I wrote about tax credits last week. This time let’s look at tax deductions. First a recap of the difference between a tax credit and a tax deduction:

A tax credit directly reduces your tax dollar for dollar. If you are supposed to pay $5,000 in tax, a $500 tax credit reduces your tax to $4,500.

A tax deduction reduces your taxable income, which indirectly reduces your tax. If you are supposed to pay $5,000 in tax, a $500 tax deduction reduces your taxable income by $500 which then reduces your tax by only $500 * 15% = $75 if you are in the 15% marginal tax bracket.

Therefore a $100 tax credit is worth a lot more than a $100 tax deduction.

Within tax deductions, there are above-the-line deductions, standard deduction, and itemized deductions.

Above the Line Deductions

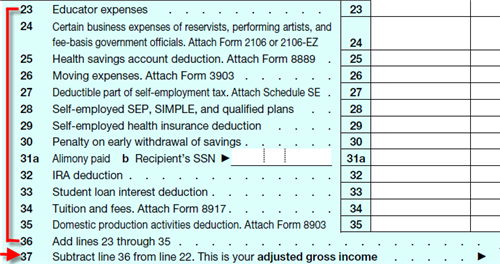

Above-the-line deductions are officially known as adjustments to income. The “line” refers to the last line on page 1 of your Form 1040 or Form 1040A, which is labeled adjusted gross income (AGI).

That AGI is the magic number that determines eligibility for many tax breaks. Above-the-line deductions reduce that magic number. They can be taken even if you use the standard deduction and not itemize your deductions. An above-the-line deduction also passes through AMT, whereas some of the other deductions are disallowed under AMT.

Therefore a $100 above-the-line tax deduction is better than a $100 below-the-line deduction.

Itemized Deductions

I think most people already know the difference between standard deduction and itemized deductions. So I’m not going to waste your time. Mortgage interest, state income tax, property tax, and charitable donations are typical itemized deductions.

I do want to point out just because an expense is tax deductible, it doesn’t mean you can actually take the deduction.

I know it sounds weird but it’s true. It took me a while to figure out many exciting deductions are only deductions in theory. Most people can’t really take them. This is because some deductions must first clear a floor before they can be deducted.

For example medical expenses are tax deductible, but you can only deduct the portion which exceeds 10% of your AGI. For many people that means zero.

Theft losses are also tax deductible, but only the portion which exceeds 10% of your AGI. That’s a very high hurdle.

Safe deposit box rental fees and tax preparation fees are also theoretically tax deductible, but few people can actually deduct them because they fall into a bucket called miscellaneous deductions, which are subject to a floor of 2% of AGI. All your miscellaneous deductions added together must exceed 2% of your AGI before you can deduct anything.

For example, suppose your AGI is $80,000, 2% of your AGI is $1,600. If you have $1,700 in all miscellaneous deductions, you can only deduct $100. If you have $1,500 in all miscellaneous deductions, you can’t deduct anything.

Therefore most miscellaneous deductions are practically useless.

The following table lists some of the tax deductions (as of 2013 tax year) in alphabetical order. I’m not enumerating miscellaneous deductions here because there are simply too many. All the links point to the official IRS web site for that topic. Every tax deduction has a unique set of qualification rules. Out of 20 tax deductions listed here, 12 are above-the-line; the other eight are itemized deductions.

| Tax Deduction | Above-the-Line? |

|---|---|

| Alimony Paid | Yes |

| Casualty and Theft Losses | No, 10% AGI floor |

| Charitable donations | No |

| CD early withdrawal penalty | Yes |

| Educator Expenses | Yes |

| Health Savings Account | Yes |

| Investment Expenses | No |

| Medical and Dental Expenses | No, 10% AGI floor |

| Miscellaneous Expenses | No, 2% AGI floor |

| Mortgage Interest and Points | No |

| Mortgage Insurance Premiums | No |

| Moving Expenses | Yes |

| Property Tax | No |

| Qualified Performing Artists | Yes |

| Self-Employment Health Insurance | Yes |

| Self-Employment Retirement Plan Contributions | Yes |

| 1/2 of Self-Employment Tax | Yes |

| State Income Tax or Sales Tax | No |

| Student Loan Interest | Yes |

| Traditional IRA Contributions | Yes |

| Tuition and Fees | Yes |

Isn’t it a mess or what?

Say No To Management Fees

If you are paying an advisor a percentage of your assets, you are paying 5-10x too much. Learn how to find an independent advisor, pay for advice, and only the advice.

Sam says

You have explained this with amazing clarity. Thank you very much!!!

L says

I only wish you had written this portion in my textbook on Federal Taxation. I am preparing for my final and this article is so helpful.

Thank you,

L

Mike says

Is there a way that you know of to modify the way turbo tax does taxes, I have all my deductions in, though I feel like the software is not putting enough deductions above the line

Mira says

Thank you so much. I”m taking a tax class and my teach confused me so much but this article brought me SO MUCH clarity! You should replace my teacher..lol 🙂

Joe Drane says

Super stuff. Your explanation immediately answered my question on whether or not to pay my homestead property taxes in December 2011 or January 2012. I paid off my house last year. Yea! But I have no mortgage interest deductions to claim in 2011. Boo (sort of), so itemizing my taxes is a no-go for me anymore. Since property taxes are below the line, and since my community allows me to pay after the first of the year, I can pay them twice in 2012. So, I should have enough deductions to itemize in 2012.

But if the Feds hate this then I best find out now….

Harry Sit says

Joe Drane – The Feds will have no problem with your bunching deductions and alternating between using the standard deduction one year and itemizing deductions the next.

BJ says

Thanks for this article. Before I had not made the connection as to why the above the line deductions were more valuable than below the line deductions. Now it makes sense because of the certain criteria needed to qualify for below the line.

BlawBlaw says

The 6th item in the hyperlinked table should be “Investment Expenses” not “Investment Interest.”

Harry says

Thank you. Fixed.

Tim says

Why aren’t deductions allowed in calculating income for healthcare. We have a ton of interest expense. This is really stupid, in my opinion.

Robin R says

Is $3000 of a capital loss from the sale of stock above the line? In years past I thought that amount was allowed on the first page of my 1040.

Harry Sit says

It’s above the line but it’s technically not an adjustment. It’s part of the total income. It’s positive when it’s a gain and negative when it’s a loss.

thien nguyen says

What about standard deduction? Is the qualified income before or after standard deduction?

Harry Sit says

The standard deduction is below the line.

Bill says

Are my federal and state tax free dividends added to my agi

Harry Sit says

Not to the standard AGI, but yes to a few versions of Modified AGI for different purposes.