I updated this article I first wrote two years ago. It’s still relevant today since Congress made the 0% tax rate on long term capital gains permanent in early 2013.

2013 is coming to an end. It’s been a great year for the stock market. For those in the 10% and 15% tax brackets, you may want to realize some long term capital gains to reset your cost basis higher and take advantage of the special 0% tax rate on long term capital gains.

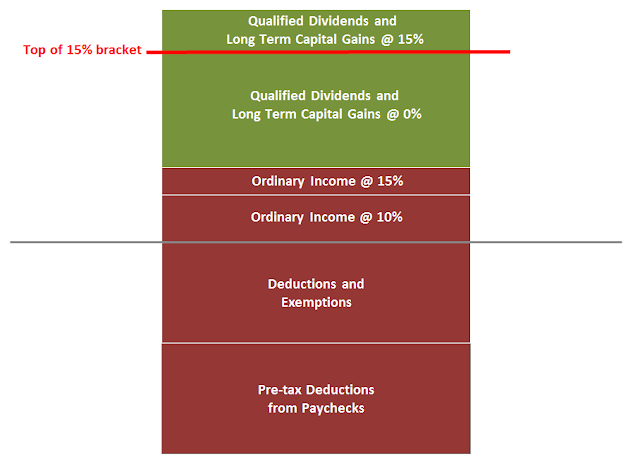

To qualify for the special 0% long term capital gains tax in 2013, you must have a taxable income before any capital gains under $36,250 if you are single, under $72,500 if you are married filing jointly.

Note these numbers are taxable income. If you add back pre-tax deductions from your paychecks (401k, health care, flexible spending accounts), personal exemptions ($3,900 per person including dependents), above-the-line deductions, standard deduction ($6,100 single, $12,200 married filing jointly), and itemized deductions if higher than standard deduction, the actual gross income cutoff for this benefit is much higher: probably more than $50k single and more than $100k married filing jointly.

I would say more than half of the people in the country qualify.

To take advantage of the special 0% tax rate on long term capital gains, sell some investments with unrealized long term capital gains and immediately buy them back. There is no wash sale on realizing gains. Your cost basis will reset higher, which means you will pay less in taxes in the future.

You will want to realize just enough long term capital gains so that when the gains are added to your other income and after subtracting the exclusions, exemptions, and deductions, your taxable income still stays right below the cutoff: $36,250 (single), $72,500 (married filing jointly).

If you accidentally overshoot a little, it’s not a big deal. Only the amount above the cutoff gets taxed at 15%. The vast majority of your realized gains are still taxed at 0%.

You will pay state income tax on the realized gains. You will pay that sooner or later anyway unless you are planning to move to a no-tax or low-tax state in the future. So weigh the cost of state income tax against the benefit of no federal capital gains tax before you do this.

If you don’t qualify but you have elderly parents who qualify, tell them about it. Or gift them some appreciated stocks or fund shares and let them sell for free.

Reader Sri brought up an excellent point about capital loss carryover from previous years. If you use this strategy, your long term capital gains are first reduced by your capital loss carryover from previous years.

Social Security recipients may find the capital gains will increase the tax on Social Security benefits. After passing a hump though, additional long term capital gains are still tax free. Please read this follow-up if you are receiving Social Security benefits: Tax on Capital Gains While Receiving Social Security Benefits.

If you are going to get a subsidy for buying health insurance from the exchange under Obamacare in 2014, you may consider realizing more capital gains in 2013 than just under the top of the 15% tax bracket, if doing so will help you stay off the premium subsidy cliff in future years.

[Photo credit: Flickr user Lucky Larry]

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

Kevin says

I thought doing what you describe would trigger a wash sale. Or do wash sales only concern losses?

Harry Sit says

Kevin – Only losses. No wash sale on gains.

nickel says

Great tip, TFB. Essentially tax gain harvesting. 🙂

dd says

Great advice and remember to have teens and young adults also take advantage of tax gain harvesting.

Sri says

I’m a bit confused. How does this work if I have a carryover loss from previous years. I’m in a situation where my taxable income is just above the cutoff, but if I count a $3000 carryover loss from previous years, then I’m under. In this scenario, does it make sense to sell gains?

Thanks for the help.

Harry Sit says

Sri – The loss carryover must be burned against any capital gains before being applied to ordinary income. Therefore you don’t qualify for this if your income is above the cutoff.

Maggie says

Thank you for the help! I have one question– do I need to wait a certain period of time before buying back the shares? Is the same day ok?

Harry Sit says

Maggie – No you don’t have to wait a certain period of time. Some mutual fund companies have restrictions on when you can buy back in after you sell out of a fund. If you are talking about regular stocks or ETFs, you can buy back on the same day if you want.

Ben says

So if you gift someone appreciated stock they could sell it and not pay income tax if they are in a lower tax bracket right? (assuming total gift is under annual gift limit).

Harry says

The gain must be long-term. They get your cost basis and purchase date. As long as the gain still fits between their income and the red line, they pay 0% federal income tax.

austin says

Okay, so I’m reading this in 2014. Does this still work?

Harry says

Yes it still works, and it will work indefinitely until laws change.

Mox Moeschler says

Hi Harry, I’ll be surprised if you are still monitoring this but here goes.

We need to sell my mother in laws family home currently in a revocable trust. She as trustee. her only means of income is 15,00+- Social Security. So 0% tax bracket. The sale of the home will produce a capitol gain of over 1MIL. Will she owe capitol gains tax? I noticed on a 1040 capitol gains is entered on line 13 and added to come to your taxable income. then putting her into A hefty tax bracket for adjusted gross income.

I am definitely missing something as the irs even states ” the regular tax rate that would apply is 10% or 15% capitol gains rate would be 0%

How might i get a truer understanding how this works

Thanks

Harry Sit says

See the red and green stacked bars in this article. 0% stops at the top of 15% bracket when the gains are put on top of other income. The remaining gains are taxed at 15%, 20% and 23.8%.

Mox Moeschler says

Wow thanks so much Harry for starting me thinking correctly, hopefully, on this answer

. Of course a elder law attorney and financial counselor will be called in.

Just to get a start here’s what I grasp from your answer. The first 15% bracket cap (37,650) is not taxed. then the difference (377,400) between that cap and the 20% cap 415,050 is taxed at 15% then anything over 415,050 is taxed at 20% ? but where does 23.8% kick in. Am I close to getting it?

And thanks again

Harry Sit says

Actually it should be 15%, 18.8% and 23.8%. The stacked bar chart in this post shows where the breaks are: Fiscal Cliff Deal and Dividends and Capital Gains.

Mox Moeschler says

so ,it looks like at least on the right line of thought?

Thanks Harry

Harry Sit says

Yes, on the right track.

Mark says

Related question regarding capital gains on a home. I live in NYC where home prices seemingly always on the rise. When I reach the 250k threshold of tax free capital gains, should I think about selling and re-buying something else and reset my cost basis so future gains are also tax free? Any calculators out there where you can estimate property value increase per year, and how many years you plan to stay to show where the break even point is with tax savings vs cost of selling/re-buying to reset your cost basis? Thanks!!

Harry Sit says

I will make one. Stay tuned.

Marc Pinneo says

Hi Harry,

I a little confused by your reset of cost basis.

If I have $1,000 in stock and I bought it for $1,000 (i.e. no capital gain or loss if I sell it), and I sell it and buy it right back again at almost the same price, my cost basis is still $1,000 only now I have started the clock over again so if I sell it in the same year with a capital gain, it will now be short term instead of long term, right?

I’m sure I am missing something here, but I don’t see what the benefit is for this scenario.

Thanks,

Marc

Harry Sit says

The title says “Reset Cost Basis Higher By Realizing Capital Gains.” If you have no gains to realize, you are not resetting your cost basis higher. You reset only when you (a) have long-term gains; and (b) pay 0% federal income tax on realizing those gains. When you reset your cost basis higher, you reduce your future capital gains.