As I mentioned in a previous post — Pay Someone By Zelle: Daily Limit and Recurring Payments — the ACH system in the U.S. is set up to be bidirectional by default. A routing number and an account number can be used to both deposit money into the account and withdraw money from it.

This makes it difficult to transfer money to another person’s account because people don’t want to reveal their bank account number, fearing you might take their money. As a result, person-to-person transfers are typically done through third-party services such as Venmo, Zelle, PayPal, or Cash App. Both parties must use the same service. You can’t do it if you have Venmo and they have Zelle. Either you must also sign up for Zelle, or they must also sign up for Venmo.

Each third-party service has its limitations. They work for smaller transfers, but they often don’t work for larger ones. Bank of America limits Zelle transfers to $3,500 per day. If you want to transfer $5,000, you’d have to split it into two days. Many banks have even lower Zelle transfer limits than Bank of America.

Trusted Parties

Some people don’t mind sharing their bank account information with you when they know and trust you. Say you’re giving annual gifts to your adult children, or you’re paying a mom-and-pop landlord monthly. They’re willing to give you their bank account for you to deposit into. Even then, it’s not that easy to transfer money to their account.

Many banks only allow linking to accounts that you own. They require verification to confirm that you have control over the target account. It’s done traditionally by micro-deposits. Lately, many banks have moved to using instant verification services such as Plaid or Mastercard Data Connect (formerly Finicity). This requires logging into online banking at the target bank. Banks see who owns the target account in this process. They won’t allow the link when names don’t match.

Intra-Bank Transfers

Some banks support transfers between customers within the same bank. Many credit unions also have this feature. They call it member-to-member transfers. Suppose your child is attending college out of state. If both of you have accounts at the same bank or credit union, you can transfer to your child’s account internally.

It’s feasible to make this arrangement with a child. It’s difficult to do with your sister unless you happen to use the same bank.

Bill Pay or Mail a Check

You can use Bill Pay to pay an individual. The Bill Pay provider will mail a paper check. Or you can mail a check yourself. Both are subject to delivery delays and potential loss or theft. That’s not a good way.

Wire Transfers

You can also send a wire transfer, but many banks charge a fee for wires. Even if you get free wires from your bank, many banks also charge a fee for receiving a wire. Making your family member or your landlord pay a $15 fee to receive money from you isn’t that great.

Push-Only ACH

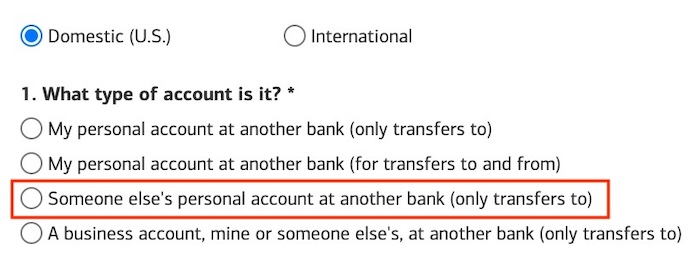

Fortunately, some banks allow linking to another person’s bank account. They don’t require ownership verification for this type of link when they disallow withdrawing money from the target account. For instance, when you link an external account to Bank of America, it asks you whether you want the account to be “only transfers to” or “for transfers to and from.”

Selecting “for transfers to and from” requires ownership verification through Plaid. Selecting “only transfers to” doesn’t. If you use Bank of America, see the detailed walkthrough in How to Link an Account to Bank of America for ACH Push.

Fidelity

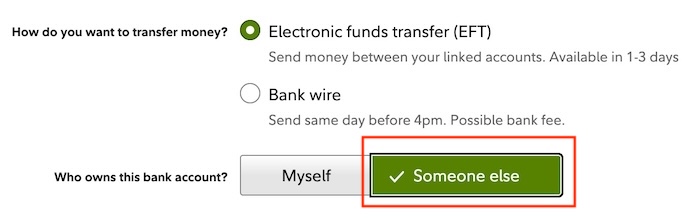

I use Fidelity for my banking (see 2 Ways to Use Fidelity as a Bank Account). I can link another person’s bank account to my Fidelity account. Like Bank of America, Fidelity asks whether the account is owned by me or by someone else.

Linking a bank account you own creates a bidirectional link: you can push money to that account or pull money from it. It requires ownership verification. Linking a bank account owned by someone else creates a push-only link: you can transfer money to that account, but you can’t withdraw from it. It doesn’t require ownership verification.

Fidelity will go through a banking industry process called “prenote” to confirm that the target account is valid. A prenote requires waiting at least 3 business days before sending the first transfer. Give it about a week of setup time before you need to transfer money. Once the link is fully set up, the transfer arrives on the same business day if you request it early enough in the morning, or on the next business day if you miss the cutoff. It’s almost as fast as a wire transfer, and it’s free to receive.

You can transfer up to $100,000 per day by EFT/ACH from a Fidelity account. It’s not possible to transfer that much by Venmo or Zelle.

Fidelity’s online interface only supports ad hoc transfers to another person’s account. You can’t schedule transfers for a future date or set up recurring transfers to another person, whereas you can set up scheduled or recurring transfers to your own accounts. If you need to set up scheduled or recurring transfers to another person, call customer service to see if they can set it up on their side.

***

Venmo or Zelle works well for buying things listed on Craigslist or Facebook Marketplace, or paying a gardener or a house cleaner. They don’t work as well for transferring larger amounts to a trusted party. Having an account that supports ACH to another person’s account makes it work in that scenario. The receiving side doesn’t require any special setup. They only need to give you their routing number and account number. It’s free on both sides.

If your bank also supports ACH transfers to another person’s account, please include its name in the comments so other readers know where to go besides Fidelity and Bank of America.

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

Joe says

I wonder if Ally Bank does this? I’ll do some research.

AC says

Fidelity does not charge a fee for wire out to another person or company. When we closed on our new house, the closing company insists only take wire transfer even though it was a high amount for the closing. We cash flow the purchase.

Harry Sit says

Sending a wire works well for real estate closing. The closing company isn’t charged a fee by their bank for receiving wires. It’s problematic when you send a wire to a family member. It’s free to you to send, but it’s often not free to your family to receive. Many banks and credit unions charge $10 to $15 for receiving a wire, whereas it’s unheard of to charge a fee for receiving ACH transfers.

Nello says

Do any banks support free ACH transfers to individuals and companies for their (small) businesses customers?

Thank you.

Harry Sit says

Banks usually offer business accounts access to ACH transfers to pay employees, contractors, and vendors. Whether they charge separately or make it part of the business account package is up to each bank. The bank that I use for a business checking account offers it under the Business Bill Pay feature. It’s included in the business checking account package for the monthly fee, which is waived when the account maintains a minimum balance. I believe this is a common practice for small business accounts.

indra says

Thank you for this useful information. If Fidelity would allow a completely separate account for banking totally detached from my investment account I would consider opening one.

Larry says

Of course you can do this. Simply open another account at Fidelity. I’ve done this.

Harry Sit says

It depends on how “totally detached” you want it to be. Fidelity offers a Cash Management Account (CMA). By default, it shows up together with your existing accounts under the same login. You can transfer between the CMA and your existing accounts if you want to, but the CMA doesn’t automatically draw from your other accounts (unless you take explicit steps to set up an overdraft, which I don’t recommend). Please read more in 2 Ways to Use Fidelity as a Bank Account.

That’s sufficient separation for most people, while allowing internal transfers to add funds to the CMA or to move excess cash to investment accounts as needed. If you want a separate login for the CMA and not see your existing accounts at all, and not see the CMA under your current login, you can call customer service to get a new “G number” and put the CMA under the new G number. That’ll be more “totally detached.”

Jen says

We have been using ACH for our business for a few years since fees have tripled. We use Frost Bank to pay contractors and it works well. We use Zelle as well when some contractors prefer it. Quickbooks fees run us $15 per transaction and from what I’ve read online, our fee is low. A few years ago, the fee was $3!

Steve says

Somewhat related.

Fidelity makes transferring shares in-kind to another person’s Fidelity brokerage account quick and easy. If you want to transfer shares from your Fidelity brokerage account, perhaps as a gift, all you need is the recipient’s name and Fidelity account number.

The transfer can be submitted by telephone to a Fidelity rep, or by completing the form “Transfer Between Existing Fidelity Accounts” and taking it to a Fidelity investment center. Money transfer lock must be disabled on the sending account.

I took the form to Fidelity office one afternoon. The transfer was completed early the next morning.

jen says

I did not know that! Thank you for sharing.

Ying says

Both persons have Fidelity CMA accounts. Can you set up once (prenote) and do subsequent push transfers without having to set-up each time?

Harry Sit says

One person can treat the other person’s Fidelity routing number and account number for ACH as any other routing number and account number from an external bank. It works the same way, and it requires only setting up once.

TWBCommonCents says

I just did this through Fidelity to transfer funds to my parents. It does have a limitation though, in that you can’t automate recurring transfers easily. You can do one time, instant transfers from the website, but recurring transfers requires filling out a multipage form and mailing it to Fidelity to setup. This adds complexity and time delays to both the initial setup and any changes you may want to make down the road.

I did end up using Zelle, as it does allow automated transfers directly into their account. As noted, it did require both their routing and account numbers, and fortunately, the amount is below the daily maximum.

Harry Sit says

A reader said if you have the account already linked, you can call Fidelity customer service to have them set up recurring transfers on their side.

David says

I do this with Ally.

It’s actually in the Zelle interface. You add a new recipient and select “bank account” instead of phone number of email address. Then you type in the routing and account numbers.

Harry Sit says

Is that path still subject to the same Zelle daily, weekly, or monthly transfer limits?

David says

I don’t know for sure, but I suspect it’s subject to the same limits as Zelle, which says $5,000 daily and $10,000 monthly for me.

Larry Too says

The article said: “Venmo or Zelle works well for buying things listed on Craigslist or Facebook Marketplace…” I can’t imagine a scenairo that this would be a good idea. From a seller’s POV, that is an easy way to be scammed by the buyer. Even if it is safer for the buyer, I would still be nervous. I have always heard that the golden rule on this is to never use these services unless you personally know or do business with the person on the other end. Maybe things have changed?

Harry Sit says

The golden rule you’ve heard is about the risk in paying and not receiving what you expect to receive. True, don’t use them for shipped items. That’s not an issue for in-person pickups.

Venmo and Zelle are safe for the seller because they’re not reversible. Venmo has a purchase mode that gives the buyer the right to dispute the transaction. If you see the buyer has checked that box, you can refuse to release the item.