Tax efficiency becomes a factor when you have investments in regular taxable accounts (versus a tax advantaged accounts such as a 401k or IRAs). Because you have to pay taxes on interest, dividends, and realized gains, an investment that loses less of its returns to taxes is said to be more tax efficient.

Tax efficiency is a non-issue if you only have tax advantaged accounts.

Which one of these two investments is more tax efficient?

- A stock mutual fund is expected to earn 7% a year; its returns are taxed at a 12% rate.

- A bond mutual fund is expected to earn 2% a year; its returns are taxed at a 30% rate.

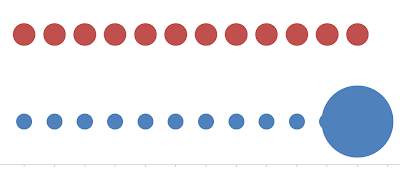

For simplicity’s sake, I spread the eventual capital gains tax when you finally sell the stock mutual fund into a constant tax rate per year.

The blue dots represent the actual pattern of taxes on a stock mutual fund: smaller when you hold, larger when you sell. The red dots represent a normalized pattern: same amount every year.

The stock mutual fund gets the preferential tax treatment. Qualified dividends and long-term capital gains are currently taxed at a lower rate than ordinary income. In this example, the stock mutual fund loses 12% of its returns to taxes instead of 30% lost by the bond mutual fund.

That makes the stock mutual fund more tax efficient relatively. But on an absolute basis, the stock mutual fund loses 7% * 12% = 0.84% to taxes each year whereas the bond mutual fund only loses 2% * 30% = 0.6%.

Which number is more important? The relative, 12% vs 30%, or the absolute, 0.84% vs 0.6%?

If you want both investments and you can’t put both of them into tax advantaged accounts because there is a limit on how much you can contribute to tax advantaged accounts, you will have to prioritize. You should focus on the absolute number: 0.84% for stocks and 0.6% for bonds in our example, because that’s how much you will lose to taxes if you hold that investment in a regular taxable account.

In other words, the investment with a larger absolute tax cost should be sheltered in tax advantaged accounts. In this case, the stock fund should go into the shelter first, leaving the bond fund outside if there isn’t enough room.

The expected return plays a big role here. Back when bond funds were yielding 6%, 8%, the correct asset placement strategy was to shelter the bond funds. Now bond funds are only yielding 2%. The low bond yield changed the picture. The strategy must follow.

The new strategy will be very obvious if our bond fund is actually a money market fund paying 0.05%. Although the income from the money market fund is fully taxable, there is no point in sheltering it because it’s too small. It’s not worth worrying about. It would be a mistake if you waste precious space in tax advantaged accounts on sheltering 0.05% yield while leaving stock mutual funds paying 2% dividends out in the cold unsheltered.

Trade Spaces

What if you are still operating under the old rules and you already have your bond funds in tax advantaged accounts and your stock funds in taxable accounts? Chances are you don’t want to trade your stock funds for bond funds because doing so would trigger capital gains tax.

You can swap gradually with new cash. Next time when you are about to buy more shares of stock funds in your taxable account, sell some bond fund shares in your tax advantaged account and buy stock fund shares there. Use your available new cash to buy bond fund shares in your taxable account. This way over time you will build up more money in stock funds inside your tax advantaged accounts and more money in bond funds outside.

Step-Up In Basis At Death

Don’t do the swap if you have more money than you can spend in your lifetime and you will leave your vast fortune behind to your heirs very soon. Assets left behind in a regular taxable account receive a step-up in basis at death. Unrealized capital gains are forgiven when you die. In such case you will want to have stock funds in taxable accounts in order to maximize tax free unrealized capital gains.

I’m assuming most people will need and use the money themselves.

What If Interest Rates Go Up

What if interest rates go up and change the picture again? Lose that fantasy. Have you not got the message from the Fed? Bond yields are not going back up to 6%, 8% any time soon. I quote this from Vanguard senior economist Roger Aliaga-Díaz (emphasis added by me):

“Our outlook for bonds is tame and really depressed,” [Aliaga-Díaz] said. “Forget about the years that bond returns were 6% to 8%. We’re talking about 1% to 2% for 10 years. If rates don’t rise, you have those yields. If rates do rise, you have capital loss (in bond value). All of this is tilted to the downside. That’s a reality, even for a long-term investor.”

* Source: With investors still focused on bonds, more talk of a bubble, Vanguard.com, September 28, 2012

If rates do go back up, no problem. Your bond funds in taxable accounts will have a capital loss. Remember bond values go down when interest rates go up. You can reverse the trade and take the capital loss. No harm is done.

Having fixed income money in taxable accounts is the more tax efficient strategy in the current low interest rate environment. Doing so also affords us many opportunities not available in tax advantaged accounts (for example buying I Bonds at 1.5% higher yield than 5-year TIPS). If the environment changes, switching back is not a problem because it won’t trigger capital gains tax.

[Photo credit: Flickr user adafruit]

[Updated on Dec. 1, 2012. Changed numbers in the example to avoid confusion.]

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

Charlie says

This is very interesting stuff. I would be taking a long look at this kind of strategy, but I use the G Fund as my primary fixed income holding.

I did have a thought about another situation. The absolute advantage of holding bonds in taxable right now seems to depend on the fact that capital gains will be realized at some point. What about investors who are young and don’t expect to realize capital gains for a very long time? Over the 10 years we expect to see low bond yields, they would lose more to taxes if they hold bonds in taxable. They also might sacrifice a lot of opportunities for tax loss harvesting, where they can save taxes at their top marginal rate. When they eventually do realize gains, they might be able to offset capital gains with prior losses, or depending on future tax law may be in a lower income bracket at the 0% capital gains rate. They may decide to give appreciated shares to charity. There seems to be a lot of assumptions one has to make to decide which course is best, and a lot of ways to avoid paying capital gains taxes on stocks for a very long time.

Lynne says

This post makes a great point about an important way our thinking needs to change in a sadly long-term low-return environment for bonds.

But it seems to assume we have as good choices in our retirement accounts as we do in the taxable accounts where we can hold anything.

In reality, my company’s 401K plan has few index funds. Our only international stock fund option, for instance, is a very expensive actively managed fund, so I’d hate to buy that rather than one of the international stock index funds I can buy in my taxable account.

Of course, there’s always my ROTH IRA, but I can only contribute $6,000/yr to that account, and that’s where I keep REIT and high yield bond funds, which I think still belong in a tax-advantaged account.

Harry says

Charlie – Yes, I did say this is assuming that you will need and use most of the money yourself as opposed to accumulating a pile for the step-up in basis at death or donating to charity. As long as you will use the money yourself, longer time only means the investment will build up more unrealized capital gains. It does not reduce the tax rate on the gains. Stocks pay dividends. Right now the dividend yield is about the same and sometimes higher than the bond yield. The preferential treatment of dividends over interest and wages is scheduled to go away. At best the preference will shrink. You are not paying that much less in taxes on dividends even before amortizing the eventual capital gains tax.

Harry says

Lynne – I hope you are contributing the max to your 401k before investing in a taxable account although your 401k has more expensive investment options. You still come out better off that way in most cases. See my previous post Alternatives to a High Cost 401k Or 403b Plan. Most plans have relatively better options for stocks than for bonds. Usually they at least have a S&P 500 index fund. It’s one more reason for putting stock funds in tax advantaged accounts. As I will post in the coming weeks, there are many opportunities to earn more than bonds in taxable accounts.

dd says

Good article, well thought out, which doesn’t follow the crowd, provides insight; which is why I read this blog.

joe says

Great article. I’ve given this idea a lot of thought myself. Looking at an index s and p 500 fund from vanguard, since 2000 it has returned with dividend on average 2.25% or so. The vanguad TIPS fund which is not tax efficient has returned 7% per year. Using these numbers I would want to shield the TIPS bond fund.

Using your strategy you need to be able to guess what the returns will be. Since bond yields are very low right now it may be better to shield stock mutual funds in tax sheltered accounts. But if inflation rears its ugly head, maybe you want to shield your TIPS funds?

Harry says

joe – Buying I Bonds in taxable account will help with that dilemma. Existing TIPS can stay in tax advantaged accounts.

Harry @ PF Pro says

I never thought about in relative vs. absolute terms. But that would seem to make sense to put your low yielding bonds in an after-tax account.

Is this not a similar concept to your last article(guest post)? Wouldn’t you want to hold stocks in your Roth and bonds in your 401k for the same reason or am I missing something?

Harry says

Harry @ PF Pro – No, this is different. The guest post talks about two tax advantaged accounts: Roth and Traditional. The conclusion is that it doesn’t matter. Here I’m talking about taxable accounts versus tax advantaged accounts (whether Roth or Traditional).

White Coat Investor says

Great post. In fact a great month worth of posts. Love the circle graphic.

I just wanted to add one thing. While nominal yields may not rise any time soon (at least if the Fed gets its way), the total yield on inflation-indexed securities may very well go up quite high if inflation spikes. Say you have a TIPS with a real yield of 0%. But then we get unexpected 5% inflation. You’ll be wishing you had those stocks in taxable then, especially when you have to pay the taxes on the phantom income.

Otherwise, great article turning the conventional wisdom on its head. It’s getting pretty old to not only have low dividend yields on stocks but also low yields on bonds. Perhaps it’s time to be investing in real estate- low prices and low interest rates. If only it wasn’t such a hassle.

CoderDude says

My first question is whether it’s realistic to assume stocks will have significantly higher returns than bonds. The example provided was stocks returning 7% and bonds 2%. As a counterpoint, in 2002 William Bernstein predicted Large US Stocks would return 3.5%, while investment-grade corporate bonds would also return 3.5%.

Next, consider the range of outcomes for stock returns. If stock returns are equal to or less than bond returns, it’s better to hold stocks in taxable. Since stocks didn’t do very well, you will really appreciate the tax savings. If stock returns are sufficiently larger than bond returns, then in hindsight, it would have been better to hold stocks in tax-advantaged. However, since stocks did very well, you can afford to pay more in taxes without compromising your lifestyle. Stocks in taxable is a win-win. Either they have low return and you play low taxes, or they have high return and you can afford to pay the higher taxes.

Finally, holding stocks in taxable allows you to tax-loss harvest. I have heard that tax-loss harvesting can increase after-tax returns by as much as 1% per year (though I don’t know the validity of this claim). Anecdotally, I was happy to be holding stocks in taxable in 2008 since I was able to bank large losses.

Harry says

Your first question has no answer. No one knows what returns will be in the future. The numbers given in the article are an example to show that the absolute tax loss is the more important number to consider, not the relative number. They are not a prediction of future returns.

Second, even if stocks end up having similar returns to bonds, you are still not saving much taxes by holding bonds in tax advantaged accounts because you can buy muni bonds in taxable account for not much loss in income.

Finally, you can only harvest losses from recent purchases. If a crash comes in year 24, there is not much loss to harvest. The 1%-per-year number is greatly exaggerated.

theo says

Nice analysis, turns conventional wisdom on its head.

You don’t seem to emphasize the fact that stocks’ capital gains are eventually taxed at the higher marginal income tax rate if held in pretax retirement accounts instead of the lower (thus far) long term capital gains in regular taxable accounts.

Is that because you assume that the gap in taxation will disappear or become smaller in the future?

CoderDude says

What is the formula for determining whether it’s better to hold stocks or bonds in taxable at a particular time? Is it based on things like taxable bond yield, municipal bond yield, stock yield, dividend and capital gains tax rates, etc?

If I do switch to holding bonds in taxable, when would I know the right time to switch back?

theo says

@Coder It would be interesting to see TFB do some real-life calculations according to current tax rates but it is obviously difficult to project future rates…

I don’t think TFB suggested switching existing holdings in taxable accounts since that would trigger capital gains. His suggestion is to redirect new contributions 🙂

Come to think of it though leaving aside anyone’s particular case, as a general rule capital gain tax rates are at historic lows and assuming (as most do) that these rates will go up, this could represent a golden opportunity to lock in the current rates by realizing those capital gains this year 🙂

Of course in particular cases one could have lower income in the future which could lead to potential lower capital gain tax rates, though IMHO that would be an exception rather than the rule…

Harry says

@theo – The tax on withdrawal from a tax deferred account is taken care of by the tax deduction when you made the contribution. From that point on, the governments (federal and state) own a portion of your account. The remainder you own is tax free. The actual percentage owned by the governments depend on tax laws in the future but it doesn’t depend on what you hold in the account. Whatever you hold in the remainder is tax free regardless. Therefore the often cited “convert capital gains into ordinary income” argument is not valid.

@CoderDude – Yes it’s based on those things. You know it’s the right time to switch when those things change. I updated my Tax Cost Calculator which uses those factors as inputs.

theo says

The total porfolio after all taxes are paid in the end does depend on the capital gain tax rate and where stocks are held …There are 2 opposing forces: deferring taxes on the higher yielding asset (- i.e. stocks) will allow for compounding to work its magic. OTOH it is only in a taxable account that you can benefit from lower capital gains taxes on stocks – this benefit disappears when stocks are held in a tax deferred account where everything is taxed as regular income in the end.

I had difficulties wrapping my head around the theoretical stuff and had to go for an example 🙂

Sorry for the wall of text, I hope nobody gets a heart attack 🙂

In each case the tax deferred account starts from a higher amount (57.15k) which after 25% tax ~ equals the taxable account amount (42.85).

I assumed a marginal income tax rate of 25%, annual bond yield of 4%, annual stock capital gain of 7% (ignoring stock dividends and bond capital gains for simplicity).

The only difference between the 2 cases is the capital gain tax which is 25% in the first example and 15% in the second.

Case #1: capital gain and income tax both are 25%, 30 years horizon.

Stocks in Tax Deferred.

57.15*(1.07^30)*0.75= 326.28

Bonds in taxable:

42.85*(1.03^30)= 104.01

total after 30 years=

430.29

Bonds in TD.

57.15*(1.04^30)*0.75= 139.02

Stocks in taxable:

42.85*((1.07^30-1)*0.75+1)= 255.35

total portfolio after 30 years=

394.37

This portfolio total is ~10% lower than the former scenario.

Case #2

capital gains tax 15 %, income tax 25%, 30 years horizon.

Stocks in TD, bonds in taxable (unchanged from case #1 above):

57.15*(1.07^30)*0.75= 326.28

42.85*(1.03^30)= 104.01

total after 30 years same as in case #1 above:

430.29

Bonds in TD:

57.15*(1.04^30)*0.75= 139.02

stocks in taxable:

42.85*((1.07^30-1)*0.85+1)=283.68

total after 30 years:

422.70, minimally lower than the reverse and better than in case #1, now only about 2% difference.

The only thing that I wanted to show through this example is that there is a tradeoff for stocks being taxed at capital gains rates vs stocks in tax deferred accounts where they are taxed at marginal income rates.

jmk says

Theo, when you say bonds in taxable generate

42.85*(1.03^30)= 104.01

is this assuming municipal and not taking out taxes?

In other words should the equation minus 25%?

theo says

@ Jmk: the 25% were already deducted when I used 0.03 instead of 0.04 annual interest rate. Since you lose 25% each year from 0.04 rate it makes it equivalent to an annual interest rate of 0.03, hence I used 1.03 in the calculation instead of 1.04.

Harry says

theo – I’m not surprised that a lower capital gains tax rate will lower the cost of holding stocks in taxable account. If that large blue circle at the end in my chart is smaller it will mean smaller red circles representing the average cost per year. It doesn’t contradict what we discussed so far. It’s also consistent with my tax cost calculator. When you lower the tax on capital gains, the tax cost for holding stocks in taxable gets lower.

allan roth says

If both the yield on the bond and the stocks are equal (say about 2.2%), then one benefits today with a lower tax rate on stocks held in the taxable account. Where the benefit really comes, however, is in the withdrawal phase. IF long term capital gains are still taxed at a lower rate than ordinary income, then the last thing you’d want to do is to hold stocks in the tax-deferred account. That’s because you’d be converting higher expected growth from a long-term capital gain to ordinary income.

I agree that any investment yielding .05% or less has very little in tax consequences. But one shouldn’t have any significant amounts of funds earning this rate.

Harry says

Allan – Thank you for stopping by. It’s been established that a tax deferred account is equivalent to a Roth account when the tax rates at the time of contribution and at the time of distribution are the same. For most people when the tax rate in retirement is lower, a tax deferred account is better than a Roth account. I think of it as a “super Roth” account. Earnings in a Roth account are tax free. More so in a “super Roth” account. There’s no converting capital gains to ordinary income. If someone doesn’t like paying tax on the capital gains, there’s always the choice of using a Roth account to begin with or converting to Roth along the way.

Retail Investor says

Your understanding that … “If long term capital gains are still taxed at a lower rate than ordinary income, then the last thing you’d want to do is to hold stocks in the tax-deferred account. That’s because you’d be converting higher expected growth from a long-term capital gain to ordinary income”….. is common but wrong.

Harry has tried to debunk it by making the universally-agreed statement that outcomes from Roth = trad when tax rates don’t change …. and everyone accepts that the Roth’s benefit is from PERMANENT sheltering of profits ….. there for the tradIRA’s benefit is also from the same effect. Profits are not taxed on withdrawal. The w/d taxes are an allocation of principal between the account’s two owners/funders.

I know what logic you are thinking proves your point. You can see it debunked on page 7 of this paper https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2636609 RRSP = tradIRA, and TFSA = Roth

allan roth says

Harry – my pleasure. I didn’t even see Roth mentioned in your piece though I agree that a traditional IRA is superior IF one has a lower marginal tax rate in retirement. Since we don’t know future tax rates, I happen to believe all three pots (taxable, tax-deferred, and tax-free) give some diversification against Congress.

What I’m referring to is that it’s still better to hold stocks in the taxable account and not in the tax-deferred. The location is at least as good now if the yields are similar but much better later on. Stocks have the likelihood (no guarantee) to grow faster and, when withdrawn, will incur ordinary income. If one had located the stocks in the taxable account, they would get a lower LTCG rate, at least under current law.

Robert Bradley says

Interesting analysis, but I think it ignores risk. In the example above, putting stocks in the (let’s say traditional IRA) shelter first results in lower portfolio risk than putting bonds in the shelter on an after tax basis, since taxes in the Tr. IRA are higher.

Only when modelling and equalizing risk can we make a definitive statement like: ” the investment with a larger absolute tax cost should be sheltered in tax advantaged accounts.”

Additionally, the point Allan Roth was trying to make – that you’d rather have a large tax friendly taxable account than a large Tr. IRA to draw down in retirement – is a further reason this decision isn’t quite so simple.

Harry Sit says

Please see my reply to Allan Roth above. Because of the up front tax deduction, a traditional IRA is at least as good as a Roth account. In many cases it’s better than a Roth. If it’s worse, you can always convert it to a Roth now. Therefore we are really comparing money in a Roth or a super-Roth and money in a taxable account. Whatever you leave outside the Roth or super-Roth, you pay the tax cost.

Brian says

Harry, what about harvesting capital losses? It seems one would get far more capital losses from a volatile asset class like stocks than from bonds. In a high tax bracket during the accumulation phase, this could be worth $1,000+ a year in taxes saved. Lowering the basis creates a bigger tax obligation down the line, but potentially in a much lower tax bracket.

Harry Sit says

The effect of tax loss harvesting is very small, as you will see in a post tomorrow. It also gets smaller and smaller as your portfolio grows.

Retail Investor says

Although I agree that the metric “$taxes paid in year 1 per $100 invested” (%rate of return * %effective tax rate) is WAAAY better than the metric “income’s %tax rate” at identifying the assets that benefit most from Asset Location …. It is still lacking because it fails to consider the compounding value over years, from high growth assets. Time matters.

The three factors deciding the issue are (1) growth rate of asset, (2) effective tax rate on profits and (3) time. It is the first that is most important. You can see this at work and play with your own numbers with the spreadsheet linked from http://www.retailinvestor.org/rrsp.html#taxfree

RRSP = tradIRA, TFSA = Roth

David says

Posted the following to a different forum but haven’t gotten many comments and it is related to the discussion here so giving it a shot…..

I have been using the following article as my guide for placing assests in taxable, tax deferred and tax advantaged accounts. https://www.bogleheads.org/wiki/Tax-efficient_fund_placement

I think I have the stock vs bonds placement down – stocks in taxable and bonds in tax deferred but wondering about stocks vs low yield money market accounts. Prior to reading about tax efficient investing, my thoughts were to place high growth assets (stocks) in tax deferred accounts and low yield money markets in taxable accounts since the money markets are paying so low that even if they are taxed at a higher rate, it is a higher rate of a low number so less tax per year than say a stock with a decent yield taxed at the lower dividend rate.

After reading the article above have switched to thinking that it is better to have the stocks in the taxable account since if they have a large amount of growth over the long run, they will (hopefully) be taxed at the lower capital gains rate vs if they are in a tax deferred account, when taken as RMD’s they will have to be taxed as income at a higher rate most likely. Having the lower growth cash assets in a tax deferred account would mean smaller RMD’s, less taxed at higher income rate and possibly keeping social security from being taxed.

I know a lot of this is unpredictable since tax rates can change but any thoughts will be greatly appreciated!

Harry Sit says

From the link you posted:

“You must consider both the return and the tax rate. With higher bond yields conventional wisdom is to hold bonds in tax-advantaged accounts. Today low yields are common, and a bond fund with an expected return of less than 1% can be more tax efficient than a stock fund with an expected return of 7% even though the bond fund’s return is taxed at a higher rate.”

David says

Looking at some numbers assuming 15% capital gains tax rate and 25% income tax rate while working and in retirement

Case 1 – 10k stocks in taxable account earning 7% and 10k bonds in tax deferred account earning 1% –

10k in stocks returning 7% growing over 30 years = 10,000 x (1.07^30) = 76,122, 66,122 (gain) taxed at .15 capital gains rate = 66,122 x 0.15 = 9918, 76,122 – 9918 = 66,204

10k in bonds earning 1% over 30 years = 10,000 x (1.01^30) = 13,474 taxed at income tax rate of .25 = 13,474 x .25 = 3368.5, 13,474 – 3368 = 10,106

total = 66,204 + 10,106 = 76,310

Case 2 – 10k bonds in taxable account earning 1% and 10k stocks in tax deferred account earning 7%

10k in bonds returning 1% over 30 years = 10,000 x (1.01^30) =13,474, 3474 gain taxed at income tax rate of .25, 3,474 x .25 = 868.5, 13,474 – 868.5 = 12,605.5

10k in stocks returning 7% growing over 30 years = 10,000 x (1.07^30) = 76,122, taxed at .25 income tax rate = 76,122 x 0.25 = 19,030.5, 76,122 – 19,030.5 = 57,091.5

total = 12,605.5 + 57,091.5 = 69,697

This example shows the big advantage of keeping stocks in a taxable account to take advantage of the lower capital gains rate. If there are numerical examples to contradicts this, please post.

David says

A small correction to the math – bonds in the taxable account will be taxed every year and not at the end of the 30 year period. The new math is included below. Case 1 (76,310) – allocating stocks to taxable and bonds to tax deferred is still the far better choice than case 2 (69,604) – allocating bonds to taxable and stocks to tax deferred in this example.

Looking at some numbers assuming 15% capital gains tax rate and 25% income tax rate while working and in retirement

Case 1 – 10k stocks in taxable account earning 7% and 10k bonds in tax deferred account earning 1% –

10k in stocks returning 7% growing over 30 years = 10,000 x (1.07^30) = 76,122, 66,122 (gain) taxed at .15 capital gains rate = 66,122 x 0.15 = 9918, 76,122 – 9918 = 66,204

10k in bonds earning 1% over 30 years = 10,000 x (1.01^30) = 13,474 taxed at income tax rate of .25 = 13,474 x .25 = 3368.5, 13,474 – 3368 = 10,106

total = 66,204 + 10,106 = 76,310

Case 2 – 10k bonds in taxable account earning 1% and 10k stocks in tax deferred account earning 7%

10k in bonds returning 1% over 30 years = 10,000 x (1.0075^30) = 12,513

10k in stocks returning 7% growing over 30 years = 10,000 x (1.07^30) = 76,122, taxed at .25 income tax rate = 76,122 x 0.25 = 19,030.5, 76,122 – 19,030.5 = 57,091.5

total = 12,513 + 57,091.5 = 69,604.5

theo says

Your example is fundamentally mistaken because your two cases are not identical. You have to level the playing field by correcting for the pre-tax post tax situation.

If you put 10k in the tax-deferred account, you only invest 7,500, the rest is owned by the taxman. Now of course if you take more risk (by investing 10k in stocks and 7.5k in bonds) you’ll get more growth than the reverse (10k in bonds and 7.5k in stocks), but that’s a mistake that leads you down the wrong path to the wrong conclusion 😛

In my example above (from a few years ago) I accounted for the pre-tax post-tax situation, and that correction, no doubt, should lead you to the opposite conclusion, i.e. stocks should be held in a tax-deferred account in your example 🙂

Harry Sit says

Redo the math assuming your tax advantaged account is a Roth account. You will see different results.

You contributed to a Traditional account and you are keeping it as a Traditional account because you think it will do better than a Roth account, even though you will pay taxes when you withdraw. Otherwise you would’ve contributed to Roth to begin with or converted to Roth already. Therefore your Traditional account is actually a super-Roth account. For the purpose of figuring out which asset classes in which account you should just treat all your tax advantaged account as Roth accounts. When you do that you also don’t have to worry about RMD.

David says

Theo,

I read over your example and maybe we are comparing two different things. I am only trying to allocate assets that are already sitting in tax deferred and taxable accounts. I don’t think I have to correct for the pre tax- post tax situation because I have already paid the taxes on the taxable accounts and now trying to figure out how to place assets that are already in each category.

Harry,

I will redo that math as you suggested soon and post assuming Roth.

Thanks and appreciate the feedback.

theo says

David, you get better results in case 1 because you put 10k in stocks (taxable). In case 2 you take less risk and put only 7.5k in stocks (after tax calculations), hence you end up with less assets in the end. This has nothing to do with tax efficiency, it is because you take more risk and invest a higher portion of your portfolio in a higher yield asset (7%) in case 1.

David says

I think what this example and discussion is showing is that if you want to minimize year to year taxes then the original premise of sticking low yielding bonds in a taxable account will give you lower taxes initially but when it comes time to pay taxes on the tax deferred held stocks you can be stung in a bigger way when you have to pay tax at the income tax rate vs the capital gains rate.

Another advantage of keeping stocks in the taxable account will be to make your RMD’s smaller and the capital gains from stocks will not push you into a higher tax bracket.

Retail Investor says

I disagree with David’s conclusion (May 7 5:13pm) as to what the discussion has shown.

I don’t understand why Theo’s point has been ignored. A Traditional account is larger when the same after-tax $savings is put in a Roth account – because contributions reduce taxes and allow greater savings. The larger balance funds the eventual withdrawal tax – so during its lifespan not all of the Traditional account is YourMoney. The w/d tax is an allocation of principal between owners (the gov and you), not a tax on profits. That is why $outcomes from a Roth and Traditional are equal when tax rates don’t change.

The differing benefits for both accounts from Asset Location choices is not determined by w/d taxes on profits in a Traditional account. The benefits come mostly from the compounding-over-time benefit of permanent sheltering of profits from tax. Those relative benefits change over time. Given a long enough time span the attribute most important is the asset’s rate of return. (figure 2, page 7 at link below)

Trying to determine universal rules from singular examples won’t work (even when you get the before/after tax issue correct). Instead measure directly the $benefit over time for any asset with stipulated tax rates and rates of return. Instead of modelling any presumptions about holding periods before capital gains are realized, include that factor in the input variable for the effective annualized tax rate. Use the Excel tab called “Cumulative Benefits” at http://www.retailinvestor.org/xlsxSecureCopy/Challenge.xlsx

The effective tax %rate on profits is not the deciding metric. Neither is ‘tax efficiency’ which measure the $taxes paid in year one (Rate of return multiplied by tax rate). You must consider the compounding benefit over time – which makes the %rate of return the most important metric.

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2317970

David says

Thank you Harry, Theo and Retail Investor,

Haven’t had much time to completely digest but get what you are saying Theo about the assets held in tax deferred is a joint ownership between individual and taxman. I am thinking the same applies in a taxable account to the capital gains. This will be a small initial factor but over a longer time period, the capital gains could make up a majority of the value of the taxable balance.

To Retail Invsestor – the paper you posted looks very good and I need to reread it. I have an older version of excel and going to see if I can convert your xlsx to xls version.

John says

Harry,

I have a related question wrt Emerging and Developed markets ETFs. Should these be placed exclusively in Taxable accounts or in tax deferred like IRAs? I realize that in a taxable account I can deduct the foreign tax paid which I can’t do when these are in in IRAs. Is there any benefit in placing foreign stocks in IRAs?

FinancialDave says

Harry, I’m sorry I did not have time to read all the posts to see if it was addressed but let me pose this question to you.

You said tax efficiency is a non-issue for any tax-advantaged account so I am guessing you will get this correct.

Let’s say your working tax rate is 25% and your retirement withdraw rate for the funds in question is also 25%.

Will you have any more money in either situation below?

Case 1: you put your $10,000 stocks earning 10% in the IRA and $7500 (after-tax) bonds earning 3% in the Roth. (Tax equivalent amounts in each account)

or

Case 2: You swap it around and put $10,000 of 3% bonds in the IRA and $7500 of 10% stocks in the Roth.

You withdraw both after 10 years.

Dave

Retail Investor says

@Financial Dave

The outcomes would be the same. Your example shows correct Asset Allocation math. The IRA’s $10,000 is not all ‘your’ money. $2,500 is the government’s money that they gave you (via the tax reduction on cont) to invest for them). That portion of the account will be repaid to them at closing. So in both cases you are investing only $7,500 of your own money in each asset class.

But be clear that this does not show anything about Asset Location or Tax Efficiency. This is about Asset Allocation and how it should be calculated. After the AA is calculated base on your money, you gross up the asset holdings in the IRA account to account for the gov’s money. http://www.retailinvestor.org/rrsp.html#aa

You won’t find any of the experts or advisors doing this though, because they fail to appreciate where the benefits of the IRA come from.

FinancialDave says

@retail investor,

The benefits from the IRA come from the fact that for “most” average investors, the GREATER portion of their retirement money will be spent in tax brackets that are lower than their marginal working tax brackets, which thus benefits the IRA over the Roth (or in Canada the RRSP over the TFSA.)

What many fail to realize is that the most important comparison amounts to your marginal rate while working and your effective tax rate (at for your tax advantaged funds being spent.) Many just compare marginal rate to marginal rate and are totally off base. Here is an article comparing an average middle income couple retiring gin 2018 @ age 70:

https://seekingalpha.com/article/4182914-risk-roth-ira-revolution-part-ii

One reason to express caution from thinking you know where assets should be located is to realize that in order to do that you have to be able to tell the future, which I don’t profess to be able to do.

Sure you can make a reasonable guess that bonds might underperform stocks, but there are time periods where you could have been wrong over as many as 10 years with such thinking.

FinancialDave says

Harry,

One comment to all these posts about whether a taxable account is more tax efficient or not, even though it is a very complex subject once you add the variable tax rate of SS into the mix. If you assume 85% of your SS is going to be taxed and your highest marginal rate is 12%, having only qualified dividends and LTCG in your taxable account gives it the EXACT characteristic as a Roth account, so everything you know about a Roth applies here!

Mainly, what “I” know about a Roth is it is very tax ineffecient because if you spend money in a marginal tax bracket lower than the average tax of the Roth contributions or conversions you are wasting money, over spending IRA money for those tax brackets.

Retail Investor says

@FinacialDave

You cannot generally conclude the Roth has worse outcomes (you call ‘tax inefficient’) while limiting your view to only situations where the effective tax rate on withdrawal is lower than the rate at contribution … creating the IRA’s bonus = $draw * change in %rates. There is always the possibility of draws from an IRA at a higher effective tax %rate creating a penalty. The possible bonus/penalty is an independent factor, and adds/subtracts from the $equal net benefit from permanently sheltering profits from tax that both accounts give you.

The tax rates used for calculation of the possible bonus/penalty for the IRA is the effective tax rate that includes the impacts of things like the loss of gov’t benefits in retirement, but also the benefit from qualifying for benefits while contributing. All else equal, if the IRA draws result in some SS being taxed, then the effective withdrawal rate will be larger than at contribution, creating a penalty that makes the Roth’s net benefits bigger in comparison.

The effective tax rate on withdrawal does not get compared to the effective tax rate on investment profits in a Taxed account. This %rate on profits is an input into the compounding benefit from permanently sheltering profits from tax (= difference in outcomes between $compounded at after-tax rates vs at nominal tax rates) (also = the time-value-or-money calculation for FV of a Growing Annuity). This is the benefit that is always exactly equal for both IRA and Roth.

Use the first table at https://www.advisorperspectives.com/articles/2017/12/11/the-unambiguous-tax-deferred-retirement-account . The 10% difference in tax rates between cont and withdrawal create the 10% bonus benefit ($498). That is completely different from …….

The 15% tax rate on profits in a Taxed account (but not Roth or IRA) creates the different growth rates (5.5% vs 4.7%). This difference creates the $784 benefit from permanent profit sheltering in both tax shelters.

FinancialDave says

@retail investor,

Not exactly sure what you are saying. It looks like the example sited is $750 after-tax (25%) bracket while working – taxable account and Roth account.

Later in retirement 15% tax bracket (neglecting any investments that create dividends and tax drag) the results would be exactly the same in both cases since taxable accounts are taxed at zero for those in the 15% bracket??

FinancialDave says

In reading the above again I am guessing you meant the taxable account is in the 15% tax bracket because the investors marginal rate is still 25% for his other ordinary income. This example seems trivial because everyone “should” know that the taxable account generally is not going to win vs the Roth or IRA – the best it can do is tie the Roth with zero taxes on LTCG and qualified dividends.

FinancialDave says

@ retail investor,

Let me explain the seriousness of the Roth example when a couple saves all their Roth money within a marginal tax rate of 25%. This example is made clear in my link above but let me lay it out here and let’s leave out SS in the first go because SS really doesn’t make a difference as to whether any Roth money should be spent.

2018 tax rates, couple is deferring SS to age 70 and only spending down tax advantaged accounts – whichever is the most efficient to spend. Below is the math:

$24,000 (or $26,600 age 65 and up) is spent TAX-FREE from the IRA

$24,000 to $43,050 is spent in 10% bracket from the IRA

$43,050 to $101,400 is spent in 12% bracket from the IRA

$101,400 to $189,000 is spent in 22% bracket from the IRA.

I ask you just where is the average investor of modest means going to spend any of that Roth money to his advantage?

Also, if you assume the couple needs at least $100k of income from SS and tax-advantaged accounts the Roth account still cannot spend $1 in what I would call a tax-efficient way, over an IRA, since even though it is possible to pay no taxes in retirement, the Roth savers will run out of money before the IRA savers, as my article clearly shows.