401k plans are slowly getting better. My plan added a low-cost collective trust. My wife’s plan added a self-directed brokerage account, also known as a brokerage window. Her plan is managed by Fidelity. Fidelity calls it BrokerageLink.

Some 401k plans managed by Charles Schwab also have this feature. Schwab calls it PCRA — Personal Choice Retirement Account.

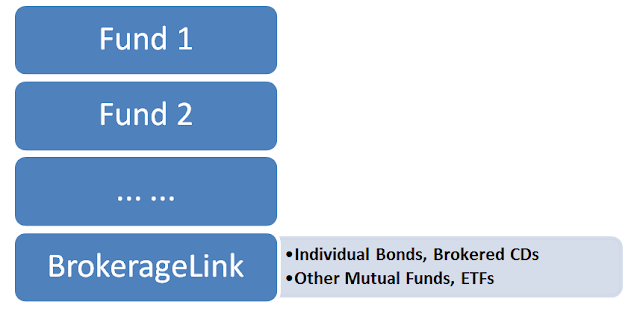

How Does It Work?

Fidelity BrokerageLink is listed in the plan’s investment options just like another fund. She can designate a percentage of her ongoing payroll deductions toward it. She can transfer money between it and other funds. She can rebalance her plan account by saying what percentage of the total plan account should be in BrokerageLink.

Inside BrokerageLink, it’s just like a regular brokerage account, with its own account number. You can buy or sell pretty much everything you can with a regular brokerage account.

The “link” that connects BrokerageLink to other funds in the plan is a money market fund. Money going into or coming out of the brokerage account is put into or taken from the money market fund. From there, you place trades to buy or sell other mutual funds, ETFs, individual stocks and bonds, etc. This is similar to how Vanguard Brokerage Service works.

Because it’s a two-step process, it’s too much trouble to put a percentage of the ongoing payroll deductions into BrokerageLink and place trades twice a month. Instead, it’s easier to still put the ongoing payroll deductions into core funds. Transfer a chunk to BrokerageLink after the money builds up to a larger sum.

Fees

Other 401k providers often charge a high annual maintenance fee and high trading commissions for the self-directed brokerage account. A fee of $100 to $200 per year is quite common. Fidelity doesn’t do that. Its BrokerageLink has the same low prices as its retail brokerage accounts. There is no annual fee. Commissions are the same as retail:

- Fidelity funds: free

- Treasury bonds: free

- new-issue brokered CDs: free

- select iShares ETFs: free

- Vanguard ETFs: $5 a trade

The brokerage window opens up a world of good investment options. Prior to adding Fidelity BrokerageLink, my wife’s plan only offers two index funds: an S&P 500 fund and a US bond index fund. With Fidelity BrokerageLink, she will have many good options. I’m showing some of the best options here.

Fidelity Index Funds

Fidelity’s index funds are its answer to low-cost index funds from Vanguard. There aren’t as many as at Vanguard, but if you are limited to Fidelity, there are enough good choices. Notable ones include:

- Fidelity Total Market Index Fund (FSTVX)

- Fidelity Total International Index Fund (FTIPX)

- Fidelity U.S. Bond Index Fund (FSITX)

iShares ETFs

Fidelity has a joint marketing deal with iShares to make 240 iShares ETFs commission-free at Fidelity. Some iShares ETFs have lower expense ratios than comparable Vanguard ETFs. Some notable ones include:

- iShares Core S&P Total U.S. Stock Market ETF (ITOT)

- iShares Core MSCI Total International Stock ETF (IXUS)

- iShares Core U.S. Aggregate Bond ETF (AGG)

Vanguard ETFs

Vanguard ETFs will cost a $5 commission per trade in BrokerageLink. It’s best if you transfer a chunk to the brokerage window, buy in one trade, and then hold them and select free dividend reinvestment. If you buy a large chunk, paying a one-time commission is better than paying a higher expense ratio every year to a similar iShares ETF. Some notable ones include:

- Vanguard Value ETF (VTV)

- Vanguard FTSE All-World ex-US Small-Cap ETF (VSS)

- Vanguard MSCI Emerging Markets ETF (VWO)

With all these great investment options, Fidelity BrokerageLink makes a big difference to an average 401k plan.

Say No To Management Fees

If you are paying an advisor a percentage of your assets, you are paying 5-10x too much. Learn how to find an independent advisor, pay for advice, and only the advice.

Dan says

My employer added Brokeragelink a few months ago. I have used it mainly for buying iShares TIP. It is a nice feature overall, but has a few annoying delays and quirks:

1) New money arrives in BL a day after money contributed to the regular 401k core funds.

2) Transferring cash from BL back to the core funds requires a phone call (can’t be done online) and a day to transfer to the core money market fund, then another day to invest in the desired core fund. A core mutual fund exchange is an atomic transaction that happens all at once at the end of the business day.

3) There is no way to set up a standing order for ETFs, so I have to go in and trade manually every couple of weeks.

4) Fidelity’s own FullView (Yodlee-powered) doesn’t know how to count BL investments properly. It usually, but not always, double-counts them in my total investments and net worth.

All of these are fairly minor, especially when used for bond investments that don’t fluctuate much and in such a low-rate environment.

My broader concern is that Brokeragelink may give employers an excuse for not offering better low-cost core funds in their 401k’s. For example, my employer used to offer the VIPIX TIPS institutional fund (0.07% ER) in our 401k, but dropped it at the same time they added BL. Now they just tell us to use iShares TIP. Sure, an 0.20% ER is better than what most people have, but as long as we’ve got this paternalistic system of our employers pushing us towards specific investments… those employers ought to be using their influence and buying power to get the lowest-cost institutional funds for their employees.

I realize I might be accused of “making the perfect the enemy of the good here.” Overall, I think BL is a very positive development.

Johnny Begourdous says

Nice Dan, you have done terrible in the TIPs fund. I hope youre very conservative because you have missed out on massive gains you would have had elsewhere.

Johnny D. Begourdas = Loser says

Johnny Begourdous,

You are a disgrace to the human race. Go spread your negativity elsewhere.

Harry Sit says

Dan – Thank you for sharing your experience with Fidelity BrokerageLink. As mentioned in the post, I think it works best when you transfer a chunk from the core funds to BrokerageLink as opposed to trying to invest new money into it. I didn’t know about your note #2: must call to transfer back.

I agree with your comments about employers (or rather the plan vendors) using brokerage window to silence the demand for better funds. They must know that very few employees will take the trouble to actually use the brokerage window. As a result, they get to keep the vast majority of the money in the more profitable core funds. But for those who do take the trouble, it’s a great feature.

Dan says

TFB, you’re probably right. I like to get my money fully invested where I want it as soon as I have it, but my habit may be just a neurotic hassle in this case.

The first time I transferred money from BL to the core fund, I asked the Fidelity rep if I could do it online. He told me, “Boy, I wish you could. Everybody’s asking me.” Perhaps it’s something that will be fixed soon.

I guess that inattentive or uneducated investors will always be susceptible to paying too much. I just don’t want employers to use the accessibility of better options as an excuse to complacently default uninformed employees into crummy options.

Lynn says

I use the Schwab PCRA brokerage window. It’s an improvement over our 401K fund options, but I was disappointed to discover that most of the mutual funds available on a no-load, no transaction fee basis from Schwab are the more expensive actively managed funds. To buy an inexpensive index fund like Vanguard, I’d have to pay a $39 transaction fee.

Also, we’re only allowed to buy mutual funds, not ETFs, making it even harder to find inexpensive funds.

On the plus side, we can set up automatic monthly transfers to buy Schwab mutual funds.

edward says

Dan’s first comment describes my own experience, after over a year with the FBL option,

although I can’t attest to the standing order part. It’s true it requires a call to a rep to move

funds back, although they have claimed for some time it should be the same as the transfer

in, some day.

One additional point, although this may be specific to my plan: ask about funds lockup.

In my plan, certain transfers between “competing funds” can be prohibited for up to 90

days. As transfers into BL are to the core account (FDRXX), the direct competitor on the

other side is, of all things, the stable value fund. The one that most would think of as

the “core” or “cash” account on the employer side, as there is no other MM like choice.

I think there might be other pairings as well, and you can’t “launder” by passing quickly

through a non-competing fund. So far, we still have bond index and TIPS index with low

cost, but they don’t provide a ticker or much more than daily, YTD, 1yr, etc., price history.

From conversations with co-workers, I don’t think BL is widely used where I am.

Dan says

Good point, Edward. We have the “funds lockup” too. After numerous complaints, our 401k plan added a *separate* money market fund to the core, which is not subject to the lockup, so that money can be transferred between the core and BL without running afoul of it.

I don’t understand the rationale for the lockup at all. Just a seemingly meaningless bureaucratic hassle that’s easy to get snagged by. Is there some regulatory requirement for it?

Harry Sit says

The lockup is an artifact of the stable value fund. A stable value fund gives you an above-money-market interest rate while maintaining a stable value. In exchange, the investors must agree to keep the money there for some time. That’s the deal. Otherwise a stable value fund won’t work. It would have to either give you low yield like a money market fund or let the value fluctuate and potentially cause losses like a bond fund.

If a plan doesn’t have a stable value fund or if it doesn’t use the stable value fund as the conduit, you won’t have the lockup problem.

JeffB says

My concern would be for employees who might now “day trade” in their retirement accounts. Chasing one hunch after another.

David C says

Are there any restrictions on how much money can be placed in the brokerage window? The only reason I ask is that my 401k (through ING formerly CitiStreet) places limits on the amount of money I can place in the “self-managed account”: up to 75% of Traditional 401k contributions can be moved into the brokerage window, but NO Roth 401k money can be moved.

For that and other reasons I don’t currently use my plan’s brokerage window… but I’m just wondering if the contribution limit is ING-specific or not. Perhaps Fidelity and Schwab are more lenient in this department.

Harry Sit says

It’s plan-specific. In the plan I referred to in the post, she can transfer 100% of the balance into the brokerage window. She can also buy ETFs in addition to mutual funds.

nickel says

I have access to BrokerageLink, but cannot trade ETFs. Thus, I have to pay the $75 fee to get into Vanguard funds — though I can then set up an auto-invest for $5 once I have a position, fire it once to move a chunk of money, and then cancel. Kind of a pain, but it works.

Dan says

My BL plan *can* buy ETFs and *can* put 100% in BL, but… we could not buy treasury bonds as “individual securities” are deemed to be too risky. I can buy a 2x leveraged ultrashort ETF, but I can’t buy a single treasury bond issue? Go figure… :-p

Nickel, your plan probably forbids ETFs (and individual stocks, I presume) based on similarly poor logic about risk and volatility.

Actually, my colleagues made a sufficient fuss about the no-treasury-bonds rule that management is supposed to be fixing it. We’ll get the ability to buy individual treasury bonds in BL (with no commission if bought at auction, I might add). If you make enough noise, you might get the no-ETFs rule fixed as well. Point out that iShares ETFs are low-cost and diversified index funds with no commissions?

edward says

For my plan, USTs via BL are no problem. In fact, other than FINPX, that’s all I’ve used it for, TIPS at auction. I don’t think USTs ever have a commission at Fido, auction or secondary, buy or sell, but you have to pay their spread on buy secondary/sell. Might apply to other govvies as well, but I’m not sure. No restrictions on percentage of balance in, or percentage of contribution going to BL ( I have done 100%) for me, as far as I know.

I think my 401k has changed recently; “STABLE VALUE” is no longer there, but now we have a “SHORT DURATION FUND” and another called “FID INST MMKT”. Might be because of the lockup issue, but I’m not going into either, so I don’t care.

steve says

Had a question for the group, does anyone work at Nstar/Northeast Utilities? I know they offer brokerage link,

and am trying to find out if every fund/etf/stock is available. I have heard some plans only allow mutual funds.

Thanks for the help.

– Steve

paul says

Fees: $6.25/quarter = $25/year.

Adam says

Do you know if there are any tax implications within the brokerage link account if you buy shares of stock and later sell the shares for a profit?

Harry Sit says

There are none, because it’s still within the 401k/403b plan.

Sun says

I have account in vanguard and fidelity.

I’m 65.

All in mutural fund target plan.

I ll retire soon.

Fidelity fee much more than vanguard.

Is it worth move some to vanguard for cheaper fee or keep them in fidelity invest etf with brokage account or keep it there?

Harry Sit says

If you’d like to consolidate, you can certainly move from Fidelity to Vanguard or from Vanguard to Fidelity. If you decide to stay with Fidelity or move your Vanguard account to Fidelity, check out Fidelity Freedom Index Funds: Hidden Gems For Your IRA, Solo 401k, or Brokerage Window. The fees on those Fidelity Freedom _Index_ Funds are comparable to the fees on Vanguard target date funds.

Celia Williams says

So strange that after converting BL shares to cash, it is not really available for deposit into my bank account but has to be transferred back to the core Retirement account. Very, very inconvenient. I had a struggle to understand this arcane step, having lived with preconceived notions about accessibility of my own money, leading to the rep treated me like a simpleton. Dreading having to call back to get the cash sent to my bank account.