[The next update will be on August 12, 2026, when the government publishes the CPI data for July 2026.]

Seniors 65 or older can sign up for Medicare. The government refers to people who receive Medicare as “beneficiaries.” Medicare beneficiaries must pay a premium for Medicare Part B, which covers doctors’ services, and Medicare Part D, which covers prescription drugs. The premiums paid by Medicare beneficiaries cover about 25% of the program costs for Part B and Part D. The government pays the remaining 75%.

What Is IRMAA?

Medicare imposes surcharges on higher-income beneficiaries. The theory is that higher-income beneficiaries can afford to pay more for their healthcare. Instead of doing a 25:75 split with the government, they must pay a higher share of the program costs.

The surcharge is called IRMAA, which stands for Income-Related Monthly Adjustment Amount. This applies to both Traditional Medicare (Part B and Part D) and Medicare Advantage plans.

According to a Medicare Trustees Report, less than 10% of Medicare Part B beneficiaries paid IRMAA. The extra premiums they paid reduced the government’s share of the total Part B and Part D expenses by two percentage points. Big deal?

History of IRMAA

IRMAA was added to Medicare by the Medicare Prescription Drug, Improvement, and Modernization Act of 2003. The Republican Congress under President George W. Bush passed it in November 2003.

IRMAA started with only Part B. The Patient Protection and Affordable Care Act, passed in 2010 by the Democratic Congress under President Obama, expanded IRMAA to also include Part D.

The Bipartisan Budget Act of 2018, passed by the Republican Congress under President Trump, added a new tier for people with the highest incomes.

IRMAA has been the law of the land for over 20 years. Different congresses and administrations from different parties made small tweaks, but its structure hasn’t changed much since the beginning. IRMAA has become a bipartisan consensus. There’s no impetus for major changes.

MAGI

The income used to determine IRMAA is your Modified Adjusted Gross Income (MAGI) — which is your AGI plus tax-exempt interest and dividends from muni bonds — from two years ago. Your 2024 MAGI determines your IRMAA in 2026. Your 2025 MAGI determines your IRMAA in 2027. Your 2026 MAGI determines your IRMAA in 2028.

There are many definitions of MAGI for different purposes. The MAGI for ACA health insurance subsidies includes 100% of the Social Security benefits. The MAGI for IRMAA includes taxable Social Security benefits, but not untaxed Social Security benefits. If you read somewhere else that says that untaxed Social Security benefits are included in MAGI, they’re talking about a different MAGI, not the MAGI for IRMAA.

You can use Calculator: How Much of My Social Security Benefits Is Taxable? to calculate the taxable portion of your Social Security benefits. The new 2025 Trump tax law didn’t change how Social Security is taxed. It didn’t change anything related to the MAGI for IRMAA. See Social Security Is Still Taxed Under the New 2025 Trump Tax Law.

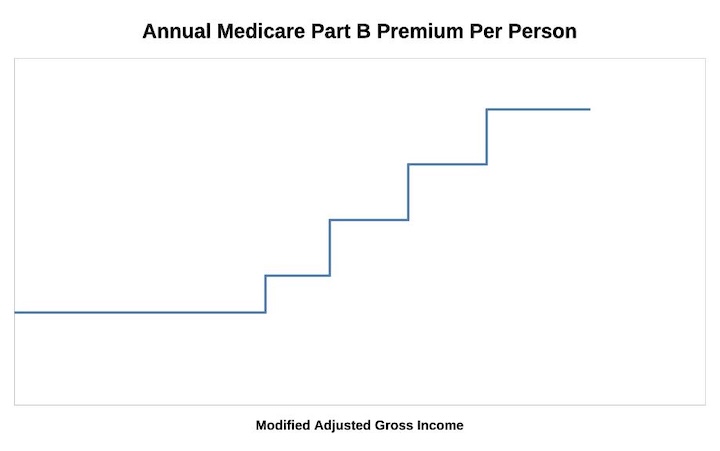

As if it’s not complicated enough, while not moving the needle much, IRMAA is divided into five income brackets. Depending on the income, higher-income beneficiaries pay 35%, 50%, 65%, 80%, or 85% of the program costs instead of 25%. As a result, they pay 1.4, 2.0, 2.6, 3.2, or 3.4 times the standard Medicare premium.

The threshold for each bracket can cause a sudden increase in the monthly premium amount you pay. If your income crosses into the next bracket by $1, your Medicare premiums can suddenly jump by over $1,000 per year. If you are married and filing a joint tax return, and both of you are on Medicare, $1 more in income can make Medicare premiums jump by over $1,000/year for each of you.

* The last bracket on the far right isn’t displayed in the chart.

If your income is near a bracket cutoff, try to keep it low and stay in a lower bracket. Using the income from two years ago makes it more difficult to manage.

2026 IRMAA Brackets

The standard Part B premium in 2026 is $202.90 per person per month. The income on your 2024 federal tax return (filed in 2025) determines the IRMAA you pay in 2026.

| Part B Premium | 2026 Coverage (2024 Income) |

|---|---|

| Standard | Single: <= $109,000 Married Filing Jointly: <= $218,000 Married Filing Separately <= $109,000 |

| 1.4x Standard | Single: <= $137,000 Married Filing Jointly: <= $274,000 |

| 2.0x Standard | Single: <= $171,000 Married Filing Jointly: <= $342,000 |

| 2.6x Standard | Single: <= $205,000 Married Filing Jointly: <= $410,000 |

| 3.2x Standard | Single: < $500,000 Married Filing Jointly: < $750,000 Married Filing Separately < $391,000 |

| 3.4x Standard | Single: >= $500,000 Married Filing Jointly: >= $750,000 Married Filing Separately >= $391,000 |

Source: CMS news release

Higher-income Medicare beneficiaries also pay a surcharge for Part D. The IRMAA income brackets are the same for Part B and Part D. The Part D IRMAA surcharges are relatively lower in dollars.

I also have the tax brackets for 2026. Please read 2026 Tax Brackets, Standard Deduction, Capital Gains, QCD if you’re interested.

2027 IRMAA Brackets

We have nine data points right now out of the 11 needed for the IRMAA brackets in 2027 (based on 2025 income).

If annualized inflation from July through August 2026 is 0% (prices staying flat at the latest level) or 3% (approximately a 0.25% increase every month), these will be the 2027 numbers:

| Part B Premium | 2027 Coverage (2025 Income) 0% Inflation | 2027 Coverage (2025 Income) 3% Inflation |

|---|---|---|

| Standard | Single: <= $112,000 Married Filing Jointly: <= $224,000 Married Filing Separately <= $112,000 | Single: <= $112,000 Married Filing Jointly: <= $224,000 Married Filing Separately <= $112,000 |

| 1.4x Standard | Single: <= $141,000 Married Filing Jointly: <= $282,000 | Single: <= $141,000* or $142,000 Married Filing Jointly: <= $282,000* or $284,000 |

| 2.0x Standard | Single: <= $176,000 Married Filing Jointly: <= $352,000 | Single: <= $176,000* or $177,000 Married Filing Jointly: <= $352,000* or $354,000 |

| 2.6x Standard | Single: <= $211,000* or $212,000 Married Filing Jointly: <= $422,000* or $424,000 | Single: <= $211,000* or $212,000 Married Filing Jointly: <= $422,000* or $424,000 |

| 3.2x Standard | Single: < $500,000 Married Filing Jointly: < $750,000 Married Filing Separately < $388,000 | Single: < $500,000 Married Filing Jointly: < $750,000 Married Filing Separately < $388,000 |

| 3.4x Standard | Single: >= $500,000 Married Filing Jointly: >= $750,000 Married Filing Separately >= $388,000 | Single: >= $500,000 Married Filing Jointly: >= $750,000 Married Filing Separately >= $388,000 |

Some of the projected 2027 brackets are the same for 0% inflation and 3% inflation due to rounding. The unrounded numbers for 3% inflation are higher, but not high enough to break into the next level after rounding.

If you’re married filing separately, you may have noticed that the 3.2x bracket goes down with inflation. That’s not a typo. If you look up the history of that bracket (under heading C), you’ll see it went down from one year to the next. That’s the law. It puts more people married filing separately with a high income into the 3.4x bracket.

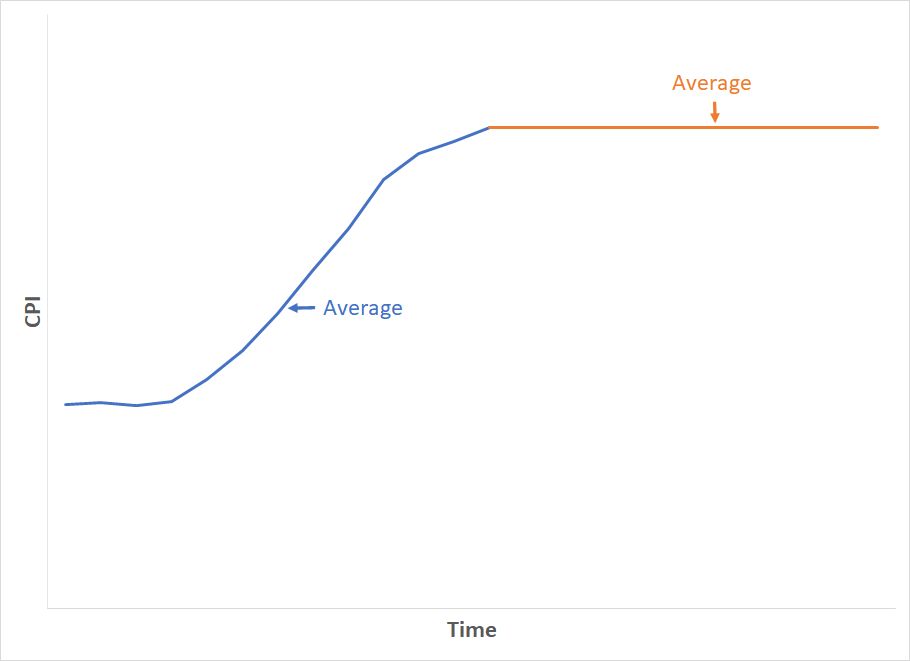

Because the formula compares the average of 12 monthly CPI numbers over the average of 12 monthly CPI numbers in a base period, even if prices stay the same in the following months, the average of the next 12 months will still be higher than the average in the previous 12 months.

To use exaggerated numbers, suppose gas prices went up from $3/gallon to $3.50/gallon over the last 12 months. The average gas price in the last 12 months was maybe $3.20/gallon. When gas price inflation becomes 0%, it means it stays at the current price of $3.50/gallon. The average for the next 12 months is $3.50/gallon. Brackets based on an average gas price of $3.50/gallon in the next 12 months will be higher than brackets based on an average gas price of $3.20/gallon in the previous 12 months.

If you really want to get into the weeds of the methodology for these calculations, please read this reply on comment page 2 and this other comment on page 4.

The Missing October 2025 CPI

The government did not and will not publish the CPI number for October 2025 because it didn’t collect the necessary price data during a government shutdown. It’s unclear how the Social Security Administration will calculate the 12-month average with only 11 data points.

The Treasury Department used 325.604 as the October CPI to calculate interest on inflation-indexed Treasury bonds. The Social Security Administration won’t necessarily use the same number for IRMAA. I calculated the projected 2027 brackets in two ways: (a) using a straight average of the projected 11 monthly data points, omitting October 2025; and (b) using 325.604 for October 2025. The projected 2027 brackets are largely the same under the two methods due to rounding. I put an asterisk on the number calculated by method (b) where they differ.

2028 IRMAA Brackets

We have no data point right now out of the 12 needed for the IRMAA brackets in 2028 (based on 2026 income). We can only make preliminary estimates and plan for some margin to stay clear of the cutoff points.

If annualized inflation from July 2026 through August 2027 is 0% (prices staying flat at the latest level) or 3% (approximately a 0.25% increase every month), these will be the 2028 numbers:

| Part B Premium | 2028 Coverage (2026 Income) 0% Inflation | 2028 Coverage (2026 Income) 3% Inflation |

|---|---|---|

| Standard | Single: <= $114,000 Married Filing Jointly: <= $228,000 Married Filing Separately <= $114,000 | Single: <= $116,000 Married Filing Jointly: <= $232,000 Married Filing Separately <= $116,000 |

| 1.4x Standard | Single: <= $143,000 Married Filing Jointly: <= $286,000 | Single: <= $146,000 Married Filing Jointly: <= $292,000 |

| 2.0x Standard | Single: <= $179,000 Married Filing Jointly: <= $358,000 | Single: <= $183,000 Married Filing Jointly: <= $366,000 |

| 2.6x Standard | Single: <= $214,000 Married Filing Jointly: <= $428,000 | Single: <= $219,000 Married Filing Jointly: <= $438,000 |

| 3.2x Standard | Single: < $507,000 Married Filing Jointly: < $760,500 Married Filing Separately < $393,000 | Single: < $517,000 Married Filing Jointly: < $775,500 Married Filing Separately < $401,000 |

| 3.4x Standard | Single: >= $507,000 Married Filing Jointly: >= $760,500 Married Filing Separately >= $393,000 | Single: >= $517,000 Married Filing Jointly: >= $775,500 Married Filing Separately >= $401,000 |

Effect of the Iran War

The CPI numbers in recent months were affected by the volatile energy prices due to the Iran war. The most recent data point reflects the market’s hope that the war would end following a ceasefire and a preliminary deal. The 0% inflation numbers assume that prices will stay at the current level. Energy prices can rise sharply if the war drags on. If that happens, CPI numbers in the upcoming months can escalate beyond the 3% inflation estimate, which may push the IRMAA numbers above the projections.

Roth Conversion Tools

When you manage your income by doing Roth conversions, you must watch your MAGI carefully to avoid accidentally crossing one of these IRMAA thresholds by a small amount and triggering higher Medicare premiums.

I use two tools to help with calculating how much to convert to Roth. I wrote about these tools in Roth Conversion with TurboTax What-If Worksheet and Roth Conversion with Social Security and Medicare IRMAA.

Nickel and Dime

The standard Medicare Part B premium is $202.90/month in 2026. A 40% surcharge on the Medicare Part B premium is $974/year per person or $1,948/year for a married couple both on Medicare.

In the grand scheme, when a couple on Medicare has over $218,000 in income, they’re already paying a large amount in taxes. Does making them pay another $2,000 make that much difference? It’s less than 1% of their income, but nickel-and-diming just makes people mad. People caught by surprise when their income crosses into a higher bracket by just a small amount are angry at the government. Rolling it all into the income tax would be much more effective.

Oh well, if you are on Medicare, watch your income and don’t accidentally cross a line for IRMAA.

IRMAA Appeal

If your income two years ago was higher because you were working at that time, and now your income is significantly lower because you retired (“work reduction” or “work stoppage”), you can appeal the IRMAA initial determination. The “life-changing events” that make you eligible for an appeal include:

- Death of spouse

- Marriage

- Divorce or annulment

- Work reduction

- Work stoppage

- Loss of income from income producing property

- Loss or reduction of certain kinds of pension income

You file an appeal with the Social Security Administration by filling out Form SSA-44 to show that although your income was higher two years ago, you have a reduced income now due to one of the life-changing events above. For more information on the appeal, see Medicare Part B Premium Appeals.

Not Penalized For Life

If your income two years ago was higher and you don’t have a life-changing event that makes you qualify for an appeal, you will pay the higher Medicare premiums for one year. The IRMAA surcharge goes into the Medicare budget. It helps to keep Medicare going for other seniors on Medicare.

IRMAA is re-evaluated every year as your income changes. If your higher income two years ago was due to a one-time event, such as realizing capital gains or taking a large withdrawal from your IRA, your IRMAA will decrease automatically when your income comes down in the following year. It’s not the end of the world to pay IRMAA for one year.

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

Robert Hoppe says

Great job Harry and Jeff on the Temporary Senior Deduction section of the Financial Bluff. Very helpful! When I saw the SSA email the other day stating discontinuance of federal income tax on Social Security benefits under the BBB, I immediately sent a reply to the SSA Press office to let them know they are incorrect and I explained the background on that topic. Since the Republican Party in the House voted for a 50% (vs 60%) majority vote to pass the BBB, this meant that income taxation cannot be part of the bill in relation to Social Security. This is why Congress came up with the Temporary Senior Deduction concept to help compensate seniors for all these years in which we paid income tax on Social Security benefits.

Jeff Enders says

Robert – thx for the ‘shout out’ and just an FYI….. the income tax collected that is related to SS goes to the Medicare and SS Trust funds and NOT to the general treasury fund. Any attempt to reduce the tax on this line item just accelerates the challenges of keeping both benefits funded. That was another reason why Congress went for this new deduction versus a direct reduction of what portion of SS is subject to tax.

Further, the rationale is the SS income that is subject to tax now was never taxed in the past. It’s the interest that was generated on the investment of the funds over time. Yes, we were taxed on our paychecks so our FICA contributions were aftertax monies, but we are (theoreticially) not being taxed a second time on the same dollar.

Patrick says

Jeff,

But I didn’t know Harry’s site existed in 2024. In any case, it is ridiculous and unfair for the government to force seniors to fool around with their income because of some very poorly designed “cliff tax” or as I call it, a step function tax. Surely we must all agree that the IRMAA tax should be graduated, like the IRS does it, generally in $50 increments, and not IRMAA’s $28,000 (and more) increments. Furthermore, rounding the thresholds to the nearest $1000 is incredibly lame. The Medicare Modernization Act (which includes IRMAA) was introduced in the House of Representatives on June 25, 2003, and sponsored by Speaker Dennis Hastert, who admitted he was a child molester and who was also found guilty of a structuring charge (a felony). Not surprised.

Henry Waldron says

Be careful what you wish for. In our current financial situation, where politicians are doing everything possible to reduce the deficits implicit in the new “Big, Beautiful Bill”, you may find your wish fulfilled, but with Medicare costs ramping up from a much lower level of income. As it stands very few Social Security recipients pay any IRMAA surcharge, so the fact it is a consideration (for you) puts you in a rarefied income situation. And all of us are paying a steep discount to what Medicare actually incurs. Most retirees, unlike us, have little or no flexibility in terms of income recognition in a given year. The 35% of Social Security recipients who already don’t pay any income taxes will be heavily penalized by the new tax structures, especially if monthly payments drop sooner and by more than currently projected. I can at least construct a financial vehicle from taxes saved to construct an annuity that will defer the effect of any 2033 (or 2034) loss in Social Security income until closer to 2040.

Jeff Enders says

Patrick – Henry stated it best. Nothing more to add.

Patrick says

Henry, Jeff,

I don’t so much object to the IRMAA tax per se, but I object strongly to the way it has been implemented. BTW, I do not worry about Social Security going bust after 2034, or decreasing benefits for those already getting them. It is easy enough for the government to raise the payroll tax, and also end the upper limit of Social Security tax which is currently at $176,000. Ending tax on all Social Security income also would provide more income for those who currently pay federal tax on Social Security income. The threshold below which you do not pay such a tax has not changed since the mid-1970s. It should at least have gone up by the cost of living! BTW, my financial situation has no bearing on my arguments or suggestions. I do not try to guess your incomes, nor do I care what they are.

tom says

I agree. One of the problems with IRMAA is that if much of your income

Is from IRA distributions, or capital gains, you are just guessing as to how much to take, because, for example, you don’t know exactly what the brackets will be in 2027 for tax year 2025, due to inflation adjustments, which you don’t find out about until 2027.

So if you miscalculate and take just a small amount more than what is optimal, then you run the risk of going over into the next IRMAA bracket, triggering a big increase in monthly premiums. I have had that experience more than once.

Mike F says

Thanks to Harry Sit for his insights! The Big Beautiful Bill has been passed into law now. Does that change any of the IRMAA brackets in the tables above?

Jeff Enders says

@Mike F – it does not.

IRMAA brackets are predicated on AGI (Line 11) and Tax Exempt Interest (Line 2a) of the tax return.

Neither line is impacted by the BBB.

Ros says

Can the amounts for 2025 for income brackets change after 12/31/ 2025 and affect our Medicare premiums in 2027?

The Wizard says

They certainly can!

IRMAA tiers for 2027 will not be finalized until August of 2026…

Jeff Enders says

@Ros – are you asking whether the IRMAA limits can change after 12/31/25 for 2027?

the answer to this question us “yes”, since the inflation rate through August, 2026 determines the IRMAA brackets to be used in 2027.

That is the whole purpose of Harry’s webpage – to help guide everyone’s expectation given that we “lock in” to our AGI by 12/31/25 yet the IRMAA limits do not lock in until the August, 2026 CPI is published.

David Swanson says

What are the details of any deduction on your tax return for 2025 (filed in 2026) for charitable contributions, if you do not itemize deductions, as a result of the Big Beautiful 2025 Bill?

DBS

Harry Sit says

No such deduction is allowed in 2025. It only starts in 2026, and it doesn’t affect MAGI or IRMAA.

Jeff Enders says

David – for 2025 tax year (filing early 2026), there are no changes for charitable contributions in the BBB.

My understand for 2026 tax year (filed early 2027), if not itemizing you would be able to deduct up to $1,000 (Single) and $2,000 (Joint) of charitable contributions. Also, if you do itemize, .5% of your AGI would be subtracted from the charitable contributions that are eligible for SCH A.

JoeTaxpayer says

This might be a good place and time to remind people of QCD. The ability to make a charitable deduction directly from your retirement account if you are 70 1/2 or older.

For those who don’t have enough deductions to itemize it effectively as a deduction of your charitable donations. The donation made from the IRA is not part of your taxable income. If you were going to withdraw say $10,000 and have $2400 in tax due, Donating directly to the charity avoid this.

Whenever I mention this on social media, people are quick to point out that there’s no free lunch and that “throwing away $10,000“ to save $2400 doesn’t make sense. They missed the point 100% this advice is only for people who are going to make the donation anyway. Just wanted to clarify that.

Patrick says

Thanks Harry, Jeff, Wizard, Tom. I will eat it, but just for one year. Not much I could have done about it even if I knew of Harry’s site. I probably would have put money in a zero interest checking account. Still, I argue that IRMAA is very very poorly implemented, and it is grossly unfair to force seniors to try to fool with their income two years in advance of IRMAA tax implications (I see IRMAA as a tax, like any other tax).

JoeTaxpayer says

I agree with you for many reasons.

First, the nature of how IRMAA is calculated, a series of cliffs, no phasing, creates some situations where the next dollar of income triggers an extra $1000+ of premium.

And, for the fact that these cliffs do not match up with marginal rates is absurd, in my opinion. TBH I don’t know what’s fair anymore, as I’ve been told that my SALT deduction should be capped, or eliminated completely, but the $25M+ couple shouldn’t pay a dime in estate tax. Because the average person can really relate to leaving a fortune behind.

Bev says

Wholeheartedly agree with Patrick about IRMAA. It is an additional tax, just as the NIIT 3.8% Medicare surtax is. That is two additional tax “contributions” to the Medicare system. And, the $200,000/$250,000 income threshold is not indexed for inflation either.

ERNEST kRAMER says

I believe that with some self restraint and accurate forecasting you MAY be able to avoid the IRMAA. Just remember, pigs get fat, hogs get slaughtered and keep a reasonable buffer amount under the IRMAA.

Nancy Memmel says

I don’t think the intention was to “force seniors to fool with their incomes”, the idea was just for seniors who had more income to pay up!

The SSA can’t access more timely tax data, since one can delay filing taxes for a given year until Oct of the following year, then the IRS has to process the return before the info can get to the SSA. So the 2 year lag was programmed in. Seniors who have the sufficient income to be nailed by IRMAA take it upon themselves to try to mitigate the tax bite, if they have any sense. The government would much prefer you not to bother.

Robert H says

Joe, Trump’s OBBB bill signed on 7/4/25 increased the SALT deduction (starting this year) from $10K to $40K. The $40K cap will increase by 1% per year through 2029 and then revert to $10K in 2030. Also, the OBBB indicates that the federal estate tax exemption has been increased from $13.99 million per person ($27.8 million per couple) to $15 million per person ($30 million per couple), and this is permanent.

Dennis McFall says

I appreciate all the comments previously submitted. One thing that really sticks in my craw is the stated purpose of the IRMMA which is to have those in higher income brackets pay more for Medicare (Means Testing.) If this is the case, why then does the person who withdraws $100,000 from a Roth not have to participate in the RMAA debacle? They already receive the benefit of not paying income tax on their Roth money. In addition this same money is then excluded fromThe Means Testing relative to IRMAA. When I started an IRA in 1975 the Roth was not available and to convert at that time would have resulted in a heavy tax bill (OK, tough some of you say) but my point is the inequity in the treatment of income as it relates to IRMAA. If I end up with the same income as the Roth participant he doesn’t pay income tax or an additional IRMAA component on his Roth related income which technically is the same as mine. So much for means testing.

tom says

My Roth has been entirely funded via SEP-IRA distributions. The first year

that I took a SEP-IRA distribution to fund the Roth, I was 66, and didn’t

realize what an effect it would have on both my income tax liability,

and my IRMAA liability. At the time, I wasn’t even familiar with IRMAA.

So, that year I took a large distribution, and ended up paying a substantial

amount of IRMAA two years later. So, I learned my lesson, and have been

very careful to limit my IRA distributions so that I can mitigate my IRMAA

liability.

But over the years, I have made some minor miscalculations that have

caused me to cross over into the next higher IRMAA bracket, which is

a painful experience.

John says

Instead of weakening Roth

I’d like to see IRA distributions and Roth conversions excluded from MAGI for Medicare. Using your own savings is NOT income.

I agree, have those with true high ‘income’ pay more, but using your own savings is NOT income. The present setup discourages people from saving for retirement, and in my opinion, is morally wrong.

While yes, we should pay taxes on it, (albeit it should be taxed as long-term capital gains, not ordinary income) — it should not affect our Medicare rates.

Now that the Big Bill is law, and it didn’t really help seniors, I’d like to see a congressional committee try to right this wrong. Anyone game to help approach the right Committee (via your representatives) ??

I’d like the ability to work up cost estimates for such a change, but I lack access to the data that would be necessary to do so. Also, in my opinion, this should have taken priority over $1000/kid born and no tax on overtime or tips.

MrPG says

“They already receive the benefit of not paying income tax on their Roth money“

Well, I certainly paid income tax on my Roth contributions. Not sure how this computes…

Nancy & Gary Memmel says

They paid tax at the point the Roth was either funded ( no taxable income reduction in the first place) or the conversion to Roth was done (converted amount included in taxable income in the year of conversion). If you chose not to pay tax at an earlier point then you made your choice since this is how the program works.

The Wizard says

Good luck with that…

tom says

Ditto, I have paid plenty of income tax on the SEP-IRA distributions that I have taken. I’ve placed the net distributions amounts into my Roth IRA account. Hence, I don’t see where it would be fair for the government to charge me for taxes whenever I take a distribution from my Roth IRA account in the future.

Jeff Enders says

ditto.

Roths were established by the Taxpayer Relief Act of 1997.

IRMAA was established by the Medicare Modernization Act of 2003.

Congress had full knowledge on how Roth’s worked in 2003 and with that knowledge decided that the basis of IRMAA would simply be AGI plus tax-exempt interest. My point is Congress had the opportunity to add Roth distributions (plus whatever else they wanted to add in) to determine how IRMAA was to be calculated and decided not to do so.

and they have had 20 years to rejigger it. They have not.

I do not see what the issue is. And if there is one, please write your Congressperson!

Lou says

Yeah, but why should you not pay tax on the interest income or capital gains, just like everyone else does with after-tax contributions to IRA accounts.

Jeff Enders says

Lou – I am assuming you are asking why dividends and capital gains occuring in Roth accounts, which are by definition are from after-tax contributions, are not taxed upon distribution* the way dividends and capital gains are taxed upon distribution from Trad IRA accounts which could include the same after-tax contributions. The answer is because that is how Congress traded time versus tax collection in the law. It was willing to wait for its tax, but the tradoff is everything above the cost basis is subject to income tax.

On a Trad IRA, you are incented to contribute PRE-TAX dollars and then pay income tax on ALL distributions above your cost basis, including any interest, dividends, capital gains that occured over time. The Government is willing to wait for its tax dollars but the trade is everything over your cost basis is taxed upon distribution.

On a ROTH IRA, you are incented to contribute AFTER-TAX dollars and in return, there is NO* income tax on the distributions, whether they be interest, dividends or capital gains that accured along the way. The Government gets its tax money up front and the trade is in return, you are not taxed upon distribution*. The Government is NOT willing to wait ror its tax dollars and the trade is that there is no further tax upon distribution*.

If you are suggesting that is “unfair” that there is no income tax on interest and dividends and capital gains that accurred in a Roth IRA when there is in a Trad IRA, that is “on you” for putting after-tax dollars into a Trad IRA. With Conversions from a Trad IRA to a Roth IRA, that could have been rectified “years ago” before all the interest, dividends and capital gains grew in the Trad IRA. If you did not take advantage of the laws as written, again, that is “on you”.

*assuming you are over 59.5 years old and the Roth has been open for at least 5 calendar years.

tom says

I agree. The system, as it is currently set up is fair. It would be unfair to change it to include Roth distributions in the IRMAA calculation.

Ros says

Budget bill likely to hurt most seniors’ finances- – Harry what do you know of this and does this article mean income frozen on 2023 income for this years Medicare premium, or on this years income for 2027’s Medicare premium. Would be nice if we had some information on what his law is and what it means or we could get my congressman’s office to even answer the phone or unlock his office door so someone can ask questions. Can’t get any answer from my congressman who voted for it.

https://www.ctinsider.com/waterbury/opinion/article/social-security-federal-budget-20775475.php

• IRMAA thresholds for Medicare premiums will remain frozen through 2029, meaning more middle-income seniors will face higher surcharges due to inflation. IRMAA is the Income-Related Monthly Adjustment Amount—a surcharge to Medicare premiums when a retiree’s income exceeds certain thresholds. ($300-$1,500)

Harry Sit says

A person wrote a letter to a newspaper with misinformation. Please ignore.

tom says

Yes, and interestingly, we have been told by the administration and congress that there is something in the one big bill for “Everyone”. Unfortunately, there is absolutely nothing in it for me. The new $6,000 additional deduction is phased for my income level.

If they had included in the bill the “no tax on social security” that they promised on the campaign trail, I would have benefited nicely.

Ros says

Harry, Thank you

Liftlock says

Tom, I am not a fan of the BBB. But it did extend the lower tax rates that were scheduled to expire and move about 2% higher for upper income earners. It also increased the MFJ standard deduction for 2025 to $31,500 from the $30,000 that was other was previously announced by the IRS in the fall of 2004. The Standard deduction for MFJ in 2024 was $29,200.

I believe the Standard deduction for single filers is half of the above amounts.

tom says

Liftlock,

Yes, you are right, but the standard deduction has been increasing annually since 2018.

I guess I am a bit dismayed by the fact that the campaign promise “no tax on social security” was just a ploy to get the vote of retirees, and what I am finding annoying is that i have been hearing some members of the administration and congress continue to state that the big bill includes “no tax on social security”, which is entirely untrue.

Of course, politicians from both parties often stretch and bend the truth, in order to obtain votes, and I understand that, but I am still wondering why “no tax on tips” and “no tax on overtime” were retained in the bill, and “no tax on social security” was cut out of it. Are retirees considered to be “chopped liver”?

The Wizard says

I never believed the no tax on SS would pass and, sure enough, it did not.

I get over $54,000 in gross SS this year, 85% of which is taxed. So I would need a $46,000 deduction, not $6000, to make my SS not taxed.

And I’m totally phased out of that $6000.

I guess we can be happy that lower income seniors are seeing some benefit here…

Robert H says

Jeff, I’m not clear on what you mean by “on a Trad IRA, you are incented to contribute PRE-TAX dollars and then pay income tax on ALL distributions above your cost basis, including any interest, dividends, capital gains that occurred over time. The Government is willing to wait for its tax dollars but the trade is everything over your cost basis is taxed upon distribution.” Money withdrawn from a traditional IRA (or converted to a Roth IRA) is taxed at the full amount of the withdrawal (or conversion), not on the withdrawal/conversion amount over your cost basis. What you’re describing, in terms of taxability, is a taxable (non-IRA) type brokerage account wherein the capital gain tax is based on the excess of the gross proceeds of a sale over the cost basis of the shares.

The Wizard says

I agree. There are three general types of investment accounts and Jeff is muddling them up…

JoeTaxpayer says

Replying to the wizards comment about Social Security taxation. I never believed the promise that they were going to do away with taxation on Social Security benefits. When I find interesting is that the White House website has a page with a headline basically claiming that they did just this, eliminate the tax on Social Security. Yet, on the same page further down, it shows that the percent of people receiving Social Security that paid tax on some of it will drop from 36% to 12%. In other words, one out of eight recipients will still be paying tax on some of your benefit. And then at the bottom of the website, the obligatory “promises made promises kept.“ Remarkable how this isn’t all over the news as it remains on the White House website to this day.

Harry Sit says

To be clear, the new senior deduction doesn’t affect IRMAA. Please continue the discussion of the senior deduction and the tax on Social Security under Social Security Is Still Taxed Under the New 2025 Trump Tax Law.

Jeff Enders says

Robert H – Lou’s original comment was hard to decipher. What he stated was:

<>

What I took him to mean – and it was not clear – is that the IRA accounts he mentions are Trad IRAs. That where an after-tax contribution causes the interest, dividends and capital gains to be later taxed upon distribution. So when he stated “just like eveyone else does with after-tax contributions to IRAs” he could have only been referencing Trad IRAs; it could not have been a Roth.

I took it that he made after-tax contributions to a TRAD IRA and is now “befuddled” that he has to pay tax upon distribution on the dividends, interest and capital gains that he would not have to do if he had placed the same after-tax contributions into a Roth IRA.

In most cases, the cost basis of a Trad IRA is zero. “cost basis” does not mean at what price you bought a stock / bond for that is inside the Trad IRA. Pre-tax contributions to a Trad IRA have a cost basis of zero. Post tax contributions to a Trad IRA have a cost basis of the contribution. So if all Trad IRA contributions were pre-tax dollars, every dollar that is withdrawn from a Trad IRA is subject to tax because the cost basis is zero.

With that understanding, please re-read what I wrote. Hopefully, it makes more sense now.

Robert H says

Tom. Yes, I also continue to see comments, speeches, and publications (incl from the SSA itself) that there is no longer federal income tax on Social Security benefits, a campaign promise of Trump. The reason why this didn’t happen in the OBBB bill is because the House Republicans decided in May to have a 50% (vs 60%) majority vote requirement in order to pass the bill. By law, federal income tax cannot be addressed with respect to Social Security benefits when there is a 50% majority vote required to pass the bill. Therefore, in order to compensate seniors for having paid income tax on those benefits, the bill introduced the new $6,000 senior tax deduction (65+) which is in addition to the standard tax deduction, whether or not the taxpayer itemizes or takes the standard deduction. The $6,000 is phased out by 6% of every dollar of MAGI that exceeds $75,000 for single seniors or $150,000 for MFJ seniors). This senior deduction can potentially, in effect, reduce your marginal income tax rate which then results in a lower tax calculated (on either 50% or 85%, depending on your MAGI) of your Social Security benefits. This tax is targeted to the Social Security trust fund. The OMB estimates that 90% of Social Security beneficiaries will experience a net benefit with the additional senior deduction, even while continuing to charge income tax on Social Security benefits. I have my doubts that it will be as high as 90%. since this assumes in 90% of the cases that one’s marginal tax rate will be reduced by the $6K senior deduction.

tom says

Robert,

Just my 2 cents….

Everything you say is entirely correct, and well presented.

What irks me is the way this whole thing has, and is still

currently being presented by the administration and some members

of congress.

My feeling is that during the presidential campaign, the campaign

staff was well aware that the OBBB would have to be passed with

a 50% majority. And if they didn’t know it during the campaign,

they had to have known it from the time the president took office

and the time the bill was first introduced in he House, a period of time

during which we heard over and over again, “no tax on social security”.

And now, after the OBBB has been signed, I am still hearing

members of the administration and congress state that the OBBB

contains no tax on social security, which is entirely

untrue.

As I see it, the $6,000 increase in the standard deduction for senior retirees has been advertised as very beneficial for retirees, but it really turns out to be nothing but a very small bone thrown to appease some retired senior taxpayers, in a small way.

As it turns out, higher income taxpayers will not get any benefit

from the deduction, because they are phased out, but, worse yet,

many low income taxpayers will be getting no benefit either.

For example, supposing a single senior retiree receives the average

social security income of $1,611 per month, i.e., $19,322 per year.

Prior to the passage of the OBBB, the standard deduction for

seniors (over age 65) was $17,750. Only 85% (or less) of the

$19,322 social security benefits received is taxable.

So the tax liability for this example (prior to passage of OBBB),

would have been $0, i.e., ($19,322 * 0.85 – $17,750) = -$1,326,

rounded to 0.

With the passage of the OBBB, that person’s tax liability will

also be 0, thus there is no saving at all for that low income

person.

My point here is that it is the retired seniors who have benefitted

the least from the OBBB, and it was known that would be the case

during the campaign, and during the period when the OBBB was

passing through the House and Senate.

Robert H says

Harry. I understand that the primary focus of this forum is IRMAA. However, my comments this morning were in reaction to comments raised on the topic of federal income tax on Social Security benefits. I just wanted to point out what the OBBB bill signed on July 4th actually represents on this topic, including one of the primary reasons for the introduction of the $6,000 additional senior deduction (2025 – 2028) in relation to the topic of federal income taxation on Social Security benefits. I do understand that the senior deduction has nothing at all to do with IRMAA which is based on MAGI.

Robert H says

Jeff. The topic of federal taxation on withdrawals from a traditional IRA (or conversions to a Roth) does relate directly to whether or not the taxpayer claimed a tax deduction for the contributions to the traditional IRA on IRS form 8606 (Non-taxable IRA). In other words, the tax basis for any monies withdrawn from a traditional IRA does relate back to whether the taxpayer claimed a tax deduction for prior IRA contributions. The taxpayer is taxed only on the earnings portion of the withdrawals relating to those non-deductible IRA contributions. IRA withdrawals relating to IRA contributions for which a tax deduction was claimed are fully taxable (principal and earnings) at the federal level. The taxable portion of IRA withdrawals does play a role in the IRMAA calculations, since the taxable portion is part of MAGI. There are states (e.g., first $20K in NY) where a portion of IRA withdrawals are not taxable, no matter whether a tax deduction was taken for the prior IRA contributions.

Robert H says

Thanks Tom. Actually, the senior tax deduction is beneficial in that it does offset to some extent the effect of federal income taxation of Social Security benefits. Here is an example. A MFJ senior couple receives $5,000 per month in Social Security benefits. 85% of this is $4,250. The federal income tax (at 22% marginal tax rate) is $935. Assuming this couple receives a $12,000 ($6,000 each) senior tax deduction, their tax is reduced by $2,640 ($12K X 22%) due to this deduction. Therefore, the couple is ahead tax-wise by $1,705 ($2,640 – $935) in this example. Agreed that not all senior couples are receiving $5,000/month in Social Security benefits, but I believe this is a fair example of how the new senior tax deduction will benefit seniors (as long as their MAGI is under $150K). As I previously mentioned in my comments this morning, the $6K senior deduction will be reduced by 6% for every $ that their MAGI exceeds $150K for the year. Once their MAGI exceeds $250K, the senior deduction is completely phased out.

tom says

Yes, of course. Some will benefit, some will not. Higher and lower income

taxpayers will not, many in the middle will. IMHO, it falls well short of

what is being presented to the public.

Jeff Enders says

Robert H – I am going to make this easier ….

for ANYONE whose ONLY income is SS, they were paying NO TAX on that income prior to the OBBB and they are paying NO TAX now.

What was promised is what was delivered: No Tax on SS.

Robert, the formula to determine what part of SS is not as simple as you presented; the formula is quite complex.

Even if a married couple had $100,000 of combined SS income and no other income, only $11,100 of that SS would be subject to tax. And once the standard deduction of $34,700 was applied, there is nothing left to tax! In fact, there is no tax return filing requirement!

Harry Sit says

Tom and Robert – If you followed comments on the post about the senior deduction and tax on Social Security, you would’ve known that paying tax on Social Security has always been only a result of having income outside Social Security. No other income, no tax on SS. With that perspective, one can say a deduction is really reducing non-SS income and reducing the tax on non-SS income. That’s why I keep pointing to a much better place to discuss it.

https://thefinancebuff.com/social-security-taxed-2025-trump-tax-law.html/comment-page-1#comment-36794

Robert H says

Jeff. How did you arrive at the $11,100 of Social Security income would be taxable, without indicating the portion of the $100,000 that represents SS income? 50% of SS income is added to all other taxable income which, in turn, is compared with either 50% of MAGI or 85% of MAGI (depending on filing status with respect to the MAGI threshold) to determine the portion of SS income that is taxed. While I agree that a senior couple who’s total income is in the form of SS income would not be subject to any federal income tax, I think it’s important to know what portion of the $100,000 represents SS income in this example to arrive at the $11,100 taxable SS income.

Jeff Enders says

In my example ALL $100,000 was SS income! I stated that.

and to be clear, the $11,100 (line 6b of Form 1040) is part of Adjusted Gross Income (line 11 of Form 1040) but after subtracting the standard deduction ($34,700), Taxable Income is zero (line 14 of Form 1040).

worksheet 1 (page 7):

https://www.irs.gov/pub/irs-pdf/p915.pdf

I also verified at:

https://www.dinkytown.net/java/1040-tax-calculator.html

missing line items are zero.

line 1: $100,000

line 2: $50,000

Line 6: $50,000

Line 8: $50,000

Line 9: $32,000

Line 10: $18,000

Line 11: $12,000

Line 12: $6,000

Line 13: $12,000

Line 14: $6,000

Line 15: $6,000

Line 16: $5,100

Line 17: $11,100

Line 19: $11,100

JoeTaxpayer says

Jeff – even the White House website on the page proclaiming promises made promises kept also states the 12% of Social Security recipients will still owe tax on their Social Security. (and the $6000 additional deduction doesn’t wipe that out.) What was promised during the campaign was “no tax on Social Security“. There is no way to spin this that makes it the truth.

Harry Sit says

Joe – It’s more than 12%. The reason: https://thefinancebuff.com/social-security-taxed-2025-trump-tax-law.html/comment-page-1#comment-36955

Harry Sit says

Robert – I have a calculator for it: How Much of My Social Security Benefits Is Taxable?

Mike says

Jeff, maybe I’m missing something.If your SS is $100,000 the taxable portion at 85% is $85.000. Under the current law filing MFJ you would deduct $33,200 ($30,000 +1600*2) for a Taxable income of $40,413. You would be in the 12% bracket and your taxes would be $4,373.

How did your $11,100 get there?

Jeff Enders says

look at my post above; I provided a link to the IRS official worksheet and the entries that would go on that worksheet to get to $11,100.

Do not subtract $33,200 (now $34,700) from $85,000; that is not correct.

Review the worksheet I posted or Harry’s calculator

https://thefinancebuff.com/social-security-taxable-calculator.html

It is also important to note that the $11,100 is part of AGI. THEN subtract $34,700. Taxable income would be zero and no need to file a tax return.

Harry Sit says

The taxable portion isn’t 85% or $85,000. Use the calculator: https://thefinancebuff.com/social-security-taxable-calculator.html

Mike says

Jeff, Harry,

My mistake. Thanks for the answers.

Gary says

Reading this diatribe I marvel at your patience, Harry.

Thanks for what you do!

Liftlock says

An interesting exercise is to enter Social Security benefits without any other income into the income tax calculator found here:

https://www.dinkytown.net/java/1040-tax-calculator.html#

Some taxpayers may be surprised at how little of their Social Security is actually taxed.

Then start adding non -social security and observe how taxes change.

Having non- social security income substantially drives how much Social Security is taxed. Many taxpayers are not aware of this.

JoeTaxpayer says

I looked at the Dinkytown calculator. It doesn’t match Harry’s calculator nor the one I am trying to build. From what I can tell, even after checking the 65+ box, it’s not including the $6000 extra deduction. FWIW, I used a $36000 SS benefit and $30,000 IRA distribution to check results. Harry’s estimate $2480, Dinky – $3293, a difference of $813. 12% of $6000 is $720, so there’s more than the $6000, but I believe that’s a start.

Harry Sit says

The Dinkytown calculator doesn’t include the $750/1,500 increase in the standard deduction or the senior deduction. Mine does.

Liftlock says

It looks like the DinkyTown 1040 calculator has not been updated for the BBB.

Liftlock says

This evening I received an email from Barron’s that reads:

“the annual inflation bump to Social Security benefits has averaged 2.6% over the past 21 years, versus 5% for the average Medicare Part B premium. Next year, the standard Part B premium–which gets automatically deducted from the Social Security checks of retirees on Part B—is projected to rise 11.5%, to $206.20 a month. The cost-of-living adjustment, meanwhile, is forecast at 2.7% for 2026.”

If the above is true, would this make the per person 2026 Part B IRMAA surcharge for the 1.4X IRMAA bracket equal to 40% of $206.20 or $82.48 per month ($989.76 per year)? I seem to recall an earlier post on this board that IRMAA surcharges were capped at a 6% increase per year. Does any one know?

GeezerGeek says

Liftlock, the Part D base rate is capped at 6% per year, not Part B.

RobI says

The latest Medicare Trustees report also has projected Part B premium for 2026 of $206.50, which will finalize once Sept CPI gets published. Page 204 of the report has projections above inflation for years 2035-2034. Part D projected to be up 6%.

The Medicare Hold Harmless provision will cap increases for those on Social Security, but, by law, does hot help IRMAA payees. See this article https://www.investopedia.com/terms/m/medicare-hold-harmless-provision.asp

Rob I says

sorry years 2025-34 (not 35)!

Robert H says

Rob. Where do you see $206.50 as the projected Medicare Part B premium for 2026 in the investopedia site? I don’t see it, including any of the url links in the article. That would mean a 11.62% premium increase over 2025 (i.e., $206.50 vs $185) which wouldn’t surprise me when compared with the health insurance industry premium increases. Fortunately, the Medicare Hold Harmless provision would prevent such an increase, since there is no way that SS income would increase anywhere near that %.

Harry Sit says

If I understand it correctly, when Social Security goes up by 2.5%, only people getting less than $800 per month will be held harmless from a $20 increase in Medicare. That’s well below average.

Robert H says

Harry. I find it hard to believe that there are many (if any) SS recipients receiving under $800/month in benefits, especially 66+ seniors. In any case, I have never read anything about such a Medicare Hold Harmless restriction. Please see the following on this topic:

https://www.medicareinteractive.org/understanding-medicare/health-coverage-options/original-medicare-costs/increases-in-part-b-premiums-and-the-hold-harmless-provision

Can you please provide an official Medicare website indicating that the Hold Harmless provision does not apply to individuals with monthly SS income over $800.

Harry Sit says

The $800/month comes from dividing a $20/month increase in Medicare by a 2.5% increase in SS, or dividing $21.50/month by 2.7%. Basically the SS COLA in dollars must cover the Medicare increase in dollars.

Jeff Enders says

just to add on… the $800 of math is because effectively everyone (I know there are exceptions) pays the same Medicare premium, but everyone receives different SS benefits.

Anyone who receives $800 or less of SS with a 2.5% inflation adjustment, would receive no more than $20 per month in additional SS payments.

So everyone who receives under $800 per month (and not subject to IRMAA, etc) would be held harmless as their monthly SS premium would increase less than the $20 Medicare increase.

For example, someone who SS is $400 per month would see a $10 per month inflation adjustment (at 2.5%), so their Medicare premium could not be increased more than that same $10 per month, even though Medicare premiums for most increased $20 per month.

Mike says

Here’s what Social Security says about this (they haven’t updated this site as it still refers to 2022 premiums):

https://blog.ssa.gov/how-the-hold-harmless-provision-protects-your-benefits/

Medicare

How the Hold Harmless Provision Protects Your Benefits

November 30, 2020 • By Darlynda Bogle, Assistant Deputy Commissioner

Reading Time: 1 Minute

Last Updated: April 18, 2025

How-the-Hold-Harmless-Provision-Protects-Your-Benefits

Social Security works together with the Centers for Medicare & Medicaid Services to make sure you won’t have a reduction in your Social Security benefits as a result of Medicare Part B premium increases.

A special rule called the “hold harmless provision” protects your Social Security benefit payment from decreasing due to an increase in the Medicare Part B premium. The Part B base premium for 2022 is $170.10, which is $21.60 higher than the 2021 base premium.

Most people with Medicare will pay the new premium amount because the increase in their benefit amount will cover the increase. However, a small number of people will see little or no increase in their Part B premium — and their Social Security benefit checks will remain the same — because the amount of their cost-of-living adjustment isn’t large enough to cover the increase.

To qualify for the hold harmless provision, you must:

Receive Social Security benefits or be entitled to Social Security benefits for November and December of the current year.

Have your Medicare Part B premiums for December and January deducted from your monthly benefits.

There are exceptions:

The hold harmless provision does NOT apply to you if:

You enroll in Part B for the first time in 2022.

You pay an income-related monthly adjustment amount premium.

You are dually eligible for Medicaid and have your premium paid by a state Medicaid agency.

You can learn more about Part B costs by visiting Medicare.

It’s only an issue when the COLA is small enough that your increase in benefits doesn’t cover the premium increase. The kicker is that reference to IIRMA.

Robert H says

Mike. I read the same provisions in the two websites I mentioned in my earlier reply to Harry on this topic. I have not seen any reference anywhere to a $800/month SS income threshold previously mentioned with respect to the Medicare Hold Harmless provisions. On a basic level, I believe that the intention of the Hold Harmless provisions is to ensure that the year-to-year increase in Medicare Part B premium cannot exceed the SS COLA increase. For whatever may be specific exceptions, this may not be the outcome, but I believe that was the intention. I also did see that anyone who falls into the IRMAA trap is not covered by the Hold Harmless provisions.

Mike says

Don’t get focused on the $800 that was referenced in an earlier post. He just used that and an assumed 2.5% COLA to show why only people who received less than $801 would be protected. As another example, if the premium was to be raised by $40 and the COLA was 4% then only people getting less than $1000 would be protected as 4% of $1000 is $40 and their new $1040 benefit, after they paid the new $40 more in premium, would leave their benefit unchanged at $1000 (1000×4%-40=1000). but 999×4% =1038.96 and after paying the new $40 they would be losing $1.04 . Anyone getting more than $1000 would have their premium be offset.

The writer was simply showing and example of what the hold harmless provision was designed to protect. If the COLA was zero but the Part B premium had to be raised, EVERYBODY would have to be protected and there would be no legal way to raise anyone’s premium short of those on IIRMA or people just signing up.

RobI says

Robert H

Here is a link to the CMS Medicare trustees report. https://www.cms.gov/oact/tr/2025. You can read their actuarial premium ‘projections’ on pages 204-209.

Thestreet.com did a good write up here which triggered me to dive deeper.

https://www.thestreet.com/retirement/millions-of-medicare-beneficiaries-could-see-major-price-shock.

Article discusses to why Medicare costs are expected to keep on rising, including growth in number of Medicare recipients and Medicare Advantage reimbursement growing as % of total .

Like it or not, Premium costs are likely going up faster than CPI and will become a hot issue in financial planning (non political comment). Makes staying out of IRMAA even more critical going forward.

RobI says

Another article I meant to reference from The Street. This is the one discusses overall premium increase trends from the Trustees report and its root causes.

https://www.thestreet.com/retirement/retired-workers-to-see-shocking-change-to-medicare-in-2026

The Wizard says

I’m not sure why staying out of IRMAA territory is a superior strategy. The higher your AGI and the higher your IRMAA tier, then the smaller your Medicare premium is as a percentage of your gross income.

Now most people don’t have a lot of control when it comes to increasing their AGI in retirement, I understand that.

And I’m talking about an AGI steadily increasing each year with inflation, not a one time blip due to a big capital gain or whatever…

GeezerGeek says

Wizard,

I agree. I’m not trying to stay out of IRMAA brackets. My strategy is to be near the top of whatever bracket I’m in. Close to the top but not too close that a change in the inflation rate or unexpected income at the end of the year would push me into the next higher bracket. If I need to increase income to get higher in the bracket, I’ll do a Roth conversion. If I need to decrease income to get below a bracket, I’ll do a QCD from my IRA instead of taking the full RMD as income.

I’ve been using a conservative projected inflation rate of 2.5% and try to stay about $3,000 below the next bracket, which allows one bracket limit shift of $2,000 (MFJ) and an addition $1,000 for unexpected income. Better not to cut it too close because the penalty far outweighs the reward (Pascal’s wager). Harry wrote an excellent article on that principle that I follow religiously.

https://thefinancebuff.com/pascal-wager-uncertainty-tax-rules.html

tom says

Robi,

You are right about that. Unfortunately, my Social Security Income, Interest and Dividend Income, and RMD automatically push me into the world of IRMMA.

My strategy now is to try to estimate the dollar limit of my IRMAA bracket, and take a SEP-IRA distribution that is greater than RMD, but less that what would cause me to jump into the next IRMAA bracket. In the latter part of December each year, I have to hand-calculate the amount of interest and dividends I will earn from institutions for a 31-day month, and then add those amounts to the amounts that appear on the end of November statements. A miscalculation can be costly, as I’ve learned in the past. I generally refrain from taking any capital gains in December. This year, I will use the brackets values that I found on this site we are currently viewing, i.e., https://thefinancebuff.com/medicare-irmaa-income-brackets.html, and be careful not to cut it too close. My thanks to Financial Buff for preparing the 2025, 2026, 2027 IRMAA brackets information.

Jeff Enders says

Mike – great post

2010: SS increase was 0%; Medicare increase was $15 per month

2011: SS increase was 0%; Medicare increase was $4 per month

per a Google Search, 73% of Medicare beneficiaries were held harmless in 2010 and again in 2011!

David Swanson says

Harry,

I withdraw some cash from my Traditional IRA every month, some of which I do not spend. I have paid all the Federal income tax on it every month. This excess cash is in my savings account at my bank, commingled with other funds. Since I don’t need it now, I would like to deposit this excess cash back to my Roth IRA. No tax write-off or anything, I just want it to earn interest and withdraw it years from now tax-free, principle and interest. I would have to report it on my 1040 form. Am I allowed to do this?

DBS

Terry says

There is nothing to report on your Form 1040 for making a Roth IRA contribution. You are allowed to contribute to a Roth IRA up to the amount of your earned income subject to the income limtiations and the annual contribution limits. Withdrawals from a Traditional IRA have no impact whatsoever on your Roth IRA.

Harry Sit says

Two ways you’re allowed to do it. (1) If you have W-2 or self-employment income and you’re within the income limit. (2) For the amount you withdrew in the last 60 days and you haven’t used up your one indirect rollover per year allowance.

Mike says

Dave, basically you are withdrawing too much money from your TIRA. I only take out cash from my TIRA for my RMD. I then live on that. Fidelity transfers any withdrawals within 24 hours so using Quicken I know exactly how much cash I need every day/week to cover payments coming up and if I need more cash I just transfer it from my TIRA. My checking account is a way-station for bill payment. If I am traveling I’ll simply transfer enough cash to cover bills due through the end of the month. All my bills are on Autopay. My checking account rarely has more than $1,000 in it except days when Social Security or Pensions get deposited. But I never take out more than I need, though my RMD is definitely more than I need, but I can’t not take it out eventually.

Terry says

Harry — Are you saying that David can take the money that he has withdrawn from his Traditional IRA and put it in his Roth IRA, thus retroactively treating it as a Roth conversion as long as it is done within 60 days of the withdrawal? If the withdrawal was an RMD, this would not be allowed — correct?

Harry Sit says

David didn’t say whether he’s required to take the RMD (age 73+ by 12/31) or whether the RMD was already satisfied. If he’s subject to the RMD, as Jeff pointed out, he can only rollover the amount withdrawn within the last 60 days AND after the RMD was already satisfied.

Jeff Enders says

Terry – you have to take this in separate steps.

1) you can always reverse a distribution from an IRA as long as you do it within 60 days from the original distribution date and you can only do it once per year. It has nothing to do with whether the dollars are part of an RMD or not. However, if it is part of the RMD you still have to satisfy the RMD requirement by the end of the tax year.

2) Once the money is back in the Trad IRA, you can do a conversion to a Roth IRA. However, conversions are not permitted until any RMD is satisfied.

3) there is nothing that precludes taking RMD dollars that were already distributed from the TRAD IRA and putting it back in the TRAD IRA, but if you are subject to RMDs, what is the purpose since you’d still have to satisfy the RMD by year end and can’t do a conversion until that RMD requirement is satisfied.

See the IRS link below.

https://www.irs.gov/retirement-plans/plan-participant-employee/rollovers-of-retirement-plan-and-ira-distributions

Harry Sit says

Let’s pause going down the rabbit hole of RMD until David comes back to say whether he’s subject to the RMD. It only confuses him if he’s not.

Robert H says

David. Terry is correct regarding a direct Roth IRA contribution (other than a Roth IRA conversion from a traditional IRA) in terms of not having to report it on your 1040 tax return. I’m sure you know that a withdrawal from the traditional IRA is taxable and needs to be reported as such on your 1040 return. Any transfer of money out of the traditional IRA is part of your MAGI and therefore counts towards the IRMAA MAGI threshold. Also note next time that you can instead do a Roth IRA conversion (i.e., direct transfer of money from the traditional IRA to the Roth IRA) if you don’t need the cash at this time. The conversion is taxable on your 1040 return.

Jeff Enders says

David – the way to do this is a CONVERSION. There is no dollar limit on the conversion, other than you must satisfy the RMD prior to doing any conversions.

As Harry stated, you can make CONTRIBUTIONS to a Roth IRA (or a Trad) up to $7000 per year ($8,000 if over 50 years old) or your earned income, WHICHEVER IS LESS. If you are retired, this doesn’t work. You can also reverse any Trad IRA distributions you made in the last 60 days and then complete a CONVERSION, but again you can’t do conversions unless the RMD is first satisfied

David Swanson says

No, I am not subject to RMDs from my Traditional IRA for another 2 years. I only wanted to know if I can make a contribution to my ROTH IRA with funds that are not from wages, salary or tips, i.e. W-2 income. The money is from a Traditional IRA distribution that I paid the required Federal income tax on and that sits in my savings account at my local bank.

The money in my Traditional IRA came from wages at my last job, so technically it is originally from W-2 income. One might argue that any earnings from my contributions would not be earned income.

I don’t want to violate the law, but it seems to me that I could deposit this money in my ROTH IRA. It would not be a conversion but a contribution and subject to maximum limits. I read on the internet that IRA contributions must be from taxable compensation only, which can include money from “Taxable retirement account withdrawals”.

Jeff Enders says

David – if you take a distribution from a TRAD IRA, that distribution is irrevocable once 60 days pass. Within that 60 days you can recharacterize the distribution as a conversion and put it into your Roth IRA. You can only do this ONCE per year. There is no dollar limit.

Otherwise, any contribution to your Roth IRA is predicated upon your earned income. The limit is the lesser of your earned income or $8,000 (assuming you are over 50) and there are phase out provisions that begin to kick in at $150,000 (file single) and $236,000 (file joint) of earned income.

Understanding how the IRS uses the words “contribution” and “conversion” are quite critical to understanding the rules. they connate very different steps and rule requirements.

The much easier way is to have a plan to do ‘conversions’ from your Trad IRA directly to the Roth. There is no dollar limit on a conversion and there is no limit to how many times per year you do a conversion. You can either net the tax out of the conversion or make the full conversion and pay the tax from other after-tax funds you have. The IRS does not care. Investmentwise, it’s best to pay the tax from after-tax funds so you get the full value of the conversion.

Can you make CONTRIBUTIONS to your Roth that are not from earned income? NO

Can you do CONVERSIONS to your Roth that are not from earned income? YES – these are dollars that come directly from your TRAD IRA and no other source.

does that help? any questions?

Harry Sit says

David – Taxable compensation (or “earned income”) means income from a job or self-employment. It doesn’t include money from taxable retirement account withdrawals.

Jeff – I fixed those two typos in critical spots for you.

The Wizard says

Also, when doing a Roth contribution, you must have Earned Income in the current calendar year. Earned Income from a previous year is not applicable…

Jeff Enders says

The Wizard – EXCELLENT point!

Also, in my earlier post, a typo as I meant to state: the IRS does NOT care.

Jeff Enders says

Must be too early in the morning to be posting: another typo.

Understanding how the IRS uses the words “CONTRIBUTION” and “CONVERSION” are quite critical to understanding the rules. they connate very different steps and rule requirements.

JoeTaxpayer says

Mike – I see you said you only take the RMD. Just a thought, given the venue. If you have the room, some amount available to fill the current tax bracket, and not risk an IRMAA bump, this is when a conversion to Roth is most beneficial. It gives you flexibility for years you might need the extra funds, and helps keep the RMDs from forcing you into the next bracket.

Mike says

Joe, appreciate the advice. I am in the unfortunate position of having grown my TIRA’s (wife’s and mine) to what has become in some ways an albatrossian burden. Pardon my attempt at humor. In 2026, my first year to be paying IIRMA, I will be in the 2x hell. And in 2027, barring a market crash it will be 2.6x. My headroom this year is about $43k to convert and avoid the next level. If I do that though I will have to pay $10,300 in taxes (24% bracket). I estimate I will remain in the 2x bracket for the next three years and then move into the 2.6 area. So I would incur $10,300 in taxes to avoid about $7,000 in annual IIRMA next year and more in subsequent years. I expect to be in the 32% bracket by 2029 with just average S&P growth.

Jeff Enders says

Mike – totally understand your predicament…. we were all encouraged when we were younger to defer, defer, defer. We weren’t focused on the “time bomb” that awaited in our 70s. Welcome to the “time bomb”.

What is your ‘end game’? Who gets the money in the end? If your children are successful professionals, they might be paying an even higher tax rate and only have 10 years to liquidate the assets. It might cause you to consider whether to ‘bite the bullet’ and focus on the highest tax bracket you are willing to stomach and let the IRMAA chips fall where they may. Any financially successful children will thank you later as they get to keep more.

On the other hand, if it is all going to be left to charity, not confident that doing conversions makes any sense! The goal would be to pay as little tax as possible, and just do the RMD and that is all, and leave as much as possible for the charity!

IRMAA is the tail to this dog and I think many get fixated on IRMAA without taking the long view.

Depending on your “end game”, the way to slow down the growth of the TRAD IRA is prioritize the equities for distribution / conversion. Focus the conversions and RMDs on the equities that are expected to perform the best. Why? Because once the equities are in the Roth or in your after tax brokerage account, the growth is unlikely to be further taxed (Roth will remain in a tax free status until 10 years after passing and after-tax brokerage will eventually “step up” upon passing).

make sense? it is a VERY complex topic.

Mike says

Jeff,

No children. It all goes to charities once we both are gone. There’s 10 years age difference and assuming I’m first my wife will be the beneficiary and is aware of current law on transferring of the Roth and TIRA. And yes, complicated as only government and lawyers can make it.

Jeff Enders says

Mike – then if it all goes to charity in the end, why do conversions? You end up giving money to the government (tax) that would otherwise go to charity.

are you familiar with QCDs? that is available once you are 70.5 years old. You can even avoid tax on the first $108k (2025) of distributions from a T-IRA each year by gifting DIRECTLY to a charity. That would reduce your RMD (beginning in two years) and then help with the IRMAA issue.

have you discussed with a financial planner? sounds like a few bucks for that advise could save you A LOT of money.

Mike says

Jeff,

You asked ‘why do conversions?’. Some years ago I came to the same conclusion. I had done three conversions and noticed that my TIRA ended each year bigger than the prior year while I was trying to get it to zero, and it hit me that I wasn’t making progress and giving the IRS unnecessary tax money. So I stopped doing conversions.

On QCD’s I am aware of them. I don’t make very large donations and doing a QCD was essentially giving away more money than I would save. And while charity is a noble thing I am more concerned with not running out of money, even if I could never run out. Shit happens and I want to be guaranteed that when we no longer can live in our own house that I will have whatever money is needed to remove that worry. In the meantime the charities will not do any worse because I didn’t give them my money quicker. Even Bill Gates and Warren Buffet haven’t decided to give away even more of their money now instead of at death.

And we are still very healthy so that we travel a lot and that gets expensive. When it comes to financial matters I am sort of like the guy who wears a belt and suspenders with pants that have elastic waists.

On your question of using a financial planner, I don’t use one though I had talked with a few years ago and decided I’d rather do it myself. That’s worked out well and I read a lot. But we’re probably going to be forced by prudence to do so because as we get closer to my wife surviving me I want to make sure she has whatever advice she might need.

RobI says

Jeff.

Totally get your point on the deferred tax ‘ time bomb’. I’m living it. While the large tax deferred savings pot is a blessing, it’s now boxing me out of so many better choices now I’m approaching my 70s. I may have been better advised spending or gifting more when younger.

David Swanson says

Not to drag this out, Thank you all for your most useful comments. I will not be contributing to my ROTH IRA from anything but earned income from a job.

But in looking for an answer to this question, I first looked on the internet. I googled the words “taxable compensation” and first on the list, under “AI Overview” is a bulleted list and at the fourth bullet I read “Other Forms of Compensation: This can include:

Taxable retirement account withdrawals.” Google it yourself. Maybe they mean a conversion.

And I also had a live chat with someone at the Turbo Tax website, who also said the same.

The moral of the story is: don’t take anything someone says on the internet for the truth. Always ask lots of questions from everyone.

Thanks again for your help!

Harry Sit says

Only googling “taxable compensation” lacks context. Googling “taxable compensation for Roth IRA contribution” will give you a better answer, even from AI.

We should learn to find primary sources of information and which secondary sources are reliable. AI and chatting with someone at TurboTax are both secondary sources, which proved not so reliable. The IRS website is a primary source. Its Publication 590-A talks about IRA contributions and defines what is compensation on page 6.

https://www.irs.gov/pub/irs-pdf/p590a.pdf

Now you know this website is a more reliable secondary source.

Robert H says

David. Any statement that Traditional IRA withdrawals represent “taxable compensation” is totally incorrect. Withdrawals from a Traditional IRA are taxable (assuming a tax deduction was previously taken for the contributions to the IRA) whether you put the withdrawn money into a non-IRA account or convert that money to your Roth IRA. Taxable compensation is from wages (W-2) or self-employment income. Self-employment income is either from a trade or business as a sole proprietor (including a part-time business or as a gig worker) or an independent contractor (1099-NEC). It also includes your share of income from a partnership or Subchapter S corp that carries on a trade or business.

The Wizard says

I tend to frown at terms like “tax torpedo” or “time bomb” when discussing tax-deferred accounts. We put $$$ into those accounts back when working for one reason: so that we could have a hefty stream of Ordinary Income in the follow-on years when no longer working.

I feel it’s important to start withdrawing from tax-deferred in your very first year of retirement, which was age 63 for me. You don’t have to SPEND all that income immediately; you can invest some of it in your taxable account or (preferably) your Roth IRA.

Once you are of RMD age, your investment options for withdrawals are more restricted, yes. But here’s the good news: once you have a growing amount of money in your taxable and Roth accounts, you are building real wealth. Money in tax-deferred, by comparison, is a very light green shade of wealth…

Mike says

David,

So I Googled “Taxable Compensation” and I pasted the response below. The fact is you cannot trust AI. It depends what you ask and how you phrase it. It also depends on whose AI your browser is using. Obviously my AI response said nothing about taxable account withdrawals, nor the RMD consideration. Like most complcated topics, or anything the government or IRS says, you really do need a lawyer or CPA or IRS person to explain it correctly.

Here’s the response I got from AI:

Taxable compensation includes wages, salaries, bonuses, tips, and other forms of payment received for services rendered. It is subject to federal and state income taxes, as well as Social Security and Medicare taxes. accountinginsights.org irs.gov

Definition of Taxable Compensation

Taxable compensation refers to any payment received for services rendered that is subject to income tax. This includes various forms of income that individuals earn through employment or self-employment.

Types of Taxable Compensation

Common Forms of Taxable Compensation