Hi, I’m Harry. I’ll show you the nuts and bolts of managing your money.

401k, IRA, investing, insurance, taxes, … I lived, breathed, and wrote about these for so many years. No fluff, just concrete first-hand learning and sharing.

Explore Topics

Recent Posts

Better Than Venmo and Zelle: Transfer Money with ACH/EFT

Having an account that supports ACH to another person’s account makes it easy to transfer a larger amount than using Venmo or Zelle.

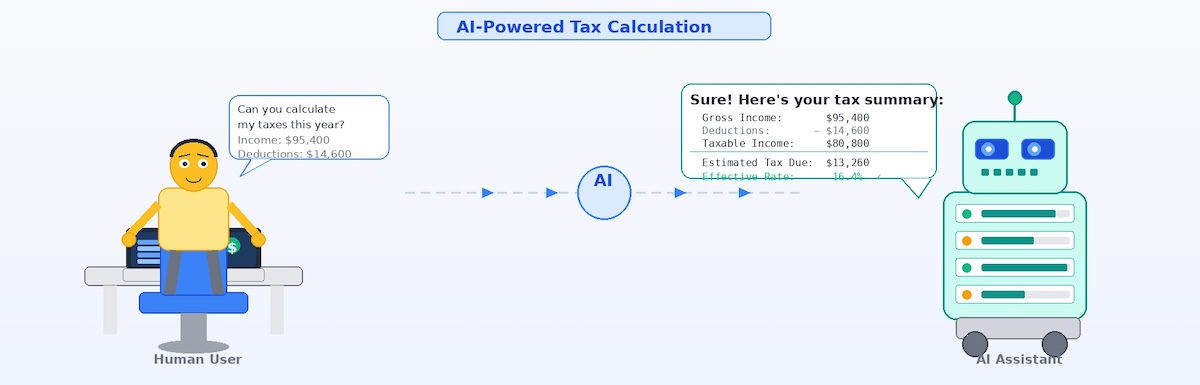

Which AI Calculates Taxes Correctly?

Whether AI can calculate taxes correctly depends on the complexity. An online tax calculator is faster and more accurate if you know which one to use.

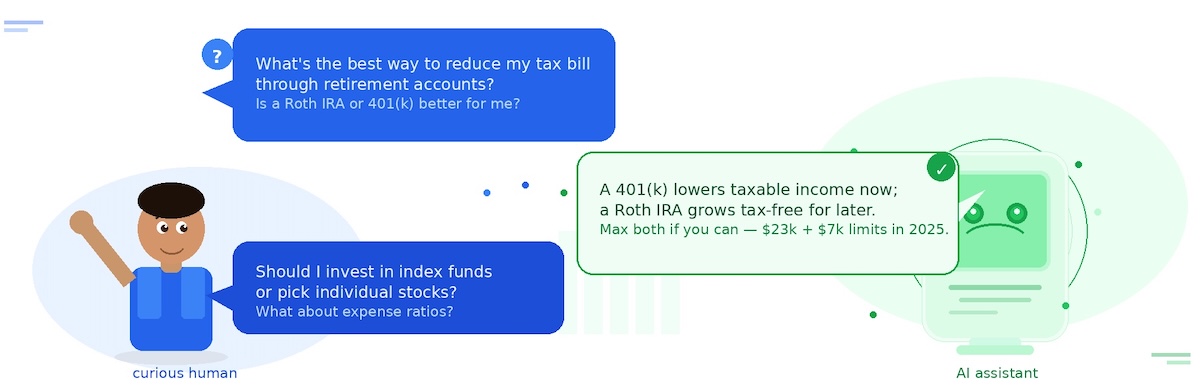

AI Gives Better Answers Than Google

AI gives you a good baseline. The less you know about a subject, the more AI will help. Use AI for how to apply knowledge to your specific situation.

A Simple Annual Financial Review Template

We use this annual financial review template to recap the previous year and plan for the current and future years.

How I Bought a Home Without an Agent After the NAR Settlement

You can buy a home without a buyer’s agent and save a lot of money when you’re prepared. Here’s how I did it.

Real Life Experience with a Deferred Fixed Annuity (MYGA)

A deferred fixed annuity, aka MYGA, is like a CD issued by an insurance company. It worked as advertised but I’m not renewing or buying more.