[The next update will be on August 12, 2026, when the government publishes the CPI data for July 2026.]

Seniors 65 or older can sign up for Medicare. The government refers to people who receive Medicare as “beneficiaries.” Medicare beneficiaries must pay a premium for Medicare Part B, which covers doctors’ services, and Medicare Part D, which covers prescription drugs. The premiums paid by Medicare beneficiaries cover about 25% of the program costs for Part B and Part D. The government pays the remaining 75%.

What Is IRMAA?

Medicare imposes surcharges on higher-income beneficiaries. The theory is that higher-income beneficiaries can afford to pay more for their healthcare. Instead of doing a 25:75 split with the government, they must pay a higher share of the program costs.

The surcharge is called IRMAA, which stands for Income-Related Monthly Adjustment Amount. This applies to both Traditional Medicare (Part B and Part D) and Medicare Advantage plans.

According to a Medicare Trustees Report, less than 10% of Medicare Part B beneficiaries paid IRMAA. The extra premiums they paid reduced the government’s share of the total Part B and Part D expenses by two percentage points. Big deal?

History of IRMAA

IRMAA was added to Medicare by the Medicare Prescription Drug, Improvement, and Modernization Act of 2003. The Republican Congress under President George W. Bush passed it in November 2003.

IRMAA started with only Part B. The Patient Protection and Affordable Care Act, passed in 2010 by the Democratic Congress under President Obama, expanded IRMAA to also include Part D.

The Bipartisan Budget Act of 2018, passed by the Republican Congress under President Trump, added a new tier for people with the highest incomes.

IRMAA has been the law of the land for over 20 years. Different congresses and administrations from different parties made small tweaks, but its structure hasn’t changed much since the beginning. IRMAA has become a bipartisan consensus. There’s no impetus for major changes.

MAGI

The income used to determine IRMAA is your Modified Adjusted Gross Income (MAGI) — which is your AGI plus tax-exempt interest and dividends from muni bonds — from two years ago. Your 2024 MAGI determines your IRMAA in 2026. Your 2025 MAGI determines your IRMAA in 2027. Your 2026 MAGI determines your IRMAA in 2028.

There are many definitions of MAGI for different purposes. The MAGI for ACA health insurance subsidies includes 100% of the Social Security benefits. The MAGI for IRMAA includes taxable Social Security benefits, but not untaxed Social Security benefits. If you read somewhere else that says that untaxed Social Security benefits are included in MAGI, they’re talking about a different MAGI, not the MAGI for IRMAA.

You can use Calculator: How Much of My Social Security Benefits Is Taxable? to calculate the taxable portion of your Social Security benefits. The new 2025 Trump tax law didn’t change how Social Security is taxed. It didn’t change anything related to the MAGI for IRMAA. See Social Security Is Still Taxed Under the New 2025 Trump Tax Law.

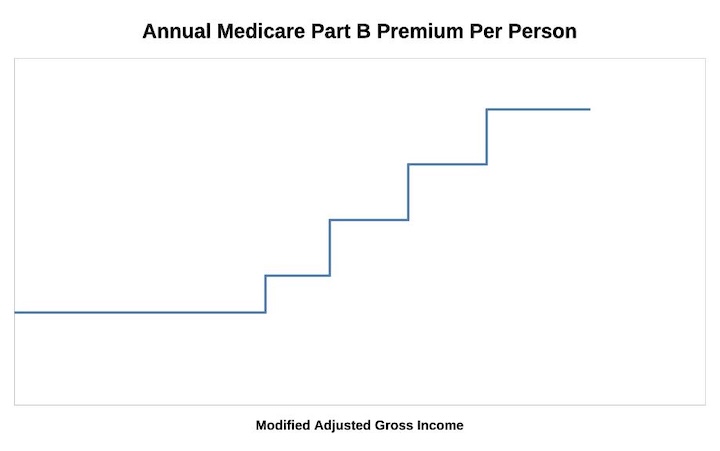

As if it’s not complicated enough, while not moving the needle much, IRMAA is divided into five income brackets. Depending on the income, higher-income beneficiaries pay 35%, 50%, 65%, 80%, or 85% of the program costs instead of 25%. As a result, they pay 1.4, 2.0, 2.6, 3.2, or 3.4 times the standard Medicare premium.

The threshold for each bracket can cause a sudden increase in the monthly premium amount you pay. If your income crosses into the next bracket by $1, your Medicare premiums can suddenly jump by over $1,000 per year. If you are married and filing a joint tax return, and both of you are on Medicare, $1 more in income can make Medicare premiums jump by over $1,000/year for each of you.

* The last bracket on the far right isn’t displayed in the chart.

If your income is near a bracket cutoff, try to keep it low and stay in a lower bracket. Using the income from two years ago makes it more difficult to manage.

2026 IRMAA Brackets

The standard Part B premium in 2026 is $202.90 per person per month. The income on your 2024 federal tax return (filed in 2025) determines the IRMAA you pay in 2026.

| Part B Premium | 2026 Coverage (2024 Income) |

|---|---|

| Standard | Single: <= $109,000 Married Filing Jointly: <= $218,000 Married Filing Separately <= $109,000 |

| 1.4x Standard | Single: <= $137,000 Married Filing Jointly: <= $274,000 |

| 2.0x Standard | Single: <= $171,000 Married Filing Jointly: <= $342,000 |

| 2.6x Standard | Single: <= $205,000 Married Filing Jointly: <= $410,000 |

| 3.2x Standard | Single: < $500,000 Married Filing Jointly: < $750,000 Married Filing Separately < $391,000 |

| 3.4x Standard | Single: >= $500,000 Married Filing Jointly: >= $750,000 Married Filing Separately >= $391,000 |

Source: CMS news release

Higher-income Medicare beneficiaries also pay a surcharge for Part D. The IRMAA income brackets are the same for Part B and Part D. The Part D IRMAA surcharges are relatively lower in dollars.

I also have the tax brackets for 2026. Please read 2026 Tax Brackets, Standard Deduction, Capital Gains, QCD if you’re interested.

2027 IRMAA Brackets

We have nine data points right now out of the 11 needed for the IRMAA brackets in 2027 (based on 2025 income).

If annualized inflation from July through August 2026 is 0% (prices staying flat at the latest level) or 3% (approximately a 0.25% increase every month), these will be the 2027 numbers:

| Part B Premium | 2027 Coverage (2025 Income) 0% Inflation | 2027 Coverage (2025 Income) 3% Inflation |

|---|---|---|

| Standard | Single: <= $112,000 Married Filing Jointly: <= $224,000 Married Filing Separately <= $112,000 | Single: <= $112,000 Married Filing Jointly: <= $224,000 Married Filing Separately <= $112,000 |

| 1.4x Standard | Single: <= $141,000 Married Filing Jointly: <= $282,000 | Single: <= $141,000* or $142,000 Married Filing Jointly: <= $282,000* or $284,000 |

| 2.0x Standard | Single: <= $176,000 Married Filing Jointly: <= $352,000 | Single: <= $176,000* or $177,000 Married Filing Jointly: <= $352,000* or $354,000 |

| 2.6x Standard | Single: <= $211,000* or $212,000 Married Filing Jointly: <= $422,000* or $424,000 | Single: <= $211,000* or $212,000 Married Filing Jointly: <= $422,000* or $424,000 |

| 3.2x Standard | Single: < $500,000 Married Filing Jointly: < $750,000 Married Filing Separately < $388,000 | Single: < $500,000 Married Filing Jointly: < $750,000 Married Filing Separately < $388,000 |

| 3.4x Standard | Single: >= $500,000 Married Filing Jointly: >= $750,000 Married Filing Separately >= $388,000 | Single: >= $500,000 Married Filing Jointly: >= $750,000 Married Filing Separately >= $388,000 |

Some of the projected 2027 brackets are the same for 0% inflation and 3% inflation due to rounding. The unrounded numbers for 3% inflation are higher, but not high enough to break into the next level after rounding.

If you’re married filing separately, you may have noticed that the 3.2x bracket goes down with inflation. That’s not a typo. If you look up the history of that bracket (under heading C), you’ll see it went down from one year to the next. That’s the law. It puts more people married filing separately with a high income into the 3.4x bracket.

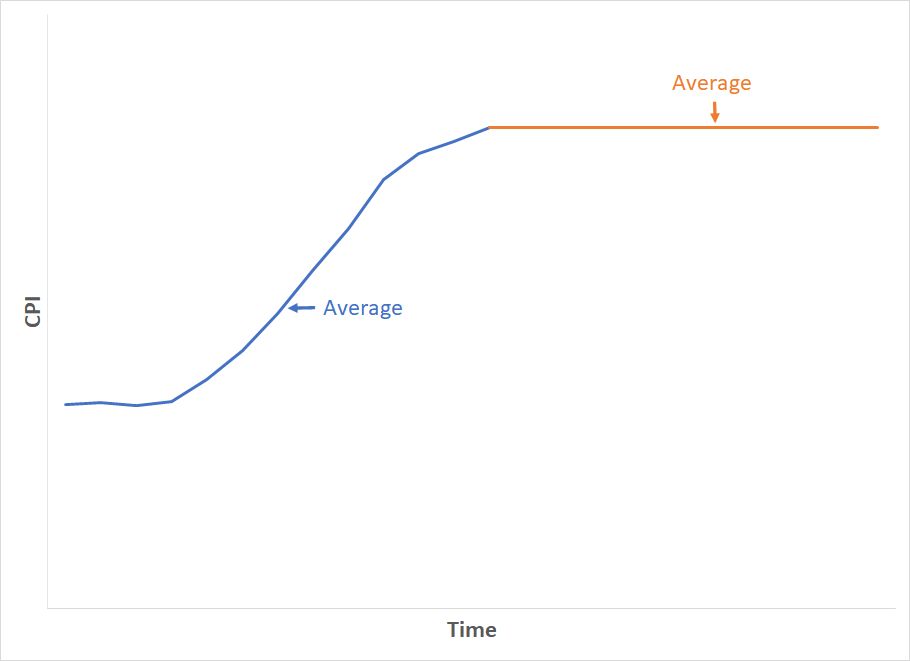

Because the formula compares the average of 12 monthly CPI numbers over the average of 12 monthly CPI numbers in a base period, even if prices stay the same in the following months, the average of the next 12 months will still be higher than the average in the previous 12 months.

To use exaggerated numbers, suppose gas prices went up from $3/gallon to $3.50/gallon over the last 12 months. The average gas price in the last 12 months was maybe $3.20/gallon. When gas price inflation becomes 0%, it means it stays at the current price of $3.50/gallon. The average for the next 12 months is $3.50/gallon. Brackets based on an average gas price of $3.50/gallon in the next 12 months will be higher than brackets based on an average gas price of $3.20/gallon in the previous 12 months.

If you really want to get into the weeds of the methodology for these calculations, please read this reply on comment page 2 and this other comment on page 4.

The Missing October 2025 CPI

The government did not and will not publish the CPI number for October 2025 because it didn’t collect the necessary price data during a government shutdown. It’s unclear how the Social Security Administration will calculate the 12-month average with only 11 data points.

The Treasury Department used 325.604 as the October CPI to calculate interest on inflation-indexed Treasury bonds. The Social Security Administration won’t necessarily use the same number for IRMAA. I calculated the projected 2027 brackets in two ways: (a) using a straight average of the projected 11 monthly data points, omitting October 2025; and (b) using 325.604 for October 2025. The projected 2027 brackets are largely the same under the two methods due to rounding. I put an asterisk on the number calculated by method (b) where they differ.

2028 IRMAA Brackets

We have no data point right now out of the 12 needed for the IRMAA brackets in 2028 (based on 2026 income). We can only make preliminary estimates and plan for some margin to stay clear of the cutoff points.

If annualized inflation from July 2026 through August 2027 is 0% (prices staying flat at the latest level) or 3% (approximately a 0.25% increase every month), these will be the 2028 numbers:

| Part B Premium | 2028 Coverage (2026 Income) 0% Inflation | 2028 Coverage (2026 Income) 3% Inflation |

|---|---|---|

| Standard | Single: <= $114,000 Married Filing Jointly: <= $228,000 Married Filing Separately <= $114,000 | Single: <= $116,000 Married Filing Jointly: <= $232,000 Married Filing Separately <= $116,000 |

| 1.4x Standard | Single: <= $143,000 Married Filing Jointly: <= $286,000 | Single: <= $146,000 Married Filing Jointly: <= $292,000 |

| 2.0x Standard | Single: <= $179,000 Married Filing Jointly: <= $358,000 | Single: <= $183,000 Married Filing Jointly: <= $366,000 |

| 2.6x Standard | Single: <= $214,000 Married Filing Jointly: <= $428,000 | Single: <= $219,000 Married Filing Jointly: <= $438,000 |

| 3.2x Standard | Single: < $507,000 Married Filing Jointly: < $760,500 Married Filing Separately < $393,000 | Single: < $517,000 Married Filing Jointly: < $775,500 Married Filing Separately < $401,000 |

| 3.4x Standard | Single: >= $507,000 Married Filing Jointly: >= $760,500 Married Filing Separately >= $393,000 | Single: >= $517,000 Married Filing Jointly: >= $775,500 Married Filing Separately >= $401,000 |

Effect of the Iran War

The CPI numbers in recent months were affected by the volatile energy prices due to the Iran war. The most recent data point reflects the market’s hope that the war would end following a ceasefire and a preliminary deal. The 0% inflation numbers assume that prices will stay at the current level. Energy prices can rise sharply if the war drags on. If that happens, CPI numbers in the upcoming months can escalate beyond the 3% inflation estimate, which may push the IRMAA numbers above the projections.

Roth Conversion Tools

When you manage your income by doing Roth conversions, you must watch your MAGI carefully to avoid accidentally crossing one of these IRMAA thresholds by a small amount and triggering higher Medicare premiums.

I use two tools to help with calculating how much to convert to Roth. I wrote about these tools in Roth Conversion with TurboTax What-If Worksheet and Roth Conversion with Social Security and Medicare IRMAA.

Nickel and Dime

The standard Medicare Part B premium is $202.90/month in 2026. A 40% surcharge on the Medicare Part B premium is $974/year per person or $1,948/year for a married couple both on Medicare.

In the grand scheme, when a couple on Medicare has over $218,000 in income, they’re already paying a large amount in taxes. Does making them pay another $2,000 make that much difference? It’s less than 1% of their income, but nickel-and-diming just makes people mad. People caught by surprise when their income crosses into a higher bracket by just a small amount are angry at the government. Rolling it all into the income tax would be much more effective.

Oh well, if you are on Medicare, watch your income and don’t accidentally cross a line for IRMAA.

IRMAA Appeal

If your income two years ago was higher because you were working at that time, and now your income is significantly lower because you retired (“work reduction” or “work stoppage”), you can appeal the IRMAA initial determination. The “life-changing events” that make you eligible for an appeal include:

- Death of spouse

- Marriage

- Divorce or annulment

- Work reduction

- Work stoppage

- Loss of income from income producing property

- Loss or reduction of certain kinds of pension income

You file an appeal with the Social Security Administration by filling out Form SSA-44 to show that although your income was higher two years ago, you have a reduced income now due to one of the life-changing events above. For more information on the appeal, see Medicare Part B Premium Appeals.

Not Penalized For Life

If your income two years ago was higher and you don’t have a life-changing event that makes you qualify for an appeal, you will pay the higher Medicare premiums for one year. The IRMAA surcharge goes into the Medicare budget. It helps to keep Medicare going for other seniors on Medicare.

IRMAA is re-evaluated every year as your income changes. If your higher income two years ago was due to a one-time event, such as realizing capital gains or taking a large withdrawal from your IRA, your IRMAA will decrease automatically when your income comes down in the following year. It’s not the end of the world to pay IRMAA for one year.

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

Bob says

Jeff. The IRS must have included on form 1040 the “QCD” checkbox, as well as the IRA “Rollover” checkbox, for a reason. At least that seems to be the point with respect to the 2025 1040 return, given that financial institutions issuing the 1099-R for 2025 had the “option” (not mandatory) to show a “Y” (QCD) rather than a “7” (normal distribution) in box 7. I honestly don’t think it would be preferable for taxpayers who do a QCD to populate those line 4 items on the 1040. I think it would eliminate any question as to the role of the QCD on the tax return for any 1099-R that did not show a “Y” on the 1099-R, as opposed to simply offsetting the IRA gross distribution with the QCD amount as a calculation and then showing the net taxable distribution on line 4b of the return.

Since you’re saying that the IRS has made it mandatory for 1099-R issuers to show a “Y” for a QCD in box 7 of the 1099-R starting with tax year 2026, the IRS may decide (for 2026 1040 purposes) not to include the QCD checkbox on the 1040. I think they included the QCD checkbox on the 2025 1040 only because code “Y” was not mandatory for the tax year 2025 1099-R form.

Jeff Enders says

Bob – it’ll be mid-summer before the draft version of the 2026 1040 is available.

Richard says

I suspect the 2026 return will still need a QCD checkbox since it will not be possible for all 1099-R providers to know that a distribution is a QCD and so would not put a Y down. Schwab, for example, allows one to write checks drawn on an accompanyiong IRA bank account. It will not know which of those checks are for QCDs and which are not. Unless it asks the IRA holder to specify somehow that a paarticular check is for a QCD it would not be able to issue a 1099-R with a Y code. That means there would have to be some other way for the taxpayer to indicate that there is a QCD.

Nancy Memmel says

Sorry, no comment here I just clicked on the link in my e-mail to get to the comments but through poor mouse control hit the unsubscribe link instead… sigh.

John F says

Bob

I stand by my comment regarding box 4c(3). Please provide where in the 2025 1040 Instructions it shows: “enter the QCD $ amount in 4(c)(3)”.

Bob says

John. See “Exception 3” on page 27 of the 1040 instructions. It covers how to report the portion of an IRA distribution associated with a QCD.

John F says

Bob

Exception 3 requires the QCD box be checked. That’s it. Box 3 has nothing to do with a QCD. Subtracting 4b (IRA taxable amount) from 4a (IRA distribution) = Amount of QCD. There isn’t any reason to have the QCD shown anywhere else.

Richard says

Bob

> Subtracting 4b (IRA taxable amount) from 4a (IRA distribution) = Amount of QCD.

Unless there is also a rollover.

Bob says

Do whatever you want on the 1040 return. As I previously indicated, my recommendation is to check the QCD box on line 4(c)(2) and enter the QCD amount on line 4(c)(3), whether or not the financial institution indicates a “Y” in the box 7 (Distribution Code) on a 2026 1099-R form. I just can’t see showing the net IRA distribution (i.e., gross distribution minus the QCD amount) on line 4b without also checking the box on line 4(c)(2) and enter the QCD amount on line 4(c)(3).

John F says

And your recommendation is incorrect. Box 3 has nothing to do with QCD. It has to do with a HSA funding distribution (HFD). Read Exception 4 on page 27 and Line 4c on page 28 and I quote “If Exception 4 applies to you, check box 3 on line 4c and enter ‘HFD’ in the entry space next to box 3”.

marvin says

if you have $2,000,000. in an rollover ira,does it make sense to leave 50 percent to wife and 50 percent to 2 children,to lessen children’s tax , they are in high tax states with income over $300,000. I value your opinion. thanking you in advance.

MTG says

I’ve been doing Roth Conversions to avoid taxes in the future while Federal Income taxes are on sale now. If I pass before my wife, she becomes an individual, rather than joint tax filer. Our kids are already in a higher bracket than we are. Big picture says convert fast keeping IRMAA in mind.

The Wizard says

Yes indeed, to Marvin.

This wise plan spreads the kids timeline for depleting their inherited IRAs out to longer than ten years, up to twenty possibly.

And the surviving spouse pays less income tax.

This assumes the surviving spouse has plenty to live on without half of your IRA…

Mike W says

Smart move. It might be better to leave less to wife and more to younger children so more can be depleted over their longer lifetime, assuming wife can live on less than 50%, and of course assuming no family issues.

We don’t have any kids so it’s pretty simple for us. Our intent is for the survivor to ‘assume’ the deceased’s TIRA and Roth’s in their name, which will combine both into one TIRA and one Roth, and of course continue to take the normal RMD albeit a much bigger one now that the survivor will be older, single and with a substantial amount to be taxed.

marvin says

thank you , your replies are always appreciated and thoughtful,marvin

Liftlock says

Marvin,

I agree with the others that it might be smart move. However, I would be cautious about reducing your wife’s assets without considering how long your wife might live and how much money she might need if she lives well beyond a normal life expectancy requiring extended assisted living care. My sister is likely to reach her 104th birthday this week and she needs 24 /7 in home care. The costs of in home care is a tidy sum and the family has become concered about her out living the financial assets available to care for her.

If your kids are high income earners they should be fine without an early inheritance of half of your IRA. One of the unintended economic consequences of the 10 year distribution rule for inherited IRAs is that it may cause productive citizens to retire earlier than might otherwise be the case and become unproductive contributors to society.

MTG says

If someone decides to retire because they have sufficient $ for whatever reason, there is a great opportunity to be a “productive citizen” through volunteerism. Retirement usually also opens a paid position for someone else.

tjk144 says

Another factor to consider in addition to the difference in tax brackets of the suriviving spouse vs children is the estate tax in your state. The estate tax in Illinois where we live is very punitive. If the value of your estate exceeds $4 million, the first $6 miiion (not just the amount over $4 million) is taxed at 5%. Between $6 million and $16 million is taxed at 10%. Thus there is great incentive to get the estate of the surviving spouse under $4 million to avoid the 5% tax on everything up to $6 million. Having the childen inherit 50% of your IRA is one way to accomplish this.

tjk144 says

Bob — While New York’s estate tax is bad, I would gladly take it over Ilinois’ where the cliff starts at $4,000,000.01. Plus any amount gifted over the annual exemption that requires a gift tax return filing reduces this amount dollar for dollar. Also Illinois has the highest real estate taxesin the nation. Just a horrible state to live in. Pritzker and his democratic cohorts have driven it into the ground. Unfortunately I was born here and If I didn’t have so many family ties here, I would move to another more tax friendly state that was more in line with my conservative political views.

Bob says

John. The procedures presented on pg 27 of the 1040 instructions are similar between Exception 3 (QCD distribution) and Exception 4 (HSA/HFD distribution).

Exception 3 is for a QCD distribution and it says: “If all or part of the distribution is a qualified charitable distribution (QCD), enter the total distribution on line 4a. If the total amount distributed is a QCD, enter -0- on line 4b. If only part of the distribution is a QCD, enter the part that is not a QCD on line 4b unless Exception 2 applies to that part. Check box 2 on line 4c.”

The line 4c instructions on pg 28 says: “If Exception 1 applies to you, check box 1 on line 4c. If Exception 3 applies to you, check box 2 on line 4c. If Exception 4 applies to you, check box 3 on line 4c and enter “HFD” in the entry space next to box 3.”

Therefore, it appears that box 3 on line 4c is to indicate “HFD”, rather than my prior comment to enter the QCD $ amount in box 3 on line 4c. In conclusion, if a taxpayer has both a QCD and an HFD, he/she would check box 2 (QCD) on line 4c and also indicate “HFD” in box 3 on line 4c.

The instructions on pg 28 goes on to say “If more than one exception applies, check a box for each exception and include a statement showing the amount of each exception, for example, “Line 4b – $1,000 Rollover and $500 HFD.”

Bob says

tjk144. Estate taxes in New York are also punitive. For deaths in 2026, the New York estate tax exemption is $7.35 million per individual . Estates exceeding this threshold are taxed at progressive rates from 3.06% to 16%. New York has a “cliff” provision: if the estate exceeds the exemption by more than 5%, the exemption is lost entirely, subjecting the whole estate to tax.

Key Aspects of NY Estate Tax:

The “Cliff”: If an estate is valued at 105% or less of the exemption, taxes only apply to the excess. If it exceeds 105% (e.g., above \(\approx\$7.7M\) in 2026), the entire estate is taxed from the first dollar.

Tax Rates: Graduated from 3.06% to a maximum of 16%.

Gifts: While NY has no gift tax, gifts made within three years of death are included in the taxable estate.

Non-Residents: Non-residents owning real or tangible personal property located in New York may owe estate taxes.

Portability: NY does not have federal-style portability, meaning a deceased spouse’s unused exemption is lost if not properly planned for (e.g., via a credit shelter trust).

marvin says

can’t spread kids withdrawals beyond 10 years

The Wizard says

Sort of.

Parent #1 passes and wills each kid $200k IRA, remainder to surviving spouse. Kids have 10 years to empty the inherited IRA.

12 years after #1 death, parent #2 passes and wills each kid a percentage of the remaining IRA. Kids start a new 10-year clock to empty that inherited IRA…

Jeff Enders says

Wizard – what is the logic of the approach?

who is expected to have the higher tax bracket? surviving spouse or children?

The Wizard says

To Jeff,

The logic is based on allowing the “children” to deplete their combined tIRA inheritance over a period longer than the standard ten years, up to twenty years in some cases…

Jeff Enders says

Wizard, but if the children are in a higher tax bracket than the surviving spouse, what is the benefit?

yes, they can deplete it over more than 10 years, but if the children pay higher taxes, then why do it especially if there is absolutely any risk of the surviving spouse running out of money?

If the children are in a higher tax bracket, wouldn’t it be better for the surviving spouse to inherit the whole TIRA, which increases the chances that when the surviving spouses passes, the children are closer to their own retirement, and presumably their own lower tax rate?

I’ve just never seen any one else pose the benefit of creating two 10 year RMD streams. o I don’t understand the logic.

The Wizard says

If the married couple is basically broke or are barely breaking even in retirement, then it makes zero sense to plan on any early disbursement to heirs, correct.

But if they have $10 Million or more in financial assets, the situation is different.

Specific details matter…

JoeTaxpayer says

And, if the couple is in-between, not broke, but not enough to want to let half go when one passes, it’s not all-or-none.

Couple can make use of Roth conversions to top off the lower brackets each year, mitigating the damage their kids will face.

Or – easy to split the beneficiary so the kid(s) get a portion on death of first spouse, but living spouse gets the rest.

Agree, 100% with Wizard, the details matter, both for the couple, and the kids.

ros says

I did a direct transfer this year in March. Will this affect my but that is how the credit union policy regularly did it if you did not wire it. Will this affect my income for IRMAA. I did not touch my the check. It was sent to the new institution.

The Wizard says

You’re not giving us enough info to understand what you did .

You mention a credit union, so was this a checking account from which the money came?

And then what was the destination: the custodian and the type of account?

Richard says

Are you talking about a direct transfer from a traditional to another traditional or a direct transfer from a traditional to a Roth?

Ros says

The credit union deposited the check in a checking account I use once a year for my RMD. They made out a cashier check to the other instituion as a tradtional IRA for the benefit of me and the traditional Ira and the CD account number it could be added to. Years ago when I did this I checked a box that it was added to another IRA at tax time. But I have been on Medicare for many years now and I don’t want to be in IRMAA. Will this count as a income even though this was a direct transfer and I did not touch the check. It was a cashier check and they wrote it out and they mailed it. Both were in other states. I am quite elderly and combining accounts.

Harry Sit says

So you had involved 3 institutions: institution A, institution B, and the credit union. If institution A sent a check payable to institution B for the benefit of you, it would have been a direct transfer. Because you put your checking account at the credit union in the middle, it was an indirect rollover.

It’s still not taxable unless you had taxes withheld from institution A, but you only get to do an indirect rollover once every rolling 12 months. I hope you hadn’t done the same in the previous 12 months.

And be careful not to do it indirectly again too soon. Work with A and B alone. Don’t put the credit union in the middle.

The Wizard says

Your RMD always counts as Ordinary Income and having it sent to your checking account is normal.

But you cannot contribute money to either type of IRA unless you have earned income from employment, which I’m guessing you probably do not.

You also cannot do a rollover of your RMD into either type of IRA; that RMD money generally needs to stay in your taxable account.

So this traditional IRA contribution or rollover is likely illegal…

Richard says

Are you talking about a direct transfer from a traditional IRA to another traditional IRA or a direct transfer from a traditional IRA to a Roth IRA?

ros says

Both instituions has it designated as a direct transfer when I wrote and ask and them in my PM. My question is –will this box be able to be checked as a direct transfer and not count of income for IRMAA on my tax return.

I did not ever have taxes taken out. I always do the RMD in Dec. I have enough taxes automatically taken out of other income even 25% of my SS is taken out. I have a certain fixed amount taken out of other income for federal taxes and have always had a refund for over 60 years. Only had to pay state taxes twice. This year I sent in a check to pay the state income taxes for the first time all at once for the year because no taxes are taken out of pensions now because everyone this year does not pay state taxes on pensions and I have a lot of interest.

Harry Sit says

You can’t rely on side communication because people often misunderstand each other. Only the 1099, or lack of it, will show officially how it’s treated.

Doing RMD in December is a bad habit when you will also do other things with an IRA. As previously discussed, the first sums coming out of an IRA in a year are considered to be the RMD. Do the RMD and QCD in January and get it over with. Then you’re free to do other things.

The Wizard says

Harry is correct. You must complete your RMD obligation on a tax-deferred account before you can legally do a direct rollover from that account to a new custodian or do a Roth conversion from that account.

I’m in a similar situation and complete my quarterly RMD in mid October which gives me time at year-end to plan additional transactions…

Lou says

This is incorrect. Direct rollovers or transfers from one institution to another can be done anytime. Indirect or 60-day rollovers, however, can only be done after your RMD is satisfied.

tjk144 says

Lou is correct. With a direct transfer, no funds are leaving your IRA and can be done before or after an RMD is taken.

The Wizard says

I disagree…

Lou says

It’s easy to look up. If you do, you will see that you are wrong.

tjk144 says

When you do a direct transfer (where the money moves directly between financial institutions), the IRS does not view this as a “distribution.” Because no money was actually paid out to you, the “RMD-first” rule that applies to rollovers does not apply here.

The Responsibility Moves: When you transfer the funds, your RMD obligation moves with it. The new custodian will eventually need to know the December 31st balance of the old account from the previous year to help you calculate the correct RMD amount for the current year.

The Deadline Stays: You still must ensure the total RMD amount is withdrawn from the new account (or another IRA you own) by December 31, 2026.

Lou says

Thank you tjk144 for this correct response.

Ros says

Richard,

I was going from a mature traditional IRA in a credit union to another credit union that I can add it to a traditional IRA I have at that credit union. I will take my RMD in Dec as I have since I had to start taking it years ago and when it is put in my checking account it that 2nd credit union if my income allows I will do my roth conversion. They also allow me to put the conversion in a Roth IRA I have with them which I will do if if the rate I have is better than the rate they have at the time and if they do no have a higher rate at that time many times I can add my RMD to the newer rate and many times they have put the older CD and the Roth conversion together with no penalty. Last year they did all the CD’s I had with them at the higher rate. But they do not do that every year. I have been converting every year since they allowed it in the 2011 income and did the Roth’s at work for both my husband and I when my company started the Roths and did it for the 10 years to 2008 when I had to retire to care for my disabled husband 24 hours a day. I did the traditional IRA’s for me and a spousal IRA for both of us since 1978 until my work started the Roths and the 401k when my employer started it.

When my husband was working he also did the 15% in the 401k when they started it the 1080’s and his company employees voted to be self insured and he started working there in 1965 or 1966 and all the employees put in the same amount per hour worked in that pension and when they retired each hour of each year was paid on the amount for that year for each hour worked. Double time you put in double and that was counted as double hours in the pay out. He loved his job and had 30 years of actual working when they put him on 100% disability and he had 43 pension years in when it was calculated.

Richard says

OK I just wanted to make sure there were no implicit assumtions we were making.

Direct transfer form traditional to traditional would not run afoul of any rules. Direct transfer from traditional to Roth must be done AFTER you have made the RMDs.

Gary Egnasko says

Harry – Any updates on how Gov’t will be treating the missing October CPI data points for social security, federal tax brackets or IRMAA brackets? For my spreadsheets, I am using the average of the September and December indices as a guesstimate. Any better insights would be appreciated.

Harry Sit says

I haven’t seen anything new from government sources. I suspect they will use a straight average of the available 11 months for federal tax brackets and IRMAA, which produces a higher average and generates fewer complaints.

Social Security isn’t affected, because it uses Q3 averages. October 2025 was in Q4.

Tom P says

In late April I received the following in an email from the Bureau of Labor and Statistics:

BLS has engaged the National Association for Business Economics (NABE) and the Committee on National Statistics (CNSTAT) to conduct expert panels regarding approaches for handling missing October and November 2025 Consumer Expenditure data from the 2025 lapse in appropriations and its impact on the Consumer Price Index. These meetings will take place May 7 and May 8, 2026, and they are open to the public.

Big-Pops61 says

Seems to me that the easiest way would be to follow the same methodology that the treasury used to fill in the missing refcpi values for TIPS. The formula used has been around for a while, long before this happened. A little surprising (not really) that the BLS didn’t already have something codified for just such a case.

https://www.treasurydirect.gov/files/laws-and-regulations/auction-regulations-uoc/auct-reg-gsr-31-cfr-356.pdf#page=17

Harry Sit says

Thank you, Tom P. This page has links to the meeting recordings on YouTube.

https://www.bls.gov/cex/notices/2026/missing-ce-data-impact.htm

Experts only give opinions and suggestions. They don’t make decisions.

Richard says

Thanks. I had not seen anything about that, I wonder what the general consensus there was.

Looking at the undelying legislation I cannot see that the people setting the IRMAA thresholds have any authority other than to take the average of the 11 figures unless the BLS itself publishes a missing figure. Howver if a figure for October 2025 is generated I suspect that, as set out in https://www.bls.gov/cpi/factsheets/approximating-missing-data.htm it would be the geometric average of the September and November figures, which would give 324.461 rather than the 325.604 that the TIPS method gave.

The method used for TIPS would, IMV, be wholly inappropriate. For TIPS what matters is not accuracy or precision but rather a method that gives a figure NOW with any problems that causes being dealt with by the next proper figure coming out. The reason speed over accuracy is important is because TIPs are traded on a day to day basis with the purchaser “buying” part of the next month’s interest payment, so that figure needs to be known before the publication of any subsequent month’s CPI figure. You can see this in the fact that whenever a provisional CPI figure is released, that figure is used and the revised figure is not substituted in any later calculations. The need for immediate certainty trumps anything. The method for TIPS, just inflating the previous month’s figure by the average of the last 12 months gives a good “quick and dirty” figure for immediate use. However where the point is to make a calculation later it is not the best method because it ignores some highly pertinant later data.

Big-Pops61 says

In the case of refCPI, there was not an immediate need for speed to plug October 2025, since daily refCPI is calculated as a linear extrapolation of 2 month’s prior CPI-U numbers from the BLS. In this case, the first REFCPI calculated based on October (and November) numbers was January, 2026

It is true that the October estimated number wasn’t needed for as long as numbers are needed for IRMAA, tax brackets, etc. since the Feb 1st refCPI is based on November & December published CPI-U.

Richard says

> A little surprising (not really) that the BLS didn’t already have something codified for

> just such a case

It is not BLS’s job to have provisions for what happens if it is prevented from doing its job: it is the job of those who rely on the BLS’s figures being available to have provisions for what happens when they are not; in this case the people who administer Medicare and those who drafted the regulations. The people at the Treasury did their job (in part) by having provisions about what to do for TIPS, but interestingly, have no provisons about what to do about income tax, where various threshholds are also linked to the CPI. The people at Medicare dropped the ball completely (or maybe considered the point and reckoned that just taking the average of what figures were available was good enough).

The BLS did try to help by saying what the best method of interpolation is, but really that is about all that they can do when circumstances prevent them from generating a figure.

Keith says

I will turn 73 this year. Will my brokers send me a notice about RMD’s?

The Wizard says

You betcha!

Jeff Enders says

Keith – whether the brokers sends you a notice or not, you are responsible for the RMD – not the brokers.

Since you know you have a responsibility to take the RMD, curious why you are asking the question.

Take your 12/31/25 IRA balance across all your Trad IRA accounts and divide by 26.5, that is your RMD.

Richard says

They probably will but even if they do you still have some work to do. As was said above why wait though. Whether they send you info or not it is still your responsibility to take the correct amount.

Firstly do you have IRAs and 401ks? RMDs apply to both but with some differences.

For 401ks, each is treated individually, you have to calculate the RMD for each one separately and take amounts from each. For traditional IRAs you add together the balance at the end of the previous year divide that by (probably but see below) 26.5. That is your total RMD from IRAs . You do not have to spread it between the IRAs but you can, if you wish, take it all from one traditional IRA and leave the others untouched. Also if you make qualifying charitable distributions *directly from the IRA after you turn 73* they count towards the RMD requirement.

As for the amount to divide the year end balance by, it will be 26.5 unless you are married and your spouse is more that 10 years younger than you, in which case there is a different table to use.

JoeTaxpayer says

You said “brokers”, plural.

Keep in mind –

401(k) have a separate RMD from IRAs. But IRAs can be combined, 2025 year end value, and withdrawal, calculated on that balance, taken from any of the IRA accounts.

And – withdrawals can be “in kind”, taken as shares of the stocks or funds you hold.

Last – once that RMD is made, it’s time to look at your year end forecast and (maybe) use a Roth conversion to ‘top off’ your current tax bracket mindful of the IRMAA cliffs as well.

The Wizard says

26.5 is the correct RMD divisor for age 73, yes, but it gets smaller each year after that, so probably better to print a copy of that table or know where to find it.

And you can do QCDs at age 70.5 (not 63) and even before you are of RMD age …

Richard says

Yes the divisor changes each year so keep an eye on that. The year end balance changes each year too so the calculation will need to be completely redone each year.

QCDs can be made at any time after you hit 70½ (if made directly from the IRA) but they count towards meeting the RMD requirement only once there is a requirement.

Jeff Enders says

Harry – can you please comment on the Part D IRMAA projections in the new Medicare Trust fund report? See page 208 (table V.E.4). It appears the tranches percentages* change DRAMATICALLY in 2030. What is driving this change? (and if I compare back to the same table in the 2025 report, the Part D IRMAA charges beginning in 2030 are ~50% higher than projected a year ago)

https://www.cms.gov/oact/tr/2026

https://www.cms.gov/oact/tr/2025

*35% tranche becomes 100%

50% tranche becomes 200%

65% tranche becomes 300%

80% tranche becomes 400%

85% tranche becomes 433%

if my math is correct, my current $83 / mo. Part D IRMAA charge is projected to be $207 / mo. in 2030!

so much for the $2100 annual drug cap!

Hopefully, I am incorrect on some of this – please set me straight!

GeezerGeek says

I guess that the law, that limited the increases to a maximum of 6% per year, expires in 2030.

A lot can change in 4 years. With the ever-increasing national debt and with Social Security’s main reserve fund projected to be depleted by the end of 2032, a lot will have to change.

I really didn’t anything to say but I wanted to change my email address on this topic, so I made this comment just for that purpose. 😉

Harry Sit says

When the 6% cap on the increase in Part D base premium expires in 2030, enrollees must pay a minimum of 20% of the program cost. Table V.E2 shows that the projected base premium is $68.93 in 2030, which means that the program cost is projected to be $68.93 / 0.2 = $344.65 per month. When people in the first IRMAA tier must pay 35% of the program cost, they’ll pay $344.65 * .35 = $120.63. The surcharge (or reduction in subsidy) over the base premium is $120.63 – $68.93 = $51.70, which matches the number in Table V.E4.

Enrollees were supposed to pay 25.5% of the program cost but the 6% cap on the increase made them pay lower than that percentage. IRMAA amounts in recent years still pretended that the base is paying 25.5%. People in the first IRMAA tier paid less than 35% as well. When the base changes to 20% to get closer to reality, the gaps between the base and the IRMAA tiers become larger.

Harry Sit says

P.S. Assuming the 20% floor will hold in 2030, the multipliers for Part D at each income tier becomes 1.75x, 2.5x, 3.25x, 4x, and 4.25x in 2030 and beyond, not our familiar 1.4x, 2.0x, etc. for Part B.

Rick says

Harry, without reading the 271 page report, in 2030 will the multipliers for Part B also become 1.75x, 2.5x, 3.25x, 4x, and 4.25x? In your opinion, how likely is it that the 20% floor will hold?

Thanks in advance.

Harry Sit says

You don’t have to read the whole thing (I didn’t). The premium projections and discussions are on pages 207-213 of the 2026 report (pages 213-219 of the PDF, because there are 6 unnumbered pages at the beginning). The Trustees are political appointees, but they have subject-matter experts working for them. We should believe them when they say it will be 20% in 2030 and subsequent years (bottom of page 148). This only changes the multipliers for Part D. Part B multipliers won’t change, as you will see in Table V.E3 on page 209 over the base premiums in Table V.E2 on page 207.

To be clear, Part D IRMAA multipliers apply to a national average, not to the specific Part D plan you choose.

Rick says

Harry, thanks VERY much for your comprehensive response. Even if this only applies to the Part D multipliers, it will require a re-evaluation of my Roth conversion strategy. Using Jeff’s numbers, in 2030 the Part D IRMMA charge will increase by $124 per month per person, or about $3,000 annually for a couple. That extra cost may be enough for me to decide to either reduce my Roth conversions or discontinue them entirely after 2027, given the 2-year income look-back. I suppose another option would be to finish my Roth conversions over the next two years (2026 and 2027) but that’s a tough nut to swallow. It looks like I need to do a lot more number crunching, once again.

Thank goodness for your website, Harry.

Jeff Enders says

Rick – I too was taken aback by the increases for Part D IRMAA and I reviewed my Roth Conversion approach (I have detailed spreadsheets so faily easy to play “what if”.)

part of my analysis is how much would be expected to remain in my T-IRA in 10 years (and for sake of argument and simplicity I assume both my wife and I die that year). Since the remaining T-IRA will be left to our children and they would only have 10 years to liquidate what remains, it’s still advantageous for me to continue my Roth conversion plan, even though my Part D IRMAA payment would go from $2,000 in 2026 to a projected $5,000 in 2030.

if we stop conversions, then the tax my kids pay on a much higher T-IRA balance that they inherit (and it would push them into higher tax brackets), far exceeds the additional IRMAA (plus federal income tax)I would pay from 2030 forward.

Like you, I figure I have as late as Dec 31, 2028 to determine my Roth conversion scheme for 2028 as it would impact 2030 IRMAA. (you state through 2027, but you technically could make a decision as late as Dec 31, 2028 and either do conversions or not do conversions for that year). Maybe by that time Congress may have decided what they are going to do about SS shortfall and that could be part of my decision-making process as well. We’ll also have updated estimates on projected Part D (and Part B) IRMAA tranches.

RobI says

Hi Harry. Any updates expected for June 10 May CPI which showed a step up?

Harry Sit says

The post was already updated on June 10 with the May CPI report. If your browser is showing you a cached previous version, please try the Incognito/Private mode.

Bart Rice says

So thankful that I read your site. It gave me the knowledge to know that a Fidelity Viewpoints article today (6-25)titled “What to know about the new $6,000 Senior deduction” incorrectly stated that MAGI for IRMMA includes non-taxable Social Security. I tried to get them to fix it but ran into a brick wall.

Jeff I says

I really appreciate that you provide this useful information. The July 14, 2026, zero-inflation estimates for the 2028 IRMAA are slightly lower than the estimates from the previous month. So the actual IRMAA bracket could be lower than the zero-inflation estimate. The zero-inflation estimate is not the worst-case scenario.

Harry Sit says

0% inflation means prices staying at the current level through August 2027 for the 2028 numbers. The previous projections were based on prices staying at the then-current levels, with the effect of the Iran war.

Prices came down in June after the ceasefire. The current projections are based on prices staying at the post-ceasefire levels through August 2027.

The war is flaring up again, and the projections next month may go back up.

It really depends on the starting point. 0% from a low starting point is more conservative than 0% from a high starting point.

Jeff Enders says

Jeff I – these estimates are NEVER the “worst case scenario”! nothing says that inflation can’t be negative (i.e. deflation!). It simply answers the question, “if inflation was zero from TODAY until August, what would the IRMAA tranches look like?”

“TODAY” is reset each month as we get an actual figure to replace an estimated figure.

ros says

I thought the inflation rate for July, August and September of 2026 were compared for the same months of 2025 but could change through August of 2027 before the 2028 rate for Medicare would be decided.

Jeff Enders says

Ros- I wonder if you are confusing a number of different terms and measurements:

1) The increase in social security benefits is based on the average consumer price index (CPI-W Urban Wage Earners) for July, August and September of 2026 compared to the same three month average from 2025. The Senior Citizens League currently estimates that COLA increase will be 3.8%, which would increase SS benefits by 3.8% for 2027.

2) The increase in Medicare premiums is based on the Medicare Trust Fund assessment of what is needed to cover the costs of Medicare. Its June report estimated the 2027 monthly Medicare premium would be $209.50 for Part B and $41.33 for Part D. This would be the base premium before any IRMAA charges if their estimates hold.

3) IRMAA is based on the average CPI for the 12 months ending in August, 2026 compared to the base period from 2017-2018. That formula defines the 2027 IRMAA tranches. This website currently presents what the 2027 IRMAA tranches would be: there are 9 months of actuals and 2 months of estimates remaining to lock in the 2027 IRMAA tranches which are applied to your 2025 MAGI (because of the government shutdown last year, one month was never reported). The 2028 IRMAA tranches will be based on the reported inflation from Sept, 2026 – August 2027 and will be applied to your 2026 MAGI.

does that help?

Ros says

Jeff, I was and did and thank you for setting me straight.

Gary says

Jeff – Is there anything officially published yet, as to just how they will be responding to the missing month of CPI data across Federal Tax and IRMAA brackets? Harry takes one reasonable approach for his estimates, but only the Gov’t can tell us for sure.

Jeff Enders says

Gary – I am not aware of anything other than what Harry wrote. However, why would it matter? We are locked in to our 2025 MAGI in any event, so 2027 IRMAA will be what it will be and there is nothing we can do about it. Am I missing something?

The Wizard says

What you’re missing is that we’re focusing on 2026 MAGI at this point, and 2028 IRMAA…

Jeff Enders says

Wizard – That missing data point causes uncertainly in how the index from Sept, 2025 – August 2026 plays out. And that average is bounced against the 2017-2018 base line. THAT is used for the final 2027 IRMAA tranches, which uses 2025 MAGI. And we are locked in to 2025 MAGI.

For 2028 IRMAA, it’s uses the 12 data points from Sept 2026 – August 2027 and compares that to the 2017-2018 baseline, and short of another government shutdown or similar fiasco, there will be 12 datapoints!

While we may be focused on 2026 MAGI, because it is still something we can control, the issue of the missing datapoint from Oct 2025 affects 2027 IRMAA – not 2028 IRMAA.

Again, am I missing something?

Harry Sit says

If someone is preparing a 2027 budget, knowing whether they will pay IRMAA helps, even though they can’t change the 2025 MAGI now.

Gary says

Thanks to everyone for responding. I am sensitive to both 2027 & 2028 IRMAA & Federal tax brackets, as I project personal income statements, balance sheets and tax returns for future years in my own financial modeling spreadsheets. As part of this modeling, I also plan future Roth Conversions.

Your discussion made me look closer at the potential impact of the missing data point, and I confirm that 2027 IRMAA brackets are sensitive to this data point while 2028 is immune. Fortunately, my 2025 MAGI currently has a $6,000 buffer, so I should be fine. The 2027 Federal Tax Brackets could change, but it is a rather small cost which is beyond my control at this point anyway.

However, I have learned that 2028 IRMAA brackets are immune, so my 2026 Roth Conversion can be planned with one less uncertainty. Thanks everyone for opening my eyes!

The Wizard says

I’ve been using IRMAA projections from this site for years to plan my year-end Roth conversion, a quite modest one nowadays.

My goal is to stay in the 2.6x IRMAA tier which tops out at $211k or $212k for 2025 MAGI filing Single based on latest numbers. I forget what it was projected to be last December when I did my small Roth conversion for the year but it must have been roughly the same, for the 0% case at least.

My MAGI for 2025 was ruffly $207,500 so I should be fine for 2027 IRMAA, regardless of that missing month.

I’ll repeat the process again in less than five months…

Gary says

Wiz, we also stay just below the 2.6X tier, but it’s more of a choice thing for us. Even though we are 73 now (how did that happen so fast?), we are pushing extra Roth Conversions to move up an extra tier.

Our best projections show this aggressive strategy as a slight overpay of expected future costs. However, there is also many potential risks to future costs due to higher: federal and state taxes, IRMAA brackets, medical inflation, surviving spouse tax rates on early death and lastly, our usage of conservative investment returns in our modeling. Any of these would create much higher Tax/IRMAA costs. So we view the overpay as an “insurance premium hedge” that reduces future exposure for us and/or our heirs.

Jim M says

Gary, similar thoughts here. Tax brackets are “permanent” only while this party is controlling. Medical costs continue to exceed forecasts thus creating larger IRMAA surcharges. My spreadsheet forecasts (confirmed by Boldin) show a “pay taxes now” strategy will save low six figures in combined tax, IRMAA and NIIT before I’m 95. Keeping a 5K buffer below my target tier as security from going over the cliff.

GeezerGeek says

Gary, Wiz, Jim M, et al

It is reassuring to see others following the same Roth conversion strategy that I have been using.

I began doing Roth conversions in 2011, initially converting only enough each year to reach the top of my current income tax bracket. In 2018, after the Trump-era tax cuts took effect, I increased my conversions to bring my income close to the threshold of the first IRMAA bracket, thereby avoiding any IRMAA surcharge.

In 2022, I adjusted my strategy again, converting enough to bring my income close to the beginning of the second IRMAA bracket. My reasoning was that it made sense to convert more while the lower tax rates remained in effect, even if it meant paying the first-tier IRMAA surcharge.

Last year, 2025, was the first year I had to take Required Minimum Distributions (RMDs). Because the RMD itself pushed me into the second IRMAA bracket, I converted up to the bottom of that bracket. This year will be similar, although Qualified Charitable Distributions (QCDs) I’m making are creating a little additional room for Roth conversions.

At some point, I may increase my QCDs enough to move into a lower IRMAA bracket. For now, however, I use my RMD to cover my entire annual tax bill rather than deal with quarterly estimated tax payments. As a result, any QCD strategy has to leave enough of the RMD available to pay those taxes. If that becomes a problem in the future, I could begin withholding federal taxes from my pension and Social Security payments, since I currently have no withholding from either source. One way or another, I intend to avoid making quarterly estimated payments.

Some subscribers to this column do not believe Roth conversions are a good idea, but I think the decision depends entirely on an individual’s financial circumstances. Personally, I believe higher tax rates are inevitable. The U.S. Government Accountability Office (GAO) projects that the national debt will grow roughly twice as fast as the economy over the next decade, a trend that economists widely consider unsustainable. In my view, that makes future tax increases, particularly for higher-income taxpayers, likely.

In addition, Medicare premiums have been rising much faster than inflation, suggesting that future IRMAA surcharges could become significantly more costly. For me, the choice comes down to a simple question: pay the taxes now, or risk paying substantially more later.

As Willie Sutton reportedly said when asked why he robbed banks, “Because that’s where the money is.” I suspect future tax policy may follow the same logic and increase taxes on higher-income taxpayers “Because that’s where the money is.”

GeezerGeek says

Correction: As you might suspect, where I said “I converted up to the bottom of that bracket” in the fourth paragraph, I meant “I converted up to the top of that bracket”.

Jeff Enders says

GeekGeezer: curious what your “end game” is, meaning who receives the remaining value after your passing?

I think that question is frequently overlooked in the assessment of whether to do Roth Conversions. My modeling suggests that if your children are going to inherit the remaining Trad/ 401k balance, assuming a 5% increase in the balance each year after they inherit, they would have to distribute around 13% of each year’s remaining balance so the Inherited IRA is liquidated about evenly each year in the prescribed 10 years. THAT could put THEM into an even higher tax rate than we are paying today (even assuming no change in the tax laws).

agreed everyone’s financial situation is different and one size can not fit all.

On the other hand, if the remaining balance is ALL going to charity, I would have a multitude of questions about the rationale to do Roth Conversions today.

On Medicare: here is the annual expected base premium for the next 5 years as reported in this year’s Trust Fund Report. Note the big jump in Part D comes 2030. First number is Part B and then Part D premium.

2027: $209.50; $41.33

2028:$ 229.50; $43.81

2029: $238.50; $46.44

2030: $255.50; $68.93 (the Part D multipliers also change so IRMAA would be around DOUBLE the 2029 charge)

2031: $272.10; $71.27

LiftLock says

GeezerGeek,

I’m in the 24% marginal income tax bracket and am following a similar Roth IRA conversion as you are. My marginal income tax bracket is unlikely to ever fall below the 24% and my analysis indicates there is no downside to doing Roth conversions well into the 24% bracket if that’s the case. I agree with your assessment about the risk of tax rates moving higher and I view Roth conversions a hedge against that possibility. My annual Roth conversions are relatively small since I stated RMDs which have grown in size. I design my Roth conversions to keep my MAGI just below the bottom of the next higher IRMAA bracket to avoid or delay the time when the rates in the next higher IRMAA bracket will apply. A significant stock market correction would cause me to become more aggressive with my Roth IRA conversions. I currently have 67% of my IRA assets in T-IRA and 33% in a Roth IRA, having started with nothing in my Roth IRA when I retired 11 years ago. I don’t consider living beyond age 90 when evaluating the economic viability of doing Roth conversions as I view that as a lower probability event. If I am lucky enough to live beyond age 90, I will be happy to pay higher taxes if they should come.

Jeff Enders,

Requiring heirs to distribute Inherited IRAs within 10 years may prompt some of them to retire earlier than might otherwise be the case if the 10 Year distribution rule were not in place. Depends on the circumstances of the persons inheriting the IRA. So that may not drive some heirs into higher tax rates.

Lou says

Have you ever considered they could not only increase tax rates in the future but could could also start taxing Roths for taxpayers with AGI over a certain threshold. If the debt and the deficits become unsustainable, this would be a logical place to look for revenue. They could rationalize it by saying they are only taxing so-called rich people.

Jeff Enders says

Lou – I don’t believe they would consider taxing Roths – it’s after tax money and to tax it upon distribution would be double taxation. (Wasn’t that clearly resolved with the British 250 years ago?) However, what I do believe they could do, and it came up a few years ago but died in committee, is limit the size of the Roths.

In essence they could create rules to force distribution once a Roth pierced a certain dollar threshhold. (A few years back a $5 million cap was debated). While that doesn’t create taxable income per se, it does move dollars from the Roth to non-qualified accounts where the dividends and any future capital gains would be taxed.

Another devious approach could be that Roth distributions are added to MAGI for IRMAA purposes. It would not change the income tax collected, but would increase the money provided to support Medicare by forcing more into higher IRMAA tranches. Not a lawyer or a politician so not sure whether that is even legally possible. Just an idea.

Lou says

Jeff, agree about the double taxation but they could start taxing all dividends and interest in the Roth Accounts.

GeezerGeek says

Jeff, my “end game” is mixed.

1. I have no kids but lots of relatives who would appreciate an inheritance.

2. Charities. I have been financially fortunate and I am sharing with the less fortunate. We really have little control of who we are or of our circumstances. The idea of a self-made man is an egotistical myth. I’m not denigrating individual accomplishments because those should be lauded, but accomplishments are not possible without opportunity.

3. Me! Of course I can’t take it with me, but no one knows what their future needs will be. My Roth accounts can meet that need without any undue tax consequences.

So you might say my end game is flexibility, and a substantial Roth account balance gives you a lot of flexibility. Still, even with all of the conversions I’ve done, the balance of my traditional IRAs continues to grow. Roth and traditional split is about 33% Roth and 67% traditional.

In addition to the retirement accounts, there are additional assets that have to be considered for my end game. Retirement accounts are about a third of my net worth, highly appreciated stocks held for decades are about another third, and the remainder is diversified taxable assets, except for 5% in real estate, my house. The highly appreciated stocks are also great options for inheritance and charitable donations.

As for Medicare, I have more than ten years history of the Trustees Annual Report, which I started downloading a few years ago. With the exception of the Part D Premium, which is legally pegged to an increase of no more than 6% increase for the next 3 years, the actuals can vary significantly from the projections. The 2022 increase for the Part D premium was one of the worst missed projections when the premium was increased more than 14% from the previous year instead of a less than 7% that was projected on the 2021 report. That increase was a bit of an anomaly because the anticipated impact of a new Alzheimer’s drug but there have been other double-digit increases. My point was that the percent increases have been more than the rate of inflation, and certainly more than Social Security increases, even with the Hold Harmless rule kicking in a few times. Thus, in the future, the IRMAA penalty becomes, relatively, a bigger penalty than currently.

Gary says

One possible way to increase taxes that makes some sense to me is to expand RMD requirements. While RMDs use a minimum age 73 today, a rule change would require RMDs annually for large accounts at any age (e.g. $2M, $5M, $10M, $50M, etc.). Current RMD tables would be extended for any age, with smaller annual requirements for earlier years. The taxing logic would be that IRAs were created to help average people save, not to subsidize “large” accounts. This RMD approach could be applied to both TIRA as well as Roth accounts.

My wife and I are defending against this by judicious Roth conversions to equalize both of our accounts. Since IRAs are administered per person, this might minimize the chance that one of us could hit some selected “large” account size.

Jeff Enders says

LOU: here you go! Bill introduced in Congress this week to limit IRAs to $10 million, so the debate is back in Congress again.

“More than 1,000 individuals had IRA balances of at least $25 million in 2024…..Those with $10 million or more in IRAs also rose, to about 11,600 people” – per the article below.

https://www.wsj.com/personal-finance/retirement/iras-startup-insiders-retirement-accounts-millions-ea9ecab7?st=WGoSPC&reflink=desktopwebshare_permalink

Lou says

Jeff, I read that article and apparently these accounts are mainly ones where the owner contributed private held share in companies they owned or just founded. I guess the way to do it is convert an existing IRA to a Roth and buy the shares with the cash in the Roth. Obviously, you are buying them for pennies on the dollar so you can buy a significant amount of shares. I don’t think this would raise much money for the government since there aren’t many of these accounts. Again, I think they ultimately will take away some of the tax benefits for Roth accounts with owners who make over a certain AGI, probably a few hundred thousand dollars.

Ros says

Jim, I also use a $5,000 buffer and I think maybe this year or next year we will not be sorry for not converting more to a Roth for our kids who are the retirement age.

GeezerGeek, I also started my conversions with 2011 income, but I have 25% tax taken out of my SS, and 85% taken out of my pension and 2/3rd’s taken out from my husband’s for tax and medical insurance. We get the RMD’s in the middle of DEC.

I figure out our income July for the first 6 months of the year and then just double it and add our RMD and again in Nov. to double check and the first week of DEC and decide what we will do our conversion for and stay $5,000 below IRMAA. I don’t pay attention to the tax bracket. We always get a refund, though this year the pensions stopped taking state tax out so I just wrote a check out for the year a couple hundred over the amount we paid last year as a buffer.

GeezerGeek says

Ros,

I suspect that by using tax withholding from Social Security and pension income to cover your tax liability, you’re also avoiding Quarterly Estimated Payments (QEPs). That strikes me as a smart approach. As I’ve mentioned before, I may eventually incorporate that strategy as well because it would give me more flexibility in managing RMDs. I just want to avoid making QEPs, which I had to do for several years before I started taking RMDs.

I maintain a spreadsheet that tracks my projected annual income and update it throughout the year as dividend estimates change or other significant income events occur. However, I usually wait until November, when the first version of FreeTaxUSA becomes available, before making an initial plan for how much of my RMD to withhold for taxes and how much to convert to a Roth IRA.

My spreadsheet also estimates my tax liability and generally matches the FreeTaxUSA calculation exactly. On rare occasions, the difference is only a dollar or so, which I assume is due to a rounding discrepancy somewhere in the formulas.

Because some of my Vanguard dividends ( VT) are not announced until late December, typically around the 22nd, I postpone my final calculations until then. As a result, I usually take my RMD and complete any Roth conversions during the last week of December. Any QCDs are completed earlier in the year and are reflected in the adjusted RMD amount.

For tax withholding, I generally target a small refund, usually around $200, when I file my return in late February. I also try to keep my MAGI approximately $3,000 below the next IRMAA threshold. That cushion helps protect against IRMAA estimation errors and provides room for roughly $1,000 of unexpected income without crossing into a higher IRMAA bracket.

I won’t know until I receive my Forms 1099 what portion of my municipal fund dividends will ultimately be taxable. Fortunately, that uncertainty affects only my income tax calculation, since all municipal fund dividends are included in IRMAA MAGI regardless of their federal tax treatment.

I currently live in Tennessee, so state income taxes are not a factor in my planning. However, I’ll be relocating to North Carolina next year, which means I’ll need to incorporate state tax considerations into my calculations going forward.

Jim M says

Roz, I found that even without consideration of a legacy for the heirs, making the larger conversions over the next ten years while keeping at/below the 2.6 tier provided a huge tax savings over my estimated lifetime (my family lives into the mid/late 90’s). Having had a career in finance/account, I built a spreadsheet to run the tax savings comparing conversions against no conversions – conversions result in a significant overall tax savings. The tax free legacy is just a bonus to the plan.

I take advantage of market drops to convert more shares at a “discounted” conversion rate and in December, after downloading the dividends, capital gains and interest from the brokerages, true up the spreadsheet for a final conversion to reach the targeted amount.

GeezerGeek says

Jim M,

I used to do Roth conversions during market drops, but since the IRS requires RMDs to be completed before Roth conversions, that is no longer an option. Roth conversions during market drops is a great strategy, as long as you are not required to take RMDs.

Ros says

I see I typed our and I should have type my but I do get 1/2 of my husband’s pension. He has passed many years ago and now and then I still will type our. I try to stay below the lowest bracket for single. Being in all CD’s and a large MM and still stay 100% insured and chase rates for the IRA’s and am down to my last traditional IRA becasue I discaimed all of my husband’s when he passed and a large account I had for someone to care for him if I died first. Interest rates have been fairly high and I just figures my income for the year and am $3500 below that figure. I usually try to stay below $5,000 but I doing my 6 month projection I will be only $3,500. Good thing is I have a CD that will mature the first of Oct and I can put it in a non interest bearing account and put $10,000 in

I-bonds, and save $1,900 income and also I can save another 3 months interest for my MM and save another $900 if I put that in zero interest also. I do not like this much uncertainity in the economy. My other CD’s do not mature until 2028 and 2029. I We and now I have gifted our children after they graduated college since the early 1990’s and I still do every Jan. In this environment I hope that is enough to cut. I have always been extremely risk adverse, having a disabled husband for 17 years and working 2 jobs, with 2 children in college. I have always planned for the worst and actually it never happened. The children worked during the summer. One worked 96 hours a week and one worked 107 hours a week. Both are professionals and old enough to retire.

I don’t know how good AI is but just did a google with AI and that printed out this- –

To lower the first Medicare IRMAA bracket threshold for a single filer from a projected $114,000 down to $111,000, the annual inflation rate measured for that year would need to decrease by 2.63%. [1, 2, 3, 4, 5]

Because IRMAA brackets are directly pegged to the Consumer Price Index for All Urban Consumers (CPI-U), any change to the thresholds requires a direct mathematical shift in the calculated inflation factor. [1, 2]

Understanding the Math

The Formula: The annual bracket adjustment is determined by multiplying the previous base threshold by the year-over-year percentage change in CPI-U. [1, 2]

The Decrease: Moving from $114,000 down to $111,000 represents a drop of exactly $3,000.

The Required Drop:

\(\frac{111,000-114,000}{114,000}\times 100=-2.63\%\) [1]

Critical Structural Context

Annual Rounding Rules: By law, IRMAA thresholds are rounded to the nearest $1,000increment. This means inflation doesn’t just have to trend slightly lower; it must drop enough to pull the rounded calculation down into the lower $1,000 tier. [1, 2, 3]

The Two-Year Lookback: The IRMAA bracket for any given year is determined by your Modified Adjusted Gross Income (MAGI) from two years prior. For example, the official $111,000 single tier established for 2027 is dictated by the inflation adjustments calculated on income reported on 2025 tax returns. [1, 2, 3]

Deflation vs. Low Inflation: Because thresholds shift based on cumulative economic data, moving a bracket backward usually requires a period of true economic deflation (a negative CPI-U reading) rather than just a “cooling off” of standard inflation rates.

I am surely over reacting to the economy but being in a situation we are in with the oil reserves is very conserning along with more bombing. But then again that would cause more inflation. I just remember working in the bank for 30 years what my customers went through in the 1980’s and it taking 90% of the people 7 years to be even with what they had in 2007 after the banking crash. I don’t like bills and even pay garbage in Dec for year. I wrote a check for my state income tax for the year when I realize the tax had stopped being taken out of a penion check.

Jim M says

GeezerGeek, that’s an excellent point. I still have a couple of years before my RMD‘s kick in. That’s another reason to take your RMD early in the year.

GeezerGeek says

Jim,

I agree, with a few caveats. If possible, take your RMD when the market is relatively strong and do Roth conversions when the market is down. Historically, the market is more likely to be higher 11 months from now than it is today, so the odds generally favor waiting until December to take the RMD.

That said, if the market appears unusually elevated and a correction seems likely before year-end, it may make sense to take the RMD earlier and hope the decline occurs before completing the Roth conversion. One important consideration is the relative size of the two transactions. If the RMD is substantially larger than the Roth conversion, you could be risking a larger loss on the RMD than the potential benefit gained from converting at lower market values.

When I was still contributing to my 401(k), I would increase my contribution percentage during market downturns to buy more shares at lower prices. Most of the time that worked out well. However, during the Great Recession, the market continued to decline after I had already maximized my annual contribution, so in hindsight I would have been better off spreading those purchases over a longer period. Market timing is always a gamble, even when the odds seem favorable.

Of course, if you’re relying on RMDs for current income, the calculation changes. As with most financial strategies, there’s no one-size-fits-all solution.

Ros says

When both IRAs and 401(k)-type balances are taken into account, the 200 or so Americans who had amassed $100 million or more in 2024 accounted for a total of $85.1 billion in assets, for an average balance of $409 million, the joint committee concluded in its analysis for Wyden and Neal. Another 31,887 people held more than $10 million in their IRAs and 401(k) accounts at the end of 2024, the research estimated.