[Updated on July 4, 2025 with changes from One Big Beautiful Bill Act.]

My other post listed 2024 2025 401k and IRA contribution and income limits. I also calculated the inflation-adjusted tax brackets and some of the most commonly used numbers in tax planning for 2025 using the published inflation numbers and the same formula prescribed in the tax law. These calculations have been confirmed by the IRS Rev. Proc. 2024-40.

- 2024 2025 Standard Deduction

- 2024 2025 Tax Brackets

- 2024 2025 Capital Gains Tax

- Net Investment Income Tax

- 2024 2025 Estate and Trust Tax Brackets

- 2024 2025 Qualified Charitable Distributions (QCD) Limit

- 2024 2025 2026 Medicare Part B and Part D IRMAA

- 2024 2025 Gift Tax Exclusion

- 2024 2025 Savings Bonds Tax-Free Redemption for College Expenses

2024 2025 Standard Deduction

You don’t pay federal income tax on every dollar of your income. You deduct an amount from your income before you calculate taxes. About 90% of all taxpayers take the standard deduction. The other ~10% itemize deductions when their total deductions exceed the standard deduction. In other words, you’re deducting a larger amount than your allowed deductions when you take the standard deduction. Don’t feel bad about taking the standard deduction!

The basic standard deduction in 2024 and 2025 are:

| 2024 | 2025 | |

|---|---|---|

| Single or Married Filing Separately | $14,600 | $15,750 |

| Head of Household | $21,900 | $23,625 |

| Married Filing Jointly | $29,200 | $31,500 |

Source: IRS Rev. Proc. 2023-34, Rev. Proc. 2024-40, One Big Beautiful Bill Act.

People who are age 65 and over have a higher standard deduction than the basic standard deduction.

| 2024 | 2025 | |

|---|---|---|

| Single, age 65 and over | $16,550 | $17,750 |

| Head of Household, age 65 and over | $23,850 | $25,625 |

| Married Filing Jointly, one person age 65 and over | $30,750 | $33,100 |

| Married Filing Jointly, both age 65 and over | $32,300 | $34,700 |

Source: IRS Rev. Proc. 2023-34, Rev. Proc. 2024-40, One Big Beautiful Bill Act.

People who are blind have an additional standard deduction.

| 2024 | 2025 | |

|---|---|---|

| Single or Head of Household, blind | +$1,950 | +$2,000 |

| Married Filing Jointly, one person is blind | +$1,550 | +$1,600 |

| Married Filing Jointly, both are blind | +$3,100 | +$3,200 |

Source: IRS Rev. Proc. 2023-34, Rev. Proc. 2024-40.

2024 2025 Tax Brackets

The tax brackets are based on taxable income, which is AGI minus various deductions. The tax brackets in 2024 are:

| Single | Head of Household | Married Filing Jointly | |

|---|---|---|---|

| 10% | $0 – $11,600 | $0 – $16,550 | $0 – $23,200 |

| 12% | $11,600 – $47,150 | $16,550 – $63,100 | $23,200 – $94,300 |

| 22% | $47,150 – $100,525 | $63,100 – $100,500 | $94,300 – $201,050 |

| 24% | $100,525 – $191,950 | $100,500 – $191,950 | $201,050 – $383,900 |

| 32% | $191,950 – $243,725 | $191,950 – $243,700 | $383,900 – $487,450 |

| 35% | $243,725 – $609,350 | $243,700 – $609,350 | $487,450 – $731,200 |

| 37% | Over $609,350 | Over $609,350 | Over $731,200 |

Source: IRS Rev. Proc. 2023-34.

The 2025 tax brackets will be:

| Single | Head of Household | Married Filing Jointly | |

|---|---|---|---|

| 10% | $0 – $11,925 | $0 – $17,000 | $0 – $23,850 |

| 12% | $11,925 – $48,475 | $17,000 – $64,850 | $23,850 – $96,950 |

| 22% | $48,475 – $103,350 | $64,850 – $103,350 | $96,950 – $206,700 |

| 24% | $103,350 – $197,300 | $103,350 – $197,300 | $206,700 – $394,600 |

| 32% | $197,300 – $250,525 | $197,300 – $250,500 | $394,600 – $501,050 |

| 35% | $250,525 – $626,350 | $250,500 – $626,350 | $501,050 – $751,600 |

| 37% | Over $626,350 | Over $626,350 | Over $751,600 |

Source: IRS Rev. Proc. 2024-40.

A common misconception is that when you get into a higher tax bracket, all your income is taxed at the higher rate and you’re better off not having the extra income. That’s not true. Tax brackets work incrementally. If you’re $1,000 into the next tax bracket, only $1,000 is taxed at the higher rate. It doesn’t affect the income in the previous brackets.

For example, someone single with a $70,000 AGI in 2024 will pay:

| First 14,600 (the standard deduction) | 0% | ||

| Next $11,600 | 10% | ||

| Next $35,550 ($47,150 – $11,600) | 12% | ||

| Final $8,250 | 22% |

This person is in the 22% tax bracket but only a tiny fraction of the $70,000 AGI is taxed at 22%. Most of the income is taxed at 0%, 10%, and 12%. The blended tax rate is only 10.3%. If this person doesn’t earn the final $8,250, he or she is in the 12% bracket instead of the 22% bracket but the blended tax rate only goes down slightly from 10.3% to 8.8%. Making the extra income doesn’t cost this person more in taxes than the extra income.

Don’t be afraid of going into the next tax bracket.

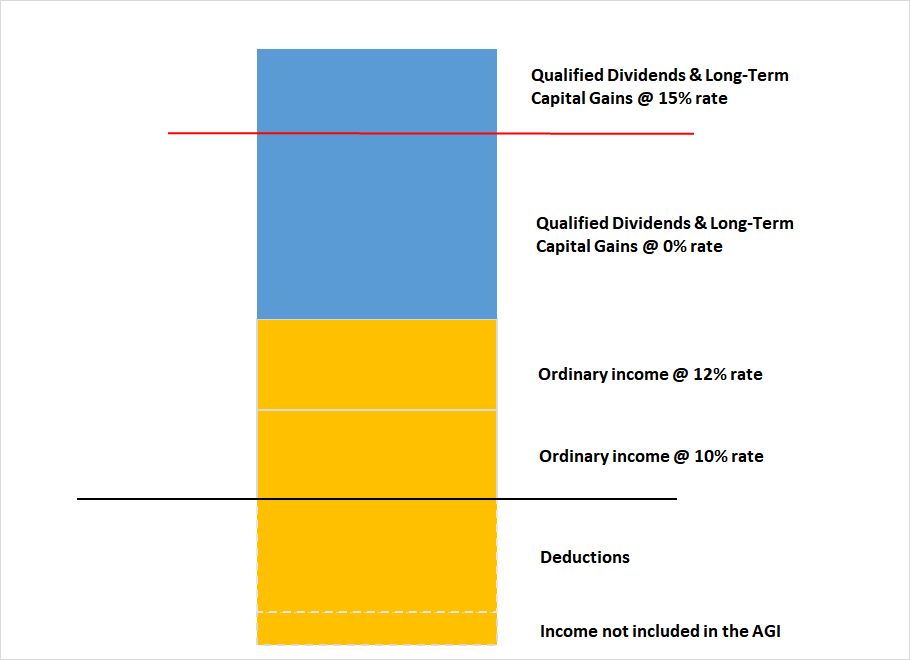

2024 2025 Capital Gains Tax

When your other taxable income (after deductions) plus your qualified dividends and long-term capital gains are below a cutoff, you will pay 0% federal income tax on your qualified dividends and long-term capital gains under this cutoff.

This is illustrated by the chart below. Taxable income is the part above the black line, after subtracting deductions. A portion of the qualified dividends and long-term capital gains is taxed at 0% when the other taxable income plus these qualified dividends and long-term capital gains are under the red line.

The red line is close to the top of the 12% tax bracket but they don’t line up exactly.

| 2024 | 2025 | |

|---|---|---|

| Single or Married Filing Separately | $47,025 | $48,350 |

| Head of Household | $63,000 | $64,750 |

| Married Filing Jointly | $94,050 | $96,700 |

Source: IRS Rev. Proc. 2023-34, Rev. Proc. 2024-40.

For example, suppose a married couple filing jointly has $70,000 in other taxable income (after deductions) plus $25,000 in qualified dividends and long-term capital gains in 2024. The maximum zero rate amount cutoff is $94,050. $24,050 of the qualified dividends and long-term capital gains ($94,050 – $70,000) is taxed at 0%. The remaining $25,000 – $24,050 = $950 is taxed at 15%

A similar threshold exists on the upper end for qualified dividends and long-term capital gains. When your other taxable income (after deductions) plus your qualified dividends and long-term capital gains are above a cutoff, you will pay 20% federal income tax instead of 15% on your qualified dividends and long-term capital gains above this cutoff.

| 2024 | 2025 | |

|---|---|---|

| Single | $518,900 | $533,400 |

| Head of Household | $551,350 | $566,700 |

| Married Filing Jointly | $583,750 | $600,050 |

| Married Filing Separately | $291,850 | $300,000 |

Source: IRSRev. Proc. 2023-34, Rev. Proc. 2024-40.

Net Investment Income Tax

Net Investment Income Tax (NIIT) is a 3.8% tax on the portion of interest, dividends, and capital gains that makes your modified adjustable gross income exceed these thresholds:

| MAGI Threshold | |

|---|---|

| Single | $200,000 |

| Head of Household | $200,000 |

| Married Filing Jointly | $250,000 |

| Married Filing Separately | $125,000 |

These thresholds are fixed by law. They are not adjusted for inflation. You pay a 3.8% tax on the amount your MAGI exceeds these thresholds or your total interest, dividends, and capital gains, whichever is less.

Suppose you’re married filing jointly and you have $300,000 MAGI, which includes $10,000 in interest, dividends, and capital gains. Although your MAGI exceeds the $250,000 threshold by $50,000, you will pay 3.8% in NIIT on only $10,000 because you have only $10,000 in net investment income.

Suppose you’re married filing jointly and you have $260,000 MAGI, which includes $150,000 in interest, dividends, and capital gains. Although you have $150,000 in net investment income, you will pay 3.8% in NIIT only on $10,000 because your MAGI exceeds the $250,000 threshold by only $10,000.

2024 2025 Estate and Trust Tax Brackets

Estates and trusts have different tax brackets than individuals. These apply to non-grantor trusts and estates that retain income as opposed to distributing the income to beneficiaries. Grantor trusts (including the most common revocable living trusts) don’t pay taxes separately. The income of a grantor trust is taxed to the grantor at the grantor’s tax brackets.

Here are the tax brackets for estates and trusts in 2024 and 2025:

| 2024 | 2025 | |

|---|---|---|

| 10% | $0 – $3,100 | $0 – $3,150 |

| 24% | $3,100 – $11,150 | $3,150 – $11,450 |

| 35% | $11,150 – $15,200 | $11,450 – $15,650 |

| 37% | over $15,200 | over $15,650 |

Source: IRS Rev. Proc. 2023-34, Rev. Proc. 2024-40.

2024 2025 Qualified Charitable Distributions (QCD) Limit

People older than 70-1/2 can make Qualified Charitable Distributions (QCD) from their Traditional IRA directly to qualifying charitable organizations. QCDs count toward the Required Minimum Distribution (RMD).

Your total QCDs can’t exceed $105,000 in 2024. The limit will go up to $108,000 in 2025.

The QCD limit is per person. If you’re married, both you and your spouse can make QCDs up to the limit separately from your respective IRAs.

Source: IRS Notice 2023-75, author’s calculations.

2024 2025 2026 Medicare Part B and Part D IRMAA

People on Medicare Part B and Part D pay a higher Medicare premium when their Modified Adjusted Gross Income from two years ago crosses certain thresholds. I track these in Medicare Part B IRMAA Premium MAGI Brackets.

2024 2025 Gift Tax Exclusion

Each person can give another person up to a set amount in a calendar year without having to file a gift tax form. Not that filing a gift tax form is onerous, but many people avoid it if they can. This gift tax exclusion amount will increase from $18,000 in 2024 to $19,000 in 2025.

| 2024 | 2025 | |

|---|---|---|

| Gift Tax Exclusion | $18,000 | $19,000 |

Source: IRS Rev. Proc. 2023-34, Rev. Proc. 2024-40.

The gift tax exclusion is counted by each giver to each recipient. As a giver, you can give up to $18,000 each in 2024 to an unlimited number of people without having to file a gift tax form. If you give $18,000 to each of your 10 grandkids in 2024, you still won’t be required to file a gift tax form. Any recipient can also receive a gift from an unlimited number of people. If a grandchild receives $18,000 from each of his or her four grandparents in 2024, no taxes or tax forms will be required.

2024 2025 Savings Bonds Tax-Free Redemption for College Expenses

If you cash out U.S. Savings Bonds (Series I or Series EE) for college expenses or transfer to a 529 plan, your modified adjusted gross income must be under certain limits to get a tax exemption on the interest. See Cash Out I Bonds Tax Free For College Expenses Or 529 Plan.

Here are the income limits in 2024 and my estimates for 2025. The limits are in a phase-out range. You get a full exemption if your income is below the lower number in the range. You get no exemption if your income is above the higher number in the range. You get a partial exemption if your income falls within the range.

| 2024 | 2025 | |

|---|---|---|

| Single, Head of Household | $96,800 – $111,800 | $99,500 – $114,500 |

| Married Filing Jointly | $145,200 – $175,200 | $149,250 – $179,250 |

Source: IRS Rev. Proc. 2023-34, Rev. Proc. 2024-40.

Say No To Management Fees

If you are paying an advisor a percentage of your assets, you are paying 5-10x too much. Learn how to find an independent advisor, pay for advice, and only the advice.

Tom Tran says

For example, suppose a married couple filing jointly has $70,000 in other taxable income (after deductions) and $25,000 in qualified dividends and long-term capital gains in 2024. The maximum zero rate amount cutoff is $94,050. $24,050 of the qualified dividends and long-term capital gains ($94,050 – $70,000) is taxed at 0%. The remaining $25,000 – $24,050 = $950 is taxed at 15%

——————————————————————————————————————-

I plug in the numbers to the Qualified Dividends & Capital Gain Tax Worksheet: taxable income =70k, qualified dividends and long-term capital gains =25k. The result: All 25k is taxed at 0%. However, if the taxable income is 95k, your calculation would be correct.

Harry Sit says

I said $70k in “other” taxable income after deductions “and” $25k in qualified dividends and long-term capital gains. The total taxable income is $95k. I’ll change the word “and” to “plus” to make it more clear.

Lawrence Ryan says

Where can I get the 2024 Qualified Dividends and Capital Gain Tax Worksheet/

Harry Sit says

2024 Qualified Dividends and Capital Gain Tax Worksheet is in 2024 Form 1040 Instructions (page 36).

https://www.irs.gov/pub/irs-pdf/i1040gi.pdf