As I mentioned in my previous post Recharacterize Backdoor Roth, I requested recharacterization of my Roth IRA conversions in 2011 and 2012. Since this is the first time I did this, I’m documenting the process here.

Why Recharacterize?

Recharacterizing an IRA can mean two things:

- recharacterizing contributions OR

- recharacterizing a conversion (from Traditional to Roth)

You may want to recharacterize contributions to an IRA because you find you exceeded a legal limit:

- You thought you are eligible to contribute to a Roth IRA but now you see you are not allowed to because your income is too high. Your original contributions to Roth IRA must now be recharacterized to a Traditional IRA, which then can be converted to Roth at a later time.

- You thought you are eligible to take a deduction for your Traditional IRA contributions but now you see you can’t. You are better off recharacterizing your original Traditional IRA contributions to Roth.

Or you may want to recharacterize your original contributions simply because you changed your mind.

Recharacterizing a Roth conversion means undoing the conversion. Something went wrong and now you’d like to fix it.

When you recharacterize contributions, money goes from one IRA to another IRA as if you contributed to the other IRA in the first place. When you recharacterize a conversion, money goes from your Roth IRA back to a Traditional IRA, as if you didn’t convert it.

Find the Form

Because my Roth IRA is with Vanguard. I’m showing how I did it with Vanguard. I also looked at the recharacterization forms for Fidelity and Schwab. They are very similar to Vanguard’s.

First find the necessary form. From Vanguard’s home page for personal investors, click on Forms on the top right.

Type recharacterize in the “Search forms and literature by title or phrase” box.

Print and fill out the “Authorization to Recharacterize IRA Assets” form. You can’t do it online.

Fill Out the Form

The form is relatively simple if you understand the terminology.

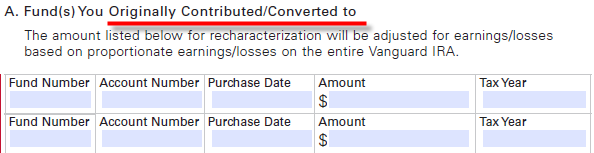

First it asks for the date and amount of the original conversion. Look this up in account history.

For my 2011 conversion, I converted $5,000.15 from a money market fund in the Traditional IRA to a total international stock index fund in the Roth IRA. So I filled in the fund number and account number of the total international stock index fund in the Roth IRA together with the purchase date and tax year.

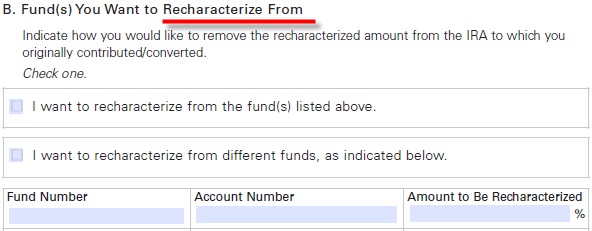

Next it asks where you want them to take the money from for the recharacterization.

Since I’m still holding the same fund, I just checked the box “I want to recharacterize from the fund(s) listed above.” If you moved on to something else, you will have to designate one or more sources for where they should take the money. Note you only designate the source(s) as a percentage, not the actual dollar amounts. They will calculate the dollar amount.

Wait for Share Transfers

After you sign the form and mail it, just wait. Vanguard processed my recharacterization very quickly. I mailed the form on a Monday. Vanguard completed it on Thursday of the same week.

Some shares moved from my Roth IRA to my Traditional IRA. There were no selling or buying. I still have the same fund and the same total number of shares, just in different accounts.

The calculation for how much should be moved is mandated by the IRS. The amount includes a proportional gain or loss in the account after the original contributions or conversion. If you really want to know how the math works, see Worksheet 1-3 in IRS Publication 590. The actual federal regulations are 26 CFR 1.408-11. Normally you don’t have to worry about the math because your IRA custodian’s computers know how to do it.

I still double checked Vanguard’s math just for curiosity. No surprise, they did it correctly.

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

Tom says

Great article that explains the process.

What if one held Vanguard Admiral Share classes in one IRA and the contribution was recharacterized into another IRA using Admiral Share funds where no Admiral Share funds existed before? Would they be automatically exchanged to Investor Class shares after the share transfer?

linda says

hi, Harry:

my daughter made contribution to her Roth IRA this year, before finding out her MAGI will be over limit.

a). so she has to do this: 1. re-characterizing her contribution to Roth IRA to a non-deductible traditional IRA; 2. then convert it back to Roth, correct? is there any waiting period (one month?) before she can covert back to Roth just try not to jeopardize things (step transaction doctrine??)

b). She also has Roth 403b that will direct rollover to her Roth IRA after she leaves the service. is there any problem that she should be aware of running those 2 actions in the same year? (pro-rata rule???)

Thanks

Harry Sit says

She can recharacterize her Roth IRA contribution as a traditional IRA contribution. Whether she can pay minimal tax when she converts it to Roth depends on what other traditional, SEP or SIMPLE IRA(s) she has. There is no official guideline for how long she should wait. Pick a time she feels comfortable with.

Rolling over a Roth 403b to a Roth IRA has nothing to do with this.