The Fed’s keeping interest rate low with QE3 will change a lot of things. I thought of one more habit change after I finished the previous post 3 Good Money Habits Going Obsolete In a Low Interest Rate World.

Old Habit: Earn Interest From Money On Deposit

New Habit: Get Paid For the Banking Relationship

In the old days, you put money into an account. You earn interest on the money. Simple.

These days, you don’t earn much interest on the money on deposit. It’s quite laughable when a rate under 1% is considered “high yield.” Instead, banks pay you for having an account with them. It’s only loosely tied to the amount of money you have with them. They are paying for the relationship.

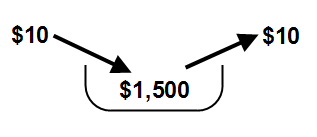

For example, Citibank was giving reward points worth $100 in Amazon gift card for opening a basic checking account with them. [Update: the offer for bonus reward points has since expired.] The basic checking account is free of monthly fee if you keep $1,500 in it or if you do 1 direct deposit and 1 bill payment every month. To earn the $100 in Amazon gift card, you need to

- enroll in their ThankYou points rewards program;

- have 1 direct deposit into the account and 1 bill payment from the account for 2 months

The direct deposit can be satisfied by a scheduled monthly recurring ACH transfer from your current bank account into the new Citibank account. The bill payment can be satisfied by a scheduled monthly recurring $10 payment to a credit card. Both require only a one-time setup.

You don’t have to switch over your primary checking; you can just use it like a savings account.

Your $1,500 if left in a “high yield” savings account that pays 1% will only earn $15 in a year. Even without a signup bonus, if you keep the monthly scheduled deposit and the scheduled bill payment, the Citibank checking account will give you ThankYou points worth $4 per month. On an ongoing basis, you will earn $50 a year from having a basic checking account with Citibank versus just $15 interest from your money in a “high yield” savings account.

Which is a better deal: $50 a year versus $15 a year elsewhere? After a one-time setup, everything is automated. You just sit back and collect the rewards. Although it may pain you to see your money not earning interest in a basic checking account, earning interest is not the game anymore. Reward points are worth several times more.

Who says big banks are bad? You just have to know how to use the account.

Although $50 a year doesn’t seem like much, in a low interest rate world, every bit counts.

Chase also offered a $200 bonus for opening a checking account (online link took down by Chase; ask in a branch if you still want it). Like Citibank, a $1,500 balance will keep it free of monthly fees. Unlike Citibank, Chase doesn’t pay on an ongoing basis after the initial bonus. You just keep $1,500 there for six months and treat it like a 25% APY 6-month CD. Nothing stops you from having an account with both Citibank and Chase. I signed up for both.

If it were up to me, I would much prefer to earn interest the old fashioned way. But the Fed isn’t giving me that choice. It wants me to play games. Although I got the message a little late, I finally figured it out. Fine. I will play along.

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

jc says

If I’m reading right, $1500 isn’t required to do this. There is no minimum to open the basic account and if you do the direct deposit and the bill pay, there is no monthly fee regardless of balance. So, you could do this for $0 plus the transfer in/out each month. I don’t think I’d take it quite to that extreme, but leaving $100 in this account to make $50/year and the other $1400 earning 1% elsewhere sounds reasonable.

Harry says

jc – You are correct. Technically the $1,500 isn’t required. However, the $1,500 will guarantee you won’t pay a monthly maintenance fee. My first priority would be do no harm — even if for whatever reason I’m not getting the reward points, I don’t want to end up paying a monthly fee. After it’s all up and running, you can withdraw it down to $100. The $1,500 serves as a cheap insurance policy before you get the reward points.

Harry @ PF Pro says

Checking and savings account bonuses are usually taxed, so hack off 30-45% right there 🙂

Credit card bonuses on the other hand are not, that’s why they are so much more valuable and they offer a lot more.

David C says

Just a word of warning regarding Chase, I’m reading conflicting information that suggests that they are no longer accepting some bank ACH pushes as direct deposits… at least for the 1st direct deposit necessary for the $200 bonus. It sounds like Ally still works, but ING Direct and Alliant doesn’t anymore… if you trust random strangers on the Internet 🙂 http://www.fatwallet.com/forums/finance/432086/

@ Harry@PF Pro

Slight correction, credit card opening bonuses that you receive just for opening the account (and doing nothing else) ARE taxable. Credit card opening bonuses that require a certain amount of spending are not taxable as the IRS lumps them along with credit card rewards earned while spending: they are considered to be discounts on purchases and thus not income.

Harry says

David C – Thanks. I’m watching that thread with amusement, as people try to figure out what works and what doesn’t with no rhyme or reason. My current theory is that if the originator uses prenote, it will work because most payroll direct deposits use prenote as opposed to random deposits. Fidelity uses prenote.

Harry @ PF Pro says

@David C – Ah ok that makes sense now, thanks for that tip! I see now why they have the spending req’s or they give you the bonus after the first purchase.

Harry says

I added a savings account at Citibank and I scheduled a recurring monthly transfer of $10 from checking to savings. This will give me additional 175 reward points per month bringing the ongoing value for the checking/savings combo to $72 a year. Not counting the initial bonus, it’s a 4.8% yield ongoing if I keep the $1,500 in the accounts, more if I only leave $100 in each.

Jules says

Harry, thanks for mentioning this. I was considering signing up for this account based on your recommendation. But then I thought about my experience redeeming ThankYou points. You probably know Citi has different terms for how you can redeem ThankYou points, depending on which accounts you have with them. For example, I just logged into my account at Citi, hit the ThankYou Rewards button, searched for Amazon, and found the only possible denominations to redeem are: 3500 points = $25 Amazon gift card and 6000 points = $50 gift card. The $100 Amazon gift card was not available. Perhaps if I added a bank account, the $100 = 10000 points option would suddenly appear. It’s not clear.

But I’m not going to find out. Am sadly about to cancel both of my Citi credit cards and terminate my relationship with them, as I just found that I can no longer ethically do business with them. I just learned that Citi is a supporter of Shariah-compliant banking, which requires Citi to donate 2% of profits to dubious “charities”. If you’ve ever seen movies like The Stoning of Soraya M., or read books like Not Without My Daughter, you know how horribly women are treated under Shariah law. I cannot and will not support this.

Keep up the great work discovering, thinking, and writing about finance. I will continue reading as usual.

Harry says

Jules – I will post the options available to me when I receive the reward points. I understand your philosophical objection to certain business practices. There’s a big market for Islamic finance. I don’t blame them for wanting to be in that market. A former colleague of mine is a Muslim. He couldn’t borrow money for a home. He had to use a compliant institution.

Jake says

Hey here’s a blog post idea. Compile a list of accounts offering cash/points for opening a new account. I’ve come across various ones online but would like a list of ones to get.

I think this is a good “investment” idea. Open accounts with no account fees that pay you for the banking relationship and then once the money is made either use them or close them.

Leigh says

Is Chase still offering a $200 bonus? The coupon I just got in the mail is “only” for $125.

Harry says

Leigh – The $200 one expired. Here’s one for $150 expiring 12/15/2012.

Leigh says

Harry, thanks! Do you know if they do a hard pull or a soft one on your credit to open the account?

Harry says

I have no idea. Never cared, because a high credit score is not necessary for the best loan rate.

indexfundfan says

Looks like the party will end in Dec 2014.

http://www.fatwallet.com/forums/finance/1380674/

Harry Sit says

Thank you for the heads up. I will close my accounts after I get the points in December. Those who have a mortgage with Citibank still get The Citibank package for free, although they too will be earning fewer ThankYou points.

Elizabeth says

Harry, what do you think of ELFCU hi interest checking 4% for the first $1000. what is to stop you from having joint accts or single accounts if you are married. I can easily think of 10 accounts to open.

Harry Sit says

Just first $1,000 is way too low. It requires 15 transactions per statement cycle. You will need 150 transactions per statement cycle if you open 10 accounts.