My other post listed 2026 401k and IRA contribution and income limits. I also calculated the inflation-adjusted tax brackets and some of the most commonly used numbers in tax planning for 2026 using the published inflation numbers and the same formula prescribed in the tax law. These numbers have been confirmed by IRS Rev. Proc. 2025-32.

- 2025 2026 Standard Deduction

- 2025 2026 Tax Brackets

- 2025 2026 Capital Gains Tax

- Net Investment Income Tax

- 2025 2026 Qualified Charitable Distributions (QCD) Limit

- 2025 2026 2027 Medicare IRMAA

- 2025 2026 Gift Tax Exclusion

- 2025 2026 SALT Cap

- 2025 2026 Child Tax Credit

- 2025 2026 Kiddie Tax

- 2025 2026 Savings Bonds Tax-Free Redemption for College Expenses

- 2025 2026 Estate and Trust Tax Brackets

2025 2026 Standard Deduction

You don’t pay federal income tax on every dollar of your income. You deduct an amount from your income before you calculate taxes. Over 80% of all taxpayers take the standard deduction. The other 10-20% itemize deductions when their total deductions exceed the standard deduction. In other words, you’re deducting a larger amount than your allowed deductions when you take the standard deduction. Don’t feel bad about taking the standard deduction!

The basic standard deduction in 2025 and 2026 is:

| 2025 | 2026 | |

|---|---|---|

| Single or Married Filing Separately | $15,750 | $16,100 |

| Head of Household | $23,625 | $24,150 |

| Married Filing Jointly | $31,500 | $32,200 |

People who are age 65 and over have a higher standard deduction than the basic standard deduction.

| 2025 | 2026 | |

|---|---|---|

| Single, age 65 and over | $17,750 | $18,150 |

| Head of Household, age 65 and over | $25,625 | $26,200 |

| Married Filing Jointly, one person age 65 and over | $33,100 | $33,850 |

| Married Filing Jointly, both age 65 and over | $34,700 | $35,500 |

The 2025 Trump tax law raised the standard deduction for 2025. The increases are reflected in the tables above. It also introduced a new senior deduction for people age 65 and over. The senior deduction is in addition to the standard deduction. It isn’t part of the standard deduction. See Social Security Is Still Taxed Under the New 2025 Trump Tax Law for more on the senior deduction.

People who are blind have a higher standard deduction.

| 2025 | 2026 | |

|---|---|---|

| Single or Head of Household, blind | +$2,000 | $2,050 |

| Married Filing Jointly, one person is blind | +$1,600 | $1,650 |

| Married Filing Jointly, both are blind | +$3,200 | $3,300 |

Source: IRS Rev. Proc. 2024-40, Rev. Proc. 2025-32.

2025 2026 Tax Brackets

The tax brackets are based on taxable income, which is AGI minus various deductions. The tax brackets in 2025 are:

| Single | Head of Household | Married Filing Jointly | |

|---|---|---|---|

| 10% | $0 – $11,925 | $0 – $17,000 | $0 – $23,850 |

| 12% | $11,925 – $48,475 | $17,000 – $64,850 | $23,850 – $96,950 |

| 22% | $48,475 – $103,350 | $64,850 – $103,350 | $96,950 – $206,700 |

| 24% | $103,350 – $197,300 | $103,350 – $197,300 | $206,700 – $394,600 |

| 32% | $197,300 – $250,525 | $197,300 – $250,500 | $394,600 – $501,050 |

| 35% | $250,525 – $626,350 | $250,500 – $626,350 | $501,050 – $751,600 |

| 37% | Over $626,350 | Over $626,350 | Over $751,600 |

Source: IRS Rev. Proc. 2024-40.

The 2025 Trump tax law raised the top of the 10% and 12% brackets in 2026 by a little less than 2% above the normal inflation adjustments. The 2026 tax brackets are:

| Single | Head of Household | Married Filing Jointly | |

|---|---|---|---|

| 10% | $0 – $12,400 | $0 – $17,700 | $0 – $24,800 |

| 12% | $12,400 – $50,400 | $17,700 – $67,450 | $24,800 – $100,800 |

| 22% | $50,400 – $105,700 | $67,450 – $105,700 | $100,800 – $211,400 |

| 24% | $105,700 – $201,775 | $105,700 – $201,750 | $211,400 – $403,550 |

| 32% | $201,775 – $256,225 | $201,750 – $256,200 | $403,550 – $512,450 |

| 35% | $256,225 – $640,600 | $256,200 – $640,600 | $512,450 – $768,700 |

| 37% | Over $640,600 | Over $640,600 | Over $768,700 |

Source: IRS Rev. Proc. 2025-32.

A common misconception is that when you go into a higher tax bracket, all your income is taxed at the higher rate and you’re better off not having the extra income. That’s not true. Tax brackets work incrementally. If you’re $1,000 into the next tax bracket, only $1,000 is taxed at the higher rate. It doesn’t affect the income in the previous brackets.

For example, someone single with a $70,000 AGI in 2025 will pay:

| First 15,750 (the standard deduction) | 0% | ||

| Next $11,925 | 10% | ||

| Next $36,550 ($48,475 – $11,925) | 12% | ||

| Final $5,775 | 22% |

This person is in the 22% tax bracket, but only a tiny fraction of the $70,000 AGI is taxed at 22%. Most of the income is taxed at 0%, 10%, and 12%. The blended tax rate is only 9.8%. If this person doesn’t earn the final $5,775, they are in the 12% bracket instead of the 22% bracket, but the blended tax rate only decreases slightly from 9.8% to 8.7%. Making the extra income doesn’t cost this person more in taxes than the additional income.

Don’t be afraid of going into the next tax bracket.

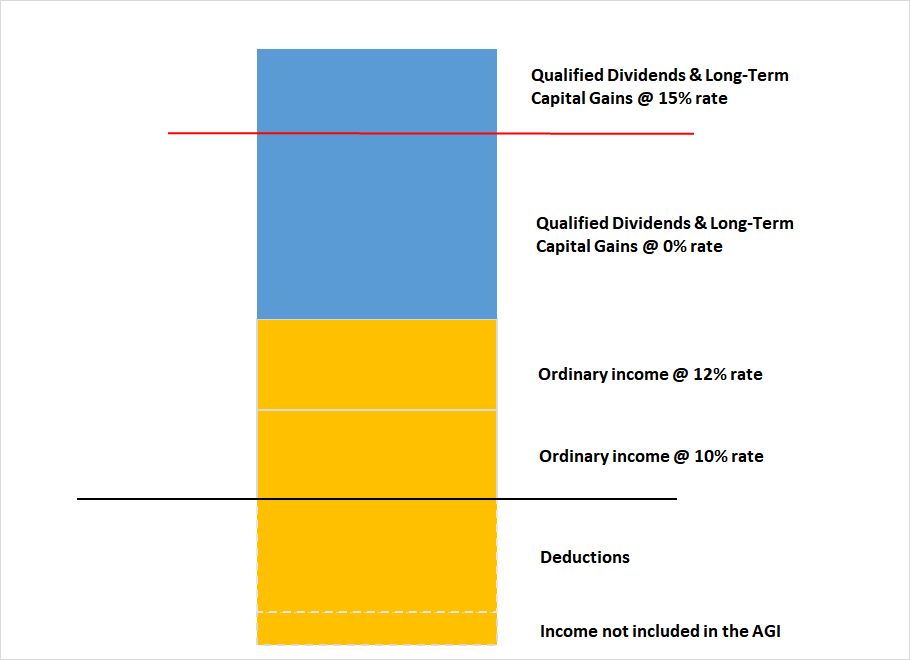

2025 2026 Capital Gains Tax

When your other taxable income (after deductions) plus your qualified dividends and long-term capital gains are below a cutoff, you will pay 0% federal income tax on your qualified dividends and long-term capital gains under this cutoff.

This is illustrated by the chart below. Taxable income is the part above the black line, after subtracting deductions. A portion of the qualified dividends and long-term capital gains is taxed at 0% when the other taxable income plus these qualified dividends and long-term capital gains is under the red line.

The red line is close to the top of the 12% tax bracket, but they don’t line up exactly.

| 2025 | 2026 | |

|---|---|---|

| Single or Married Filing Separately | $48,350 | $49,450 |

| Head of Household | $64,750 | $66,200 |

| Married Filing Jointly | $96,700 | $98,900 |

For example, suppose a married couple filing jointly has $70,000 in other taxable income (after deductions) plus $30,000 in qualified dividends and long-term capital gains in 2025. The maximum zero-rate amount cutoff is $96,700. $26,700 of the qualified dividends and long-term capital gains ($96,700 – $70,000) is taxed at 0%. The remaining $30,000 – $26,700 = $3,300 is taxed at 15%.

A similar threshold exists on the upper end for qualified dividends and long-term capital gains. When your other taxable income (after deductions) plus your qualified dividends and long-term capital gains are above a cutoff, you will pay 20% federal income tax instead of 15% on your qualified dividends and long-term capital gains above this cutoff.

| 2025 | 2026 | |

|---|---|---|

| Single | $533,400 | $545,500 |

| Head of Household | $566,700 | $579,600 |

| Married Filing Jointly | $600,050 | $613,700 |

| Married Filing Separately | $300,000 | $306,850 |

Source: IRS Rev. Proc. 2024-40, Rev. Proc. 2025-32.

Net Investment Income Tax

Net Investment Income Tax (NIIT) is a 3.8% tax on the portion of interest, dividends, and capital gains that makes your modified adjusted gross income exceed these thresholds:

| MAGI Threshold | |

|---|---|

| Single | $200,000 |

| Head of Household | $200,000 |

| Married Filing Jointly | $250,000 |

| Married Filing Separately | $125,000 |

These thresholds are fixed by law. They are not adjusted for inflation. You pay a 3.8% tax on the amount your MAGI exceeds these thresholds or your total interest, dividends, and capital gains, whichever is less.

Suppose you’re married filing jointly, and you have a $300,000 MAGI, which includes $10,000 in interest, dividends, and capital gains. Although your MAGI exceeds the $250,000 threshold by $50,000, you will pay 3.8% in NIIT on only $10,000 because you have only $10,000 in net investment income.

Suppose you’re married filing jointly, and you have $260,000 MAGI, which includes $150,000 in interest, dividends, and capital gains. Although you have $150,000 in net investment income, you will pay 3.8% in NIIT only on $10,000 because your MAGI exceeds the $250,000 threshold by only $10,000.

2025 2026 Qualified Charitable Distributions (QCD) Limit

People older than 70-1/2 can make Qualified Charitable Distributions (QCD) from their Traditional IRA directly to qualifying charitable organizations. QCDs count toward the Required Minimum Distribution (RMD).

The total QCDs can’t exceed $108,000 in 2025. The limit will go up to $111,000 in 2026.

The QCD limit is per person. If you’re married and both you and your spouse are over 70-1/2, you can make QCDs up to the limit separately from your respective IRAs.

Source: IRS Notice 2024-80, author’s calculations.

2025 2026 2027 Medicare IRMAA

People on Medicare Part B and Part D pay a higher Medicare premium when their Modified Adjusted Gross Income from two years ago crosses certain thresholds. I track these in Medicare IRMAA Premium MAGI Brackets.

2025 2026 Gift Tax Exclusion

Each person can give another person up to a set amount in a calendar year without having to file a gift tax form. Not that filing a gift tax form is onerous, but many people avoid it if they can. This gift tax exclusion amount will stay the same at $19,000 in 2025 and 2026.

| 2025 | 2026 | |

|---|---|---|

| Gift Tax Exclusion | $19,000 | $19,000 |

Source: IRS Rev. Proc. 2024-40, IRS Rev. Proc. 2025-32.

The gift tax exclusion is counted by each giver to each recipient. As a giver, you can give up to $19,000 each in 2025 to an unlimited number of people without having to file a gift tax form. If you give $19,000 to each of your 10 grandkids in 2025, you still won’t be required to file a gift tax form. Any recipient can also receive a gift from an unlimited number of people. If a grandchild receives $19,000 from each of his or her four grandparents in 2025, no taxes or tax forms will be required.

2025 2026 SALT Cap

The 2025 Trump tax law raised the cap on the State and Local Taxes (SALT) deduction from $10,000 to $40,000. The cap starts to phase out when the income exceeds $500,000. The cap and the phaseout increase by 1% a year through 2029. See Calculator: Effect of Higher SALT Cap in 2025 Trump Tax Law.

| 2025 | 2026 | |

|---|---|---|

| SALT Cap | $40,000 | $40,400 |

| Phaseout Starts | $500,000 | $505,000 |

| Phaseout Ends | $600,000 | $606,333 |

Source: One Big Beautiful Bill Act, author’s calculations.

2025 2026 Child Tax Credit

Families with a qualifying child are eligible for a tax credit per child. A portion of the Child Tax Credit is refundable.

The maximum Child Tax Credit per child and the maximum refundable portion will stay the same between 2025 and 2026.

| 2025 | 2026 | |

|---|---|---|

| Child Tax Credit (per child) | $2,200 | $2,200 |

| Refundable maximum (per child) | $1,700 | $1,700 |

Source: IRS Rev. Proc. 2024-40, IRS Rev. Proc. 2025-32.

2025 2026 Kiddie Tax

When a dependent child receives investment income, a certain amount is tax-free, and the same amount is taxed at the child’s rate. Additional unearned income is taxed at the parent’s rate.

These amounts will stay the same between 2025 and 2026.

| 2025 | 2026 | |

|---|---|---|

| Tax-Free | $1,350 | $1,350 |

| Taxed at Child’s Rate | $1,350 | $1,350 |

Source: IRS Rev. Proc. 2024-40, Rev. Proc. 2025-32.

2025 2026 Savings Bonds Tax-Free Redemption for College Expenses

If you cash out U.S. Savings Bonds (Series I or Series EE) for college expenses or transfer to a 529 plan, your modified adjusted gross income must be under certain limits to get a tax exemption on the interest. See Cash Out I Bonds Tax Free For College Expenses Or 529 Plan.

Here are the income limits in 2025 and 2026. The limits are in a phase-out range. You get a full exemption if your income is below the lower number in the range. You get no exemption if your income is above the higher number in the range. You get a partial exemption if your income falls within the range.

| 2025 | 2026 | |

|---|---|---|

| Single, Head of Household | $99,500 – $114,500 | $101,800 – $116,800 |

| Married Filing Jointly | $149,250 – $179,250 | $152,650 – $182,650 |

Source: IRS Rev. Proc. 2024-40, IRS Rev. Proc. 2025-32.

2025 2026 Estate and Trust Tax Brackets

Estates and trusts have different tax brackets than individuals. These apply to non-grantor trusts and estates that retain income as opposed to distributing the income to beneficiaries. Grantor trusts (including the most common revocable living trusts) don’t pay taxes separately. The income of a grantor trust is taxed to the grantor at the grantor’s tax brackets.

Here are the tax brackets for estates and trusts in 2025 and 2026:

| 2025 | 2026 | |

|---|---|---|

| 10% | $0 – $3,150 | $0 – $3,300 |

| 24% | $3,150 – $11,450 | $3,300 – $11,700 |

| 35% | $11,450 – $15,650 | $11,700 – $16,000 |

| 37% | over $15,650 | over $16,000 |

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

Tom Tran says

For example, suppose a married couple filing jointly has $70,000 in other taxable income (after deductions) and $25,000 in qualified dividends and long-term capital gains in 2024. The maximum zero rate amount cutoff is $94,050. $24,050 of the qualified dividends and long-term capital gains ($94,050 – $70,000) is taxed at 0%. The remaining $25,000 – $24,050 = $950 is taxed at 15%

——————————————————————————————————————-

I plug in the numbers to the Qualified Dividends & Capital Gain Tax Worksheet: taxable income =70k, qualified dividends and long-term capital gains =25k. The result: All 25k is taxed at 0%. However, if the taxable income is 95k, your calculation would be correct.

Harry Sit says

I said $70k in “other” taxable income after deductions “and” $25k in qualified dividends and long-term capital gains. The total taxable income is $95k. I’ll change the word “and” to “plus” to make it more clear.

Tracy says

Do you still have a TY 2025 calculator. This calculator is for 2026 in which the deductibles are different. You used to be able to select the TY. Thanks

Harry Sit says

It never had a way to select the tax year. It used to use 2025 brackets. I updated it to use 2026 brackets because many people asked for it.

Lawrence Ryan says

Where can I get the 2024 Qualified Dividends and Capital Gain Tax Worksheet/

Harry Sit says

2024 Qualified Dividends and Capital Gain Tax Worksheet is in 2024 Form 1040 Instructions (page 36).

https://www.irs.gov/pub/irs-pdf/i1040gi.pdf

Bill says

I thought the Senior Standard Deduction changed so that Seniors could get an extra $12000 off if they earned less than $150000 (married filing jointly) with the amount fazing out 6% (times 2 since 2 people, to make the math work) between $150000 and $250000 . Won’t the deduction now be $33100 + MAX( $12000 – (MAGI – 150000)*.06*2, 0) for those seniors married filing jointly with a MAGI over $150000? Or am I missing something?

Harry Sit says

The senior deduction is a separate deduction from the standard deduction. It isn’t part of the standard deduction. If it were, it wouldn’t be available to taxpayers who itemize deductions. See Tax Deductions: Above-the-Line, Itemized, and Neither for more on different types of tax deductions. The senior deduction is in the “neither” category.

Bill says

Thanks Harry for clearing up that misunderstanding on my part

Gary says

Harry, a fairly detailed nerdy question for my own financial modeling spreadsheets.

Will the starting year for inflation adjustments be redefined as 2025, since the standard deductions have been reset (Single $15,750, MFJ $31,500)?

Are they doing some complex calculation like staying with previous inflation adjustments to the previous amounts and then just adding in the additional 2025 amounts (Single $750, MFJ $1,500)?

Or is this just an IRS undefined procedure yet?

Harry Sit says

The starting year is reset. The 2025 numbers will be the new baseline for 2026 and beyond. The methodology is still the same as before.

Gary says

Harry, will 2025 starting year also be used for tax brackets as well as the standard deductions that I asked about?

I did not think about tax brackets until after I saw your response. thanks!

Harry Sit says

2025 tax brackets aren’t changing, and it won’t become the new base year for the future, but … there’s a different can of worms. Starting in 2026, only for the 10% and 12% brackets, the base year is pushed back one year from 2017 to 2016. This effectively raises the top of the 10% and 12% brackets in 2026 and beyond by about 2%. Approximately $1,000 that would otherwise be in the 22% bracket in 2026 will stay in the 12% bracket. It creates more work for me when I update this post next week for 2026.

Jim says

Harry,

I thought I read that they were pushing back the base year for inflation adjustments to 2016 (135.237) for the 10%, 12% AND 22% brackets. Not true??

Harry Sit says

Not the 22% bracket if you’re talking about the top of the bracket. The bottom of the 22% bracket, which is the same as the top of the 12% bracket, will go up in 2026 more than the usual inflation adjustment.

Jim Twaddell says

Harry,

If I understand you correctly:

For computing the 10% and 12% top of bracket, the 2016 C-CPI-U index of 135.237 (I think) will now be used.

But for the 22% thru 35% brackets, we will continue to use the 2017 C-CPI-U index of 138.237.

I might be a little off on the 2016 index for tax computations. The figure of 135.237 I believe was the average of C-CPI-U for Sep 2015-Aug 2016 as reported in Sep 2017, with most of those months not being finalized. The final C-CPI-U average for Sep 2015-Aug 2016 was 135.993, but that was not reported until Oct 2017.

Harry Sit says

For what it’s worth, I’m using 135.993 for 2016. My theory is that you use the latest numbers available at the time of calculation. We had no choice but to use the preliminary numbers when we were calculating for 2018 but we don’t need to hang on to those preliminary numbers in later years.

Douglas Lefforge says

The 2017-2018 CPI-U Average is 249.28. Are you saying that from 2025 and on that the average will now be 310.96, not 249.28?

My MAGI IRMAA Brackets formula instructions to myself has been:

Calculate 2026 MAGI IRMAA Brackets:

1. Estimate the 12 month average CPI-U from 9/2024 – 8/2025.

2. Subtract 249.28 (baseline 2019 CPI-U average) from step 1.

3. Divide the step 2 figure by the 2017-2018 CPI-U Average of 249.28.

4.1. Increase the 2026 baseline IRMAA brackets by the step 3 figure percentage:

4.2. Standard x 1.4.

4.3. Standard x 2.0.

4.4. Standard x 2.6.

4.5. Standard x 3.2.

4.6. Standard x 3.4.

5. Round IRMAA Brackets to the nearest 1,000.

6. Double IRMAA Brackets for married filing jointly.

I appreciate all corrections and clarifications.

Harry Sit says

The previous question was about the standard deduction. IRMAA calculations aren’t changing.

Ashley says

I love it when my calculations mostly match yours! Especially this year with the change to the standard deduction and brackets using different base years. That being said, my understanding is that the child tax credit will also be tied to inflation going forward. Is that something that you’re planning on tracking?

Harry Sit says

I added the Child Tax Credit, kiddie tax, and the SALT cap to the post. The SALT cap isn’t adjusted by inflation but by a fixed percentage.

Gary says

Harry, I think you only need to add 3-4 more items and the IRS will just have to share a link to your blog instead of publishing their release document. 😀😀

That’s my way of saying I appreciate your work.

Ginny Minch says

I’m wondering if you have plans to release a 2nd edition of My Financial Toolbox. Thank you for sharing your insights.