In a low interest rates world, you should take a serious look at any loans you have. Although a 3.25% 30-year mortgage is often said to be "cheap money" or "almost free money" it’s neither cheap nor nearly free compared to the rate you earn on your bonds.

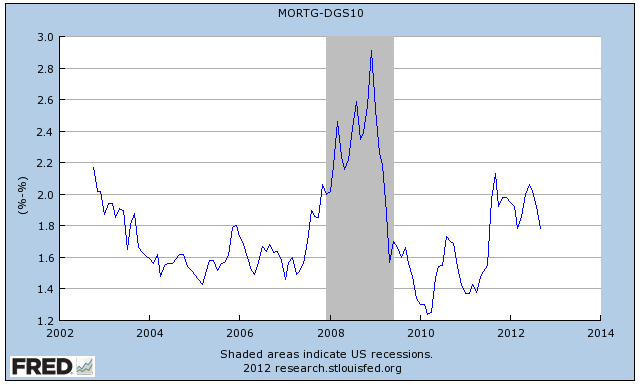

This chart shows the difference between the 10-year Treasury yield and the 30-year mortgage rate. Except the spike during the financial crisis, I would say the gap between the two right now is average to above-average. It’s not low. You are still paying a good premium on what you owe over what you earn.

Lending out money on one hand (holding bonds) and borrowing on the other at a higher rate doesn’t make sense unless you are betting on optionality: the mortgage rate is fixed and you are hoping to earn more eventually when rates go up. The problem with this line of thinking is that for every year you are holding out, you are paying a rate differential. By the time higher rates come, you are already way behind.

Contrary to popular belief, the interest rate on a 30-year fixed rate mortgage is NOT fixed for 30 years. It’s fixed until you sell the property OR 30 years, whichever comes first. Most people don’t stay in the same home for 30 years. When you sell and buy another home, you don’t get to keep your old rate. You get the market rate at that time. On average you get the fixed rate for more like 5-10 years. That’s not enough time for higher bond yields down the road to compensate for the deficit you accumulate in the early years. That is *if* we get higher bond yields down the road, which is not certain.

Also put yourself in the shoes of the investors behind your mortgage. Your mortgage eventually goes into a mortgage-backed security sold to investors. Those investors buy mortgage-backed securities for a reason. They have to bear the default risk. They have to pay a bank for servicing your loan. If they think they can earn a higher risk-adjusted return from buying the type of bonds you own through a bond mutual fund, they would do that and not bother with funding your mortgage.

Therefore you can’t expect to earn a higher risk-adjusted return from owning the same bonds they can buy. Maybe there’s a chance to make more from bonds institutional investors can’t buy (I Bonds, FDIC insured CDs, munis), but not from garden variety Treasuries, agency bonds, or investment-grade corporate bonds found in a total bond market fund.

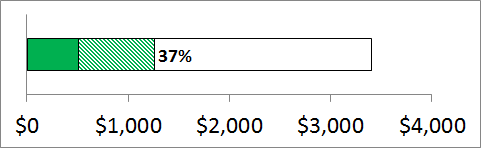

Having realized that it’s more tax efficient to have bonds in taxable accounts and that they are really upside down in bonds versus their mortgage, the hypothetical couple in my "double the bond yield" initiative decided to sell $150k in bonds to pay down their 2.75% 15-year mortgage. In doing so, they saved extra 1% a year on $150,000, which is $1,500 or $750 per person.

Remember they had a $1 million portfolio, 40% invested in bonds. After paying down their mortgage, they still have $250k in fixed income including I Bonds they bought in a previous move.

This move pushed the "double the bond yield" movement to 37% complete. I will get there.

[Photo credit: Flickr user 401(K) 2012]

Say No To Management Fees

If you are paying an advisor a percentage of your assets, you are paying 5-10x too much. Learn how to find an independent advisor, pay for advice, and only the advice.

edward says

CIT 1.80% 5yr CD comes with a 12 month early withdrawal penalty. Not worth the 0.05% differential in interest from a Discover Bank 5yr CD which has only a 6 month penalty. YMMV

babar says

ally bank has only 60 day simple interest rate penalty.

michael says

It’s hard to argue in favor of a mortgage at current rates vs. investing at current rates.

Full disclosure: We’ve paid off our mortgage.

The one thing that gives me pause is the prospect of much higher rates and/or inflation going forward. A low, fixed rate mortgage would be a good hedge against these possibilities.

Harry says

edward, babar – We need to do a bit of math on the early withdrawal penalty. On a 5-year CD paying 1.80%, you are getting 9% interest over five years (ignoring small compounding effect for now). If you pay 12 months of interest early withdrawal penalty, you lose 1.8%. If you go with a 5-year CD paying 1.75% but charges 6 months of interest, you expect to earn 8.75% over five years but lose 0.875% if you withdraw early. You are giving up 0.25% for sure for possibly paying less penalty. Your chance of early withdrawal must be greater than (9 – 8.75) / (1.8 – 0.875) = 27% for you to prefer the Discover CD.

Similarly, on the Ally CD paying 1.65% with a 2 months of interest early withdrawal penalty, your chance of early withdrawal must be greater than (9 – 8.25) / (1.8 – 0.275) = 49% for you to prefer the Ally CD.

If you are only thinking just-in-case, I don’t think the odds favor early withdrawal. When I buy a 5-year CD, I’m not planning a 27% or 49% chance to withdraw early.

Harry says

michael – As I mentioned in the post, you get that hedge for only as long as you stay in the home and you pay a price in every year before that happens. Say higher rates and/or inflation happens in year 8 and you are moving in year 10, you pay the price for 8 years and you only get to enjoy the hedge for 2 years. So it just depends on when higher rates and/or inflation happens and how long you are staying in the home. I think you made the smart decision in paying off your mortgage.

Enonymous says

Is the liquidity risk worth it?

Not asking rhetorically – for me I’m not sure it is, or at least not enough to get me to liquidate my I bonds to pay off my 3.375% 15 yr fixed – roughly 2.75% in my marginal bracket, state after tax. I bonds have no state tax, fully tax deferred for any extra 15 yrs too…

Harry says

Enonymous – It’s not all-or-nothing. Note the hypothetical couple in the post only used $150k out of their $400k in fixed income to pay down (not necessarily pay off) their mortgage. They are keeping their I Bonds and other fixed income investments still worth $250k.

John says

Harry, I agree that it makes sense to use the bond portion of your portfolio to pay down the mortgage; but do you then include the “mortgage paid” amount as part of your bond portfolio when considering rebalancing?

So if I want a 60/40 stock/bond portfolio.

For simplicity, I have 60K worth of stock and 40K worth of bond in line with my desired asset allocation.

I pay 20K mortgage using my bond fund leaving only 20K worth of bonds in my bond portfolio.

Depending on how stock and bonds rise/fall should I consider the 20K mortgage pre-payment as part of my Bond portfolio when rebalancing?

Harry says

I would. Otherwise you’d have to immediately rebalance to buy more bonds. If you use a spreadsheet you can even track where your mortgage balance should be if you didn’t prepay vs actual. The difference is your phantom bond.