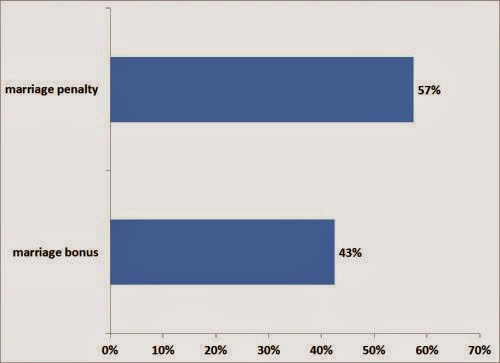

I thank the readers who participated in the marriage penalty or bonus poll. The results are in. Among the responses, 43% receive a marriage bonus. 57% receive a marriage penalty.

This split is somewhat a surprise to me. I thought more would have a marriage penalty. You definitely hear more about the marriage penalty, rarely about the marriage bonus. I guess it’s because people complain about the penalty but they gladly accept the bonus.

Marriage Bonus

You receive a marriage bonus when the two of you have more uneven incomes. The person with a higher income gets to use the low tax brackets from the person with a lower income. A one-earner married couple by definition receive a marriage bonus.

The flip side of a marriage bonus is the singles’ penalty. If two people with uneven incomes don’t marry, they pay higher taxes. Some same-sex couples who weren’t allowed to marry suffered from this penalty for a long time.

Marriage Penalty

On the other hand, you receive a marriage penalty when the two of you have relatively even incomes. Above 15%, the tax brackets for married filing jointly aren’t twice as wide as the brackets for singles. The higher your income, the higher your marriage penalty.

The flip side of the marriage penalty is the singles’ bonus. If two people with relatively even incomes live together but don’t marry, they pay lower taxes. Some same-sex couples who used to enjoy the singles’ bonus will pay the marriage penalty now after their marriage is legally recognized.

Size of Marriage Bonus or Penalty

My wife sometimes asks me if I knew how much we would pay in marriage penalty whether we would still marry. I always say yes. The table below shows the size of the marriage bonus or penalty among the poll responses:

| Marriage Bonus | Marriage Penalty | |

|---|---|---|

| Minimum | $500 | $1,000 |

| Maximum | $10,800 | $20,000 |

| Average | $5,200 | $6,100 |

| Median | $5,100 | $3,600 |

Nobody reported zero. Every respondent receives at least $500 in marriage bonus or at least $1,000 in marriage penalty.

Marriage bonus starts low, stays in a narrower range, and is more evenly spread out, as witnessed by its average and its median being close to each other. Marriage penalty is more concentrated at the lower end (lower median) but it goes out much farther. The larger penalties at the far end pull up the average.

Think about the couple who pay $20,000 more in taxes each year just because they are married. It takes a super-strong bond to say this is the price we pay for love. How much is $20,000 per year invested throughout their careers? Easily over $1 million.

To be honest I think it’s a pretty stupid system that makes you pay more or less in taxes just because the two of you are married or not married.

[Photo credit: Flickr user cupritte]

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

EscapeVelocity2020 says

The flip side of this, it made it a little easier decision for my wife to quit (back when we made similar incomes). We had just had our second child and could reduce daycare expenses and LOTS of schedule stress with her at home. It was a little rough having our household income cut in half, but going from the marriage penalty to a marriage bonus evened this out a little.

Chris in Boston says

Just a comment about the link to Personal Capital at the end of your blog posting. I recently set up an account with Personal Capital to see how their investment checkup tool works, and also to more easily evaluate my portfolio health.

I was very pleased to see that my current portfolio allocation not only has very low fees of less than 0.23%, but I am also perfectly aligned on the “Efficient Frontier”.

I have never relied on a personal financial planner, or advisor. I simply have self educated by reading blogs such as yours, as well as various other personal finance sites. There is a wealth of information out there for people who are willing to invest in themselves by taking the time to review their situation and take steps to correct any areas of concern.

After 7 years of being focused on my financial goals I have managed to build a portfolio that is sound, well diversified, and easy to manage. Personal Capital’s site provides some really nice tools to analyze your allocation and show where you may need to rebalance. It’s also great for highlighting what assets are costing you the most in fees. Making it very easy to take corrective steps.

I have no intention of paying Personal Capital to manage my assets, but it is terrific to see that resources like their site are available to the public for free, and are really quite powerful and useful tools!

Now a question for you…. regarding Marriage Penalty/Bonus. Is there any difference or concern if the marriage is a same sex marriage? Are there other factors to include in the equation?

Harry says

@Chris – Not much difference or concern if it’s a same-sex marriage. I mentioned it only because same-sex marriages weren’t recognized by the IRS until recently. Some same-sex couples were denied the marriage bonus for a long time and some others are entering into the marriage penalty for the first time.

Norman Klein says

Where one spouse has a large foreign income (as much as the person’s USA income) and would include that income obviously in gross income, but gets a $ for $ rebate of tax paid in the foreign country, what is the best way to allocate the marriage penalty?

Should one consider doing it on the basis of married but filing separately proportionately?

Harry Sit says

You take the tax for the married couple (whether filing jointly or separately as they actually do) minus the tax if they file as two singles individually.