Are you a saver? I bet you are. Did you know there’s a tax credit called Saver’s Credit that reduces your federal income tax if you save for retirement in an employer sponsored retirement plan (401k, 403b, etc.) or in an IRA? If you knew, did you ever receive it? I bet you didn’t.

I mentioned Saver’s Credit in one of my Friday roundups. I said it’s one of the most elusive tax credits.

I call it the “feel-good credit” because Congress created it to make itself feel good about helping low-income people save when in reality very few get it. When they get it, they get far less than what the credit first appears to offer.

What Is Saver’s Credit

Saver’s Credit, officially known as the Retirement Savings Contributions Credit, is a tax credit for saving for retirement. If you save at least $2,000, you can reduce your federal income tax by up to $1,000. It effectively works out to be a 100% match from other taxpayers ($1,000 out of pocket, $2,000 in your account). That’s on top of any match from your employer. It’s also on top of the normal benefits from a retirement account, for instance tax-free growth in a Roth account.

Who Qualify for Saver’s Credit

Because it’s free money from other taxpayers, Congress limited it to only people with low income. They need extra help because their low income makes it difficult for them to save for retirement on their own.

Depending on your income, there are three levels for this credit: 50%, 20%, and 10%. If your income is higher than the limit for the 10% level, you get nothing.

For a single person or a two-earner family, the income limit is set below the typical salaries of college graduates. A married, one-earner household will have an easier time to qualify for this credit. The table below lists the maximum Adjusted Gross Income (AGI) in 2013 for different tax filing statuses. See IRS Form 8880 for the latest numbers.

| 50% Credit | 20% Credit | 10% Credit | |

| Single | $17,750 | $19,250 | $29,500 |

| Head of Household | $26,625 | $28,875 | $44,250 |

| Married Filing Jointly | $35,500 | $38,500 | $59,000 |

In order to make sure rich people’s kids don’t take advantage of this generosity, Congress also put in rules to say you must be at least 18 and you can’t be a full-time student during any part of 5 calendar months in the year. Congress also added another rule saying anybody claimed as a dependent on another taxpayer’s tax return can’t qualify. If parents want the tax deduction, their child can’t claim Saver’s Credit.

With these additional rules, Congress intended to make Saver’s Credit available only to low-income people working full-time.

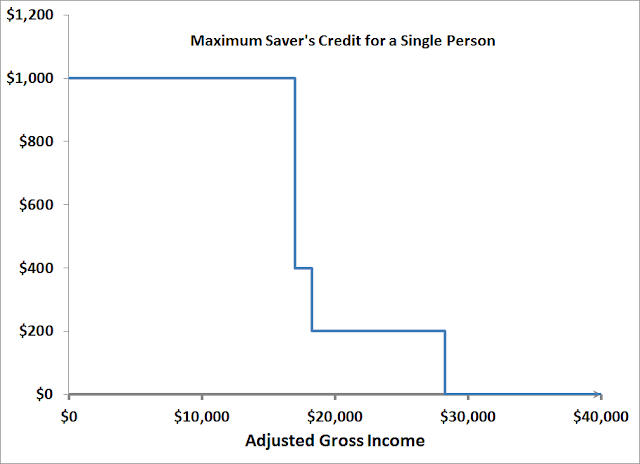

Watch Out for the Cliff

You should note how fast the credit drops off. If a single person has a AGI of $17,750, for a $2,000 contribution to a retirement account, this person qualifies for a Saver’s Credit at the 50% level. That’s $1,000. If she earns $100 more, she only qualifies at the 20% level, or $400. That extra $100 income reduces the credit by $600. It’s so not worth it. She’s much better off not earning the extra $100.

Because the credit drops off so fast, it’s very difficult to qualify at the 50% or 20% level. If people get this credit at all, most end up getting it at the 10% level. Save $2,000, get $200. It’s better than nothing but not as good as it sounds at the first glance.

Non-Refundable

Finally, because it’s a tax credit, not just a gift from other taxpayers, Congress made Saver’s Credit non-refundable, which means the credit can reduce your federal income tax to zero but that’s it.

You have to pay federal income tax before the Saver’s Credit in order to benefit from it. However, at the income limit set for the Saver’s Credit, sometimes the tax before the credit is less than the credit. You end up not getting the full credit as you think you would.

For instance, a single person earning $17,750 a year with just standard deductions will pay $778 in taxes. With Saver’s Credit, if she saves $2,000 for her retirement, she gets only a $778 credit, not the full $1,000.

Unintended Recipients

Is it realistic to expect a single person working full time earning less than $20k a year to save $2,000 for retirement? Not unless that person has other income that doesn’t show up on the tax return or the low income is only temporary.

A semi-retiree living on his savings and working part-time at a non-profit organization can qualify for the Saver’s Credit. His savings provides him income but that income isn’t income for tax purposes. In other words the income is low only on paper. His living standard isn’t low.

Someone taking a break from full time work in the middle of the year can qualify for Saver’s Credit. The low income is only temporary.

New college graduate in the first year of a full time job can qualify for Saver’s Credit (must graduate by April 30). Income from a partial year looks low even though the annual salary isn’t.

Claiming the Saver’s Credit

If all stars are aligned and you qualify for the Saver’s Credit, you claim it on Form 8880. If you use tax software, be sure to answer the questions about retirement savings even though you know your normally don’t have to report contribution to a Roth IRA. If you are right above a cutoff point, contribute to a Traditional IRA, which lowers your AGI and potentially qualifies you for the credit.

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

David C says

I was hoping I would be able to take advantage of this credit when I graduated from college several years ago and only worked 1/2 the year (hence 1/2 the income), but alas the “cannot be a full time student for 5 months” disqualified me. Oh well, it was probably for the best as the credit would have encouraged me to make tax-deferred contributions (to meet the AGI limits) rather than “mostly” Roth contributions that year.

DonB says

Technically, since you can use pre-tax savings the right question would be, “Is it realistic to expect a single person working full time earning $19,000 or less a year to save $2,000 for retirement?” They can use a $2,000 traditional IRA contribution to bring down their AGI to $17,000. That doesn’t necessary make much difference in the answer to the question (i.e. it still isn’t so easy to save when you have a low income), but it is something.

I’d guess that (smart) people landing near the 20% and 10% cliffs have a lot more flexibility tuning using exactly that technique.

Jeffrey says

Also very plausible for most military folks who are deployed and benefiting from current combat zone tax exclusions — i.e. if only a few months out of the year are taxable and contribute to his or her AGI they’re likely able to take advantage of this credit without cutting into desperately needed living expenses

Interestingly the IRS used to consider students at military academies (‘cadets’) exempt from the 5 mo. student clause as their activities were not strictly academic … not sure if this is still the case.

B says

“Is it realistic to expect a single person working full time earning $17,000 or less a year to save $2,000 for retirement? Not unless that person has other income that doesn’t show up on the tax return or the low income is only temporary.”

In the category of other income that doesn’t show up on the tax return — gifts from family members. My step daughter was able to take advantage of this because we gave her the $2K. Is a 20 something college graduate with temporarily low income and well-off parents an intended recipient? (I think probably not). It is a case of another complicated tax wrinkle ostensibly targeted to the very poor being exploited by wealthy families.

SH says

Wondering about the source for the cadets at service academies not being deemed students as far as eligibility for this credit is concerned. Would love to know if this is true.

MBM says

I just wanted to add that by excluding students they may have unintentionally blocked people out of recieving this credit who are NOT young 19 year old students. For example, my husband and I are married filing jointly. Our income is below the indicated bracket for the 50% Credit. We have three young children and my husband is the only one currently working. We live on a low income so I stay at home with the kids and am also going to school full time so that I will be qualified for a job after graduation that pays better than minimum wage. I would love to be working, but with my qualifications and the ages of our children we would be paying about the same in childcare expenses as I would be earning. But since I am a student this bars us from the credit. How frustrating!

Harry Sit says

I think the contribution and the student status are tracked per person. Being a student, you don’t qualify for the credit for your contribution but your husband should still get the credit for his contribution.