QE3 is a tipping point to me. It hit me with the reality that we are going to be in this low interest rate world for the long haul. Instead of taking a punch in the face, I resolve to fight back. I’m tired of getting paid a puny amount on my money. I’m going to pull out all the stops and maximize my advantages as an individual investor.

Yes, you read that right. When it comes to investing, institutional investors usually have the upper hand. However, as individual investors we also have our own unique advantages. I’m going to show you each one of them and help you take full advantage of them.

Here’s my goal: double the bond yield without more risk. I want to double my bond yield. If you take the same steps I take, chances are you will double your bond yield as well. I’m going to call this effort “BY2” as in “bond yield times 2.”

Is that even possible? It’s not possible unless you try. We can’t be complacent any more. I have a sense my readers have well-above-average wealth. I’m going to set the bar high for my pursuit, really high. Suppose a married couple has a $1 million investment portfolio, 40% of which is invested in bonds. I want to double the bond yield for this couple without taking more risk than they already do.

The SEC yield on Vanguard Total Bond Market Fund Admiral Shares is 1.7%. To reach my goal, I need to find $1 million * 40% = $400,000 invested in bonds * 1.7% = $6,800 worth of additional opportunities in one year. That’s $3,400 per person. If I can make or save extra $3,400 per person for this hypothetical couple, I will have doubled their bond yield. If you don’t have $400,000 invested in bonds, when you make or save $3,400 per person, you will have more than doubled your bond yield.

Extra $6,800 for a couple with $1 million invested is a big deal. Any portfolio manager or financial advisor would kill to outperform the benchmark by 0.68% a year.

To borrow some business-speak, doubling the bond yield will be my BHAG — Big Hairy Audacious Goal. Finding ways to make or save $3,400 per person in the next 12 months will be my KPI — Key Performance Indicator.

Rules

I also have some rules for this endeavor:

(1) I want to make money with money, not with labor. So I’m not going to suggest that everybody should start a dog walking business or work an extra shift to pick up some more income.

(2) I assume they are already comfortable with their spending. I’m not going to suggest they stop buying a Starbucks latte every day because (a) they probably don’t buy it every day and (b) when they do I assume they enjoy the latte.

(3) Any effort involved had better be either one-time or automated. If it requires doing something on a recurring basis, it must not take more than 10 minutes per month. I’m not going to have them hunt for grocery coupons in Sunday papers every week and look for stores that have the same products on sale so they can layer coupons on top of sale.

(4) Don’t take more risk. I will favor guaranteed return over risky investments such as dividend stocks even though dividend stocks have potential for higher returns. If I do take more risk than say the Vanguard Total Bond Market Fund, it has to be a calculated risk and it has to involve a very small percentage of the portfolio.

(5) In order to count against the $3,400/person KPI, it can’t be something too obvious. I’m not going to suggest that my hypothetical couple should pay off credit card debt and save 19% interest because I assume they don’t have credit card debt at 19% interest rate. I’m not going to suggest that they move away from actively managed funds with a 2% expense ratio to index funds because I assume they already invest in index funds.

Advantages As an Individual

So what advantages do we have as individual investors? Let me give one example.

US Treasury sells I Bonds only to individual investors. By the established laws and regulations, the fixed rate is not allowed to go below zero. At the same time, the yield on comparable 5-year TIPS is negative 1.5%. That’s 1.5% extra yield institutional investors can’t have.

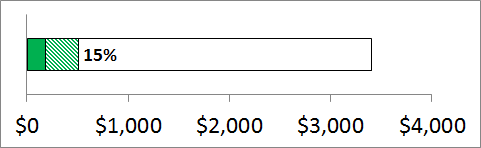

Yes, there is a maximum investment of $10,000 per person plus another $5,000 per tax return, but $25,000 a year is a much more meaningful number to our hypothetical couple with $400,000 invested in bonds than it is to institutional investors with millions and billions to invest. If they buy $20,000 worth of I Bonds now and another $5,000 at tax time next year, they will make additional $25,000 * 1.5% / 2 = $188 per person.

In addition, as I wrote last week, by moving $1,500 from their emergency fund to a new checking account with Citibank and Chase respectively, each of them will make ($150 – $15) + ($200 – $15) = $320. See previous post A Basic Checking Account That Pays More Than A High Yield Savings Account. Citibank and Chase are not giving a 10% bonus to institutional investors, but we as individuals can get the extra return. [Update: Both Citibank and Chase promotions expired now.]

You see just after these two moves I’m already 15% complete toward the goal. We will get there. Join me in this journey. Let’s do it.

If you haven’t signed up for my free email updates, please do it now. Don’t miss how you can really double what you make in bonds.

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

michael says

Hang on. $400k x 1.7% = $6800, which is the actual (current) bond yield, correct? So if you want to double it, shouldn’t you be shooting for $13,600? Or are you assuming that the $400k won’t be used, meaning that it will be able to earn $6800 in bond income, leaving you to earn another $6800 to double it?

Either way, it’s an interesting experiment. I’ll be following along. 🙂

Harry says

I’m only counting the *additional* amount gained through various moves. For example by moving $25k from regular government bonds to I Bonds (70% of the Vanguard Total Bond Market Fund is in government bonds), they would gain extra 1.5% on the $25k. So I counted $25k * 1.5% / 2 = $188 per person. Same for moving $1,500 from the emergency fund currently earning 1% to a checking account for the signup bonus. I already subtracted $15 when I calculated the additional gain.

KD says

Should we be looking at the yield or looking at the total return? One thing I noticed is that sign-up bonuses are a one-time thing and cannot be replicated – most of the time – each year. Also checking account bonuses are treated as taxable interest. So do we need to deduct taxes out of it?

Credit card sign up bonuses for spending X amount in Y months are the best deals out there as those are treated as price discounts and not taxed. The only caveat is to be careful that those bonuses – miles, points, cash etc – can be converted into something you spend anyway.

Two other things are (a) doing no-fee 0% BT and converting mortgage debt into unsecured debt and (b) investing in high yield foreign currency CD with a currency swap to protect your yield. Both have steep hill to really work – no fee 0% deals are few and far and I have availed all, and IRS reporting requirements for foreign currency transactions have become onerous and ridiculous.

Harry says

KD – Over time, the total return from a bond fund will be its yield. Any capital gains you get from declining interest rates are basically interest payments accelerated from the future. There are always businesses looking for new customers. You can replicate them each year by going to a different one. Next week’s post will show that it’s better to have bonds in taxable accounts. So we don’t have to deduct taxes out the additional amounts.

Thank you for giving me even more ideas. Sounds like you are way ahead of me. I have been complacent for too long. Better late than never!

Harry @ PF Pro says

This should be an interesting experiment. I really love credit card sign-up bonuses b/c once you sign up and hit the spending you’re done. I don’t have to do any additional work or really any work at all.

White Coat Investor says

I’m not sure having to do 20 different financial chores to get the $3400 qualifies under your rule # 3. In some ways, it’s easier for many of us to work a little more than to do all these chores. For example, if it takes an hour to get that checking account at Chase up and running (worth $135) but you can go to work for an extra hour and make $200 (an action that is repeatable), I’m not sure it’s worth it. Sure, if you’re at a $7 an hour job it might be worth it, but those folks don’t have million dollar portfolios.

In my experience there’s a lot more bang for your buck by either 1) earning more money or 2) spending less money than trying to change the third factor in the equation – increasing your return, especially without increasing risk.

Harry says

Maybe it’s easier for doctors but for many of us on salary, there is no way to work just an extra hour and get paid for it, let alone $200. To me, making extra money from some one-time effort out of idle time is worth it. The effort is much less than logging into P2P lending to pick 200 $25 loans one at a time. 🙂

Dwolf says

It sounds like you are saying by selling $25k of Vanguard Total Bond Admiral shares and buying $25k of I Bonds you will increase your yield by 1.5% (so 1.7% + 1.5% =3.2%). Did I misunderstand this because it seems like a bold prediction. Isn’t the new I bond rate going to be around 1.76% through April? Plus you have to hold for 5 years, so if you sell at the end of your year time frame you will lose the last 3 months interest.

If you are just comparing to TIPS I don’t see how that is relevant since the total bond market doesn’t hold any TIPS.

Harry says

Dwolf – The 1.5% advantage is measured against TIPS, which is comparable to nominal Treasuries after expected inflation. The total bond market fund holds a large percentage in nominal Treasuries. This initiative is looking for advantages that pay year after year, not just selling after one year.

mike says

THIS IS ONE OF THE BEST FREE FINANCIAL INFORMATIONAL I HAVE EVER SEEN

John says

Harry, did you complete the series of posts. I’m trying to understand where there are better investment options for my bond portfolio as well. Did not do the 529 plan since I have no kids

Harry says

It’s 97% complete. I’m still looking for more ideas. The articles in the series are here: http://thefinancebuff.com/tag/by2

John says

Harry,

After all the BY2 allocations have been completed; I assume that one will still have a substantial “bond” portfolio. Where does one invest that? Vanilla BND ETF or create a Bond ladder (to hedge against inflation) or some other strategy?

Great series of evergreen posts BTW to have readers coming back even after 2 years.

Harry Sit says

I put a chunk in 3% 5-year CDs from PenFed in December 2013 and January 2014. Let’s see if they will do it again. If not, there are still 5-year CDs paying 2.35% or thereabout. I also have money in an intermediate-term muni bond fund.

kc says

This link has old information.

Do you have update August 2016?

thanks,

KC

DB says

Hello, and thank you for this info. With rising interest rates affecting bond values, I too am interested in joining the BY2 quest.

I started with $5000 at Mango with an effective 5.28% after their fees. It’s more work than I prefer but it’s where I started.

I’ve also found:

5.12% on $1000 at Digital FCU

5.00% on $1000 each @ NetSpend, Western Union, HEB, Ace Express, and Brinks

4.00% on $2000 @ Priemer Members CU

3.00% on $15000 @ Lake Michigan CU

4.99% on $1000 at Blue FCU *Would not open an account due to Chex Inquiries.

I’m curious what other high yields others have found without excessive restrictions?

TJ says

Service Credit Union $500 @ 5% and $3000 @ 3%