At the end of 2014, I amended and restated my solo 401k plan from a prototype plan sponsored by Fidelity to a prototype plan sponsored by Ascensus. I did that in order to enable non-Roth after-tax contributions for so-called mega backdoor Roth. See previous article Mega Backdoor Roth In Solo 401k: Control Your Own Destiny.

It’s been one full year. I went through the complete cycle from making the non-Roth after-tax contribution, distributing such contribution and earnings to a Roth IRA, to finally issuing a 1099-R as the plan trustee. This article documents the whole process. It will remind me what to do in the years to come. It also shows how it’s done in case others are interested.

I play four different roles in my solo 401k:

- as an employee participating in the plan;

- as the employer sponsoring the plan;

- as the plan administrator administering the plan;

- as the plan trustee investing plan assets.

I sign different documents, sometimes the same document twice, depending on which role I’m playing.

Elect Contribution

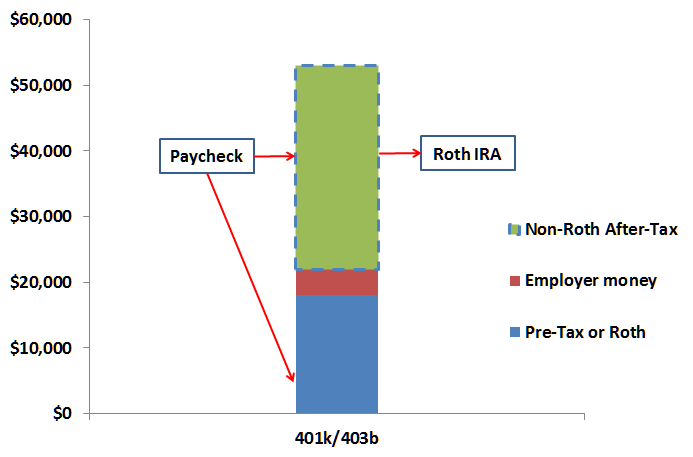

In a workplace 401k plan, you go to a website or you fill out a form to indicate how much you want to contribute to your 401k plan. For my solo 401k, I created a paper form as the plan administrator. I then filled it out as the employee and gave it to myself as the plan administrator.

Because I’m contributing my $18k to the plan at my day job, I chose to contribute 100% of my self-employment income as a non-Roth after-tax contribution to my solo 401k. The election I made will stand for future years until I change it.

Send Contribution

My plan assets stayed at Fidelity. I opened new investment-only retirement accounts at Fidelity, one per participant per contribution type. I transferred existing assets to the new accounts.

I had to get a separate EIN for my plan. I already have an EIN for my business, but my business doesn’t own these accounts. When I had the plan under Fidelity’s prototype plan, Fidelity Management Trust Company (FMTC) was the trustee. The accounts were held in trust by FMTC. Now that I’m on my own, I needed an EIN for the plan itself.

Getting an EIN was quite easy, and it was free. I did it online with the IRS.

After I closed my books for the year, I used my spreadsheet Solo 401k Maximum Contributions to calculate how much I was allowed to contribute to my solo 401k. I created another form as the plan administrator to document the contributions by contribution type (employee after-tax versus employer profit sharing).

I sent a check to Fidelity together with its Investment-Only Retirement Account Contribution Form, which broke down the contribution to each account.

Invest

After the contributions were credited to each account, I logged in to Fidelity as the plan participant and I invested the contributions. This was no different than buying mutual funds or ETFs in a brokerage account.

Request Distribution

As part of the document package, Ascensus included a distribution request form and the IRS-mandated special tax notice. As the plan administrator, I gave myself (the plan participant) the special tax notice together with a blank distribution request form. I filled out the distribution request form as the participant, requesting a direct rollover of the non-Roth after-tax contributions and earnings to a Roth IRA. I approved the distribution request as the plan administrator.

I then sent an Investment-Only Retirement Account One-Time Withdrawal Form to Fidelity. I already had a Roth IRA at Fidelity. I simply chose to distribute the entire non-Roth after-tax account (but leave the account open for the next year) in-kind as shares to the Fidelity Roth IRA.

After the shares were rolled over, I printed the transaction history that showed the value of the gross distribution and the original non-Roth after-tax contribution. The small amount of earnings would be taxable.

Issue 1099-R

When you do a rollover from a workplace 401k plan, the plan administrator will report it to the IRS and send you a 1099-R. When I’m administering the plan myself, I’m responsible for issuing the 1099-R and reporting it to the IRS.

I had to figure out what to put where on the 1099-R. The IRS has Instructions for Forms 1099-R and 5498. I read the first 17 pages for 1099-R. The pertinent part for what I needed to do is in just one small paragraph on page 5:

For a direct rollover of an eligible rollover distribution to a Roth IRA (other than from a designated Roth account), report the total amount rolled over in box 1, the taxable amount in box 2a, and any basis recovery amount in box 5. (See the instructions for Box 5, later.) Use Code G in box 7.

It’s all in the instructions. The hard part is to separate the wheat from the chaff and figure out which part applies. If I contributed $10,000 as non-Roth after-tax and I distributed $10,100, it’s just

- The plan’s name and EIN as the payer

- My name and SSN as the recipient

- 10100.00 in box 1

- 100.00 in box 2a

- 0.00 in box 4 (no federal tax withheld)

- 10000.00 in box 5

- code ‘G’ in box 7

- 0.00 in box 12 (no state tax withheld)

Once you know what to do, actually issuing the 1099-R is easy. I created an account at tax1099.com. They e-file 1099-Rs with the IRS (and some states) for $2.90 per form. I filled out the form visually. They would do the rest. I downloaded copies for the payer (the plan) and the recipient (the participant) as PDF files.

***

For $195 per year paid to Ascensus for document maintenance plus the minimal cost for postage and issuing the 1099-R, I was able to put an extra chunk of money indirectly into my Roth IRA. It was quite worth it. Obviously, you have to know what you are doing if you want to play plan administrator and plan trustee yourself. As the plan administrator and the plan trustee, you also have other duties besides what I wrote in this article. Laws and regulations are complex. There are many ways to mess up. Get professional help if you’d like to pursue this option.

Employee Fiduciary can include non-Roth after-tax contributions in their solo 401k plans. They charge a $500 setup fee and $500 in base administration fees plus 0.08% of plan assets per year.

If your self-employment income is in the right range — not too low, not too high — it can be worth it to enable the mega backdoor Roth option in your solo 401k. You can use my spreadsheet Solo 401k Maximum Contributions to find out how much room you have for non-Roth after-tax contributions and then decide whether it’s worth the effort and the cost.

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

Shalom says

Hi Harry, thanks for replying.

I didn’t understand at first that these 3 companies you mentioned in the other article are in-fact providers that offer such plans.

With your permission: one last question, I hope you don’t mind. It’s probably a very basic question:

So, clearly all the big players like Fidelity, VanGuard etc.. – they don’t offer non-Roth after-tax contributions.

I wonder:

– Why don’t they actually offer that? Is there some ‘objection’ to this product?

– Who can ‘provide’ such plans? Is there some requirement of law to be able to offer such plans and then each provider decides for themselves which feature to offer in it?

Thanks again,

Shalom.

Harry Sit says

1) We can only speculate. The market is too small. Fidelity and Schwab don’t even offer the Roth 401k feature in their plan.

2) A pre-approved provider creates plan documents. The IRS issues an opinion letter to the pre-approved plan provider if the plan document meets all legal requirements. The provider then makes its plan available for employers to adopt. Some administrators can “resell” the plan from a pre-approved provider.

Shalom says

Thanks much Harry!

Shalom.

Shalom says

Hey Harry,

I apologize if I ‘keep on piling questions’, I hope it’s okay. I’m resolved to do what you explained here so take it as a compliment, you convinced me it’s both doable and worth it, so I hope you don’t mind my questions to minimize my mistakes:

– When playing all these roles myself (as you do) then what is left of the Plan Provider, is it only to get the plan, adopt and sign, and then receive occasional updates which mostly are in events of laws changed? Is there anything more I should expect to hear from my plan provider?

– What are the events where I need to contact my plan provider post adoption? sounds like nothing really, cause as long as I’m good with doing all myself then really there’s nothing for them to do, is there anything I’m missing?

– What I need to make sure is that my plan will have the ‘after-tax’ contributions feature. That will allow me to contribute up to the 56k (2019 limit). Then the conversion to Roth IRA could either be: in-plan Roth conversion or even out-out-plan, meaning converting to a pre-existing Roth that is unrelated to the plan. I guess the in-plan conversion may only be better for convenience but that’s all. Is this understanding accurate?

– Lastly, and probably most importantly to me:

I also am employed by a company where I have a 401k (as an employee) where I contribute the max 19k (2019 limit) and receive some matching ($3000 per year).

My understanding is that there is a ‘individual contribution’ bucket and a ‘profit sharing’ bucket where both buckets are for any and all 401k plans I have (whether solo or not). So, the limit of the ‘individual bucket’ is 19K, so if I contribute all of that in my employer’s 401k, then I will not be able to contribute as individual to that bucket in my solo401k. Also, since I’m getting $3000 of my employer in profit sharing then that will reduce how much I can contribute to my solo 401k after-tax: so it won’t be $56, but it’ll be $53k.

– Is the above an accurate understanding?

– Lastly, is the $56K limit also includes the ‘individual contribution’ bucket, in which case I’ll only be able to contribute 24k (56k – 3k – 19k) or is the individual bucket separate/independent of the profit sharing bucket?

I hope I didn’t exhaust you. I hope you’ll reply – it’s a big help and I thank you much in advance.

Shalom.

Harry Sit says

This is area where one should not attempt to DIY. There are simply too many ways to mess up. A solo 401k isn’t just a bigger IRA. The IRS expects you to behave like a real employer and know all the rules imposed on employers that sponsor a 401k plan. Hire a Third-Party Administrator (TPA) and let them drive the administration. A real TPA does not just provide the document and updates. They will tell you when to do what. They will have procedures and documentation. They will help you calculate the contribution amounts. You will still sign in your different roles.

You can use my spreadsheet linked in this post to estimate the amount you can contribute. The calculation is different depending on whether you are set up as a sole proprietor or an S Corp.

Shalom says

Thanks much Harry for all your help.

Shalom.

Charles says

Thank you for this amazing article! I’ve been doing a bit of reading about QBI and it seems like maxing the profit-sharing may no longer make sense, b/c it does not lower your income when calculating the QBI deduction. Have you considered updating your spreadsheets to account for this wrinkle? I’d be happy to help make the changes.

Harry Sit says

If you are talking about the spreadsheet for calculating the contributions, the value for “Desired profit sharing (0% – 25%)” is already an input field. Set it to 0% if you would like to make no profit sharing.

Stephen says

The decision to do this seems to me to come down to whether one feels like taking the risk of administering the plan ones self or not.

Getting the document is straight forward.

Using a TPA seems to involve either losing control of the assets and/or paying asset based fees that reduce any benefit gained (if there are substantial assets).

Self administering opens up a risk of getting it wrong, especially if you are rolling over substantial amounts into these new accounts. Imagine rolling over substantial amounts and then finding out you made a mistake and they are no longer “qualified”.

There is less risk if this is started from new, but if you have existing 401K assets from the same income stream they have to be rolled over as you cannot have 2 401Ks. This magnifies the risk of getting the self administration wrong.

So the question I have is there any way to quantify the “other duties” you mention in this article? I am already responsible for the 5500-EZ, I understand the notifications you outline in this article and the 1099-R process, just looking or more info on what else before making the jump…..

SG says

Hi Hary! Thanks for your great posts. I was planning on doing the same switch as you did. I too currently have a template fidelity plan as well. Quick questions:

1) Did you close the Flidelity plan before starting the new plan? (I could rollover the plan current plan assets to my employer plan and start a plan from scratch.)

2) In your spreadsheet, why do the allowed contributions depend on whether the elective contribution is to a 403(b) vs a 401(k)?

3) I have a mega-backdoor Roth going on in an employer 401(a). Would that interfere with this?

Harry Sit says

If you’d like to do this, go with Employee Fiduciary. You will amend the existing plan to Employee Fiduciary’s plan document and roll over your assets to Employee Fiduciary’s custodian. Don’t terminate your current plan. A quirk in tax regulations says a 403(b) aggregates with a solo 401(k) but a 401(k) does not. An employer 401(a) doesn’t affect the solo 401(k).

William says

Hi Harry,

Really enjoy this post. I’m curious if 5 years later you think the complexity/hassle of doing this was worth it? Ie I see that there is “some” benefits but your time/thought is worth something too.

Curious if you feel different 5 years in!

Harry Sit says

It was worth more when I worked full-time at a W-2 job with self-employment only on the side. Because the employee contributions went into the plan at the W-2 job, I had more room in the solo 401k for non-Roth after-tax contributions. Now that I’m 100% self-employed, the employee contributions are also going into the solo 401k, which reduces the room for non-Roth after-tax contributions. Because the overhead to create and maintain the plan is the same, it all depends on how much room the extra effort really gives you.

Your self-employment income needs to be in a sweet spot to make it worthwhile. If it’s low, you can’t contribute much anyway. If it’s high, you’re able to max out the solo 401k without non-Roth after-tax contributions. Use the spreadsheet linked in the last paragraph to find out whether your self-employment income is in a good spot.

Reed says

But for the high income self employed with a defined benefit plan (DB) this is definitely worth it. Max contribution to the DB plan will limit the pretax employer profit sharing contribution to the solo 401k but it does not limit the employee aftertax non roth contribution. So aftertax non roth contributions can be used to max out solo 401k. Might be worth paying a TPA to set this up and manage both the 401k and DB plan.

Harry Sit says

Sure. The complexity in a solo 401k with non-Roth after-tax contributions is lower by an order of magnitude than the complexity in setting up and maintaining a DB plan. If you already went that far with a DB plan, you might as well take another step.

Sasha D. says

Hi Harry,

I hope you can help me with conversion from Non Prototype Solo 401k sub account after tax to a Roth IRA.

All accounts are with FIDELITY.

Contributions to solo 401k after tax subaccount of:

2022 $48,500.00

2023 $35,000.00

Total contributions $83,500.00

Gains $1,637.13

Total in after tax account: $85,137.13

1. Can I convert to Roth IRA only the $83,500.00 contributions and leave the gains in the after tax account? Does this violates pro rata?

2. Can the $1,637.13 of gains be moved to the solo 401k pre-tax subaccount? If so do I use the same Fidelity form I used to convert the contributions to Roth IRA? (This account was open when solo 401k was set up)

3. Can the $1,637.13 of gains be moved to a traditional IRA? (Do not have traditional IRA would have to open a new account)

4. Can the $1,637.13 of gains be moved to a SEP? (I have a SEP account currently open)

Thank you so much. Your Mega-Roth articles are of great help and I was very appreciative that you posted so many details.

Sasha D.

Harry Sit says

1) You must distribute proportionally out of the after-tax account. If you only distribute $83,500, a part of it will still be earnings.

2) The earnings can’t go directly into the pre-tax account in the solo 401k.

3) It can go into a Traditional IRA or a SEP-IRA but I don’t think it’s worth it. You already paid taxes on $83,500. Paying taxes on another $1,637 to move it into a Roth IRA isn’t a big deal. Don’t sweat it.

My after-tax account was closed after I emptied it last year. I had to ask them to re-open it. Maybe leave $1 behind to avoid the hassle.