to pay any taxes since I retired. can I sell my items without being taxed, and do I have to report any sales?

jill williams says

i am 71 years old married filed joint, our income 21,000 ,i sold my resident home in 12/30/2014 for $470,000. in 2013 i got areserve morgage loan for $124,000 so, i remodeled my old home build 1969 which cost me $90,000 and i paid off the load $140,000 ,then i bought a new home for $150,000 ,plus many expenses, now left with me about $60,000. i receive ss.and disability benefit for my self . my question ,dose this amount of $60,000 left with me effect on my ss.or my disability benefit. than you.

Carolyn Hieb says

I make roughly 56K per year gross, I am 56, my husband at 54 is on permanent Soc. Security Disability of about 19K per year. I have an LLC with my two brothers (three of us total). My brother wants to see the family farmland 160 acres (this is why we have an LLC). Will doing this wipe out my husbands SSD? Will splitting it into 2 years contract for deed help or hurt?!

Vaughnyb says

Hi I am 49 years old and on permanent disability. I receive 1800 from ss disability and 2200 from private insurance disability. The insurance benefit is untaxable since taxes were taken out as i paid the insurance premium. My question is. I wish to start investing in the stock market with a buy and hold strategy. Will i be subject to the same capital gains tax if i redeem the stock at 64 before i withdraw my ira or should i redeem every two years to completely avoid the capital gains tax? I will be investing 1400 per year in stocks. Thanks

Harry Sit says

Depending on your investment returns, if you sell everything after 15 years, your capital gains can trigger taxes. It’s better to sell every few years and reinvest when your capital gains are still low enough that won’t trigger taxes.

Ruth Brown says

If I received $10378.00 a year from S.S. and $11508.00 from a pension I owned 12 acres of land which my house is on I sell 10 acres keep 2 acres and my house how much would I be taxed on profit of selling land

rebecca binder says

I am on permanant disability. I am divorced and lost the marital home through foreclosure. I had to sell my mineral rights that I inherited when my father died. My disability is $15,000 a year and I have some royalty payments that were about $12,000 last year. I made $80,000 on the sale of my mineral rights and it all went to pay off debt and secure a place to rent for a while. Am I going to have to pay a huge amount of tax on this sale ? I have read this several times and still don’t quite understand it. I am terrified now that I am finally out of debt (and able to live off my disability and the dwindling royalties) that I will once again be in debt. Please help

rebecca binder says

Thank you.

Rebecca Binder

Vaughn says

I am receiving social security disabilty of $1900 per month and have no other taxable income. My question is if i sell a security from a taxable account in less than a year is this short term capital gain simoly added to my ordinary income? I believe my ordinary or taxable income is 50% of my social security disability income and the added short term capital gain, as long as i stay within the 15% tax bracket, i would pay 0% in taxes at the end of the year? Correct me if i am wrong.

So does this mean that if my disability income of $1900 a month x 12=$22800÷50%=$11400 ordinary income, then as long as i stay within the 15% tax bracket including short term capital gains i am liable to pay 0% in taxes at year end?

Vaughn says

Or is it this….t if my disability income of $1900 a month x 12=$22800÷50%=$11400 ordinary income, then as long as i stay under $25,000 (amount untaxed when receiveing social security), including short term capital gains, will i be liable to pay 0% in taxes at year end? Which scenario is correct or neither. I wish to have the short term gains taxed at 0% on a specified amount each year

Harry Sit says

TaxCaster will help you figure out more easily. If you want to calculate it yourself, first figure out how much your Social Security is taxable (50% of SS plus your other income, compared to $25,000 etc.). Suppose it comes out to $10k. Just because it’s taxable doesn’t mean you will actually pay tax on it. You add that $10k to your other income, and you apply exemption, deduction, and the brackets. The 0% tax on capital gains only applies to long-term gains, not short-term gains.

Vaughn says

I calculated it on taxcaster and it says on gross social security income of $22900 plus $10,000 in short term capital gains there is no tax owed. How could this be possible if 0% tax only applies to long term capital gains? Could it be that the $10,000 in short term capital gains is simply added to the ordinary income thus making my ordinary income under the $25000?

Harry Sit says

50% of Social Security plus $10,000 is under $25,000. That makes your Social Security not taxable. $10,000 by itself is below your personal exemption plus standard deduction.

Brenda Gonatas says

I am 64 on early S.S. with my husband the same age. We have one commerical property we bought in 1977 and would like to know what our capital gains tax will be . Our only income is our S.S. payments which total 1335.00 per month. Also will selling this property stop our s.s. payments that we are receiving now. Should we wait or can we sell it now.

Jay says

I’m 66 years old Single filer and retired with under $8,000.00 yearly income. No social security or other payments are made to me. If I sell my investment property which was a rental property, but has been vacant for a few years now, do I have to pay capital gains taxes on it? If so, what percentage? I was wondering if I would pay 0% for capital gains because I would be in the lowest tax bracket. Also as an example the property would be sold at $700,000. Please advise. Thank you!

Karen young says

Widow age 77. Never file social security since it’s only $18,000 yearly.but this year sold my short term stock for profit of $26,500. How do I file taxes .my deduction will be $13,300 sodo I have to also add 50 percent of my social security to stock profit and deduct the $13,300? What tax would I owe if any?

Harry Sit says

According to the H&R Block tax calculator, if your $26,500 capital gains were short-term you would owe about $2,000 in taxes. If the capital gains were long-term you wouldn’t owe any. When you file your taxes, use IRS Free File or find a VITA or TCE site near you.

https://www.hrblock.com/tax-calculator/

Edwin Tanghal says

My mom is 80 yrs old has 2 homes. And I’m renting one of them from her. She would like to sell her 2nd home to me to cash out the home. Our question is will she be hit with Capital Gains and is there a way for her to avoid or lessen the hit?

Cynthia Zeleski says

I have line 2 a capital distributions of 4622.00. I am disabled and widowed under age 65 and receive 22,800.00 in SSDI. Are my 2a capital distributions taxable?

Grace says

I receive $1128 a month between SSDI and VA Benefits. I have no other income.

If I cash in the currency that am holding, I will have a long term capital gain of $15 million. I’ve been holding the currency for over a year. I plan to terminate my SSDI once I cash in my currency.

Will I pay tax on my capital gains or not?

Harry Sit says

Please spend a tiny part of your $15 million and hire a CPA for professional advice.

Michelle says

My grandmother recently passed and we are settling her estate. She never worked but received my grandfather’s government pension. In addition to her own home, her son’s home was legally in her name. In 2013 that home was sold and there was a net profit of $50K which was given to the son. Is she responsible for any taxes from the sale? Nothing was ever filed with the IRS and the son is estranged.

Brenda Podnar says

I am 61 Years Old and have an annual income of $140,000 to $160,000 (determined at year end with bonus). I receive an income from the business I own. When I am at retirement age to collect Social Security at 66 and 8 months, and no longer will be reporting a wage but will be reporting a distribution.

Mai Nguyen says

Hi,

I’m 52 years old and have a miner. My husband passed away a year ago. I’m on Survivor benefit. I own a raw lot and need to sell it for improvement my own house. If I sale! is that effect my survival benefit?

Please help?

Harry Sit says

It won’t affect your survivor benefit but you may have to pay more taxes. Run a tax calculator such as the one from TurboTax twice to estimate your taxes. Run it first without the capital gain on the sale. Write down the number. Run it again with the capital gain on the sale. Compare with the previous number. That’s the amount of tax brought by selling the property.

https://turbotax.intuit.com/tax-tools/calculators/taxcaster/

Patrice says

Put it in a trust and have it transfer at her death.

The capital gains tax is calculated based on the original cost of the house (or its “basis” for tax purposes) and the fair market value of the house at the date of the sale.

If your child inherits your house, the stepped-up basis rule comes into effect. When you die, the cost (or basis) of your house is “stepped up” to the market value of your house on the date of your death.

Example:

If you bought your house for $200,000, its basis will be $200,000 the entire time you live in it. But, on the day you die, if your house was worth $500,000, its basis is “stepped up” to $500,000 and is no longer $200,000. So, if your child decides to later sell the house for $550,000, the profit on the sale is only $50,000 ($550,000-$500,000), not $350,000 ($550,000-$200,000).

Your child takes home $550,000 in either scenario. But in the eyes of the government, you can use the stepped-up basis to show a profit of only $50,000 vs. a profit of $350,000.

This has a real impact on the amount of capital gains your child has to pay: less theoretical profit = less taxes.

Even better, if your child sells the house after living in it for 2 years, they can qualify for the homeowner’s capital gains exclusion,

TRANSFER OF PROPERTY TO CHILD BY A REVOCABLE TRUST

A parent can transfer their property from themselves, while living, to their Revocable Trust, and then direct in the Trust that, upon the parent’s death, the property will be given to the child.

A Revocable Living Trust is a document, similar to a will, that allows someone to direct how and to whom they want their assets given upon death

Another advantage is that the trust and its assets, unlike a will, does NOT need to go through probate. The parent designates who they want to be the “Trustee” upon their death, and that Trustee then has the responsibility to give the property in the trust to the right people designated by the trust. Therefore, if the house is in the trust, and the trust says that the child gets the property upon the parent’s death, then the Trustee must give the property to the child. There is no court action necessary.

Mike says

I am a disabled NYC Firefighter since 1992,my tax free disability is $45.000 yr, I also receive SSDI, approx 20,000$. I purchased a home in 1992 in Florida, my only home since then. I need to relocate for various reasons. I am having difficulty getting an answer to my capital gains responsibility, never the same answer, I have been offered $1,400,000, yes, great gain, however, though I am real estate fit financially, the sale will be what determines my purchase power, could you please help me determine what my tax bill to Uncle Sam will be, at what capital gains rate thank you