I usually don’t write about things that don’t affect me, because as a reader once said to me, topics that pique the author’s own interest create the best content. I’m making an exception here because it’s important enough if by chance you happen to be able to take advantage.

I’m talking about making non-Roth after-tax contributions to your 401k or 403b plan, followed by rolling the money over to your Roth IRA. Jim Dahle at The White Coat Investor coined it as the “mega backdoor Roth.” I’m going with that. If your plan cooperates, you can put up to an additional $43,500 a year into your Roth IRA! If you are married and both of you have a cooperative plan, you can put up to an additional $87,000 a year into two Roth IRAs!

Before you get super excited, I have to warn you that not everyone can do it. Neither I nor my wife can. Sadly if your plan doesn’t cooperate, there’s nothing you can do about it. You are completely at the mercy of your employer’s 401k or 403b plan. If your plan doesn’t allow it, you are simply out of luck.

Employers that allow it tend to be large employers. Being in a large plan is still not a guarantee. For example, the federal government’s TSP is huge but it doesn’t allow it.

Between my wife and me, we worked for 8 different employers in the last 20 years. None of the 8 employers allowed non-Roth after-tax contributions. If as Vanguard said that 40% of the plan participants can do it, we would have a 98% probability of hitting at least once (1 – 0.6^8 = 0.98), but we struck out 8 out of 8.

It’s similar to having access to a 457 plan. Some people can contribute to both a 403b plan and a 457 plan, which gives them double the annual contribution limit. My wife and I never once had access to a 457 plan. I doubt we will ever. Meanwhile, some people always had one even when they move from one employer to another.

Feeling Lucky?

How do you know if you are lucky or not? Check two things:

1. whether your employer’s 401k/403b plan allows non-Roth after-tax contributions; and

2a. if it does, whether such contributions can be distributed while you are still working there (“in-service distribution”); or

2b. if the plan also offers a Roth 401k option, whether the non-Roth after-tax contributions can be rolled over to the Roth 401k part of the plan (“in-plan Roth rollover”)

#1 is the most critical piece. If you don’t have #1, you are dead out of luck. You can tell by the way you set your payroll deduction for your 401k or 403b plan. Typically you always have the choice of pre-tax. Some plans allow Roth contributions, but that’s NOT what we are looking for. You want after-tax contributions that are not Roth. Roth is after-tax, but after-tax isn’t necessarily Roth.

If you score, you then ask about the “in-service distribution” or “in-plan Roth rollover” rules of your plan. The law allows rolling over non-Roth after-tax contributions and earnings thereon while you still work at the employer. Most plans simply follow the law and they don’t place further restrictions. If you score on #1, chances are you will score on #2 as well. Make sure whomever you ask clearly understands you are talking about taking out non-Roth after-tax contributions, not taking out pre-tax contributions or Roth contributions, which is prohibited by law before you terminate or reach age 59-1/2 (or die or become disabled).

Some plans can be more restrictive. Some plans would suspend the employer match if you take money out. Some plans don’t allow taking any money out until you terminate or until you reach age 59-1/2. Some plans limit the frequency of these in-service distributions, for instance no more than once a year. Some plans charge a fee for each distribution. You will want to know whether your plan is more restrictive than the law.

Score!

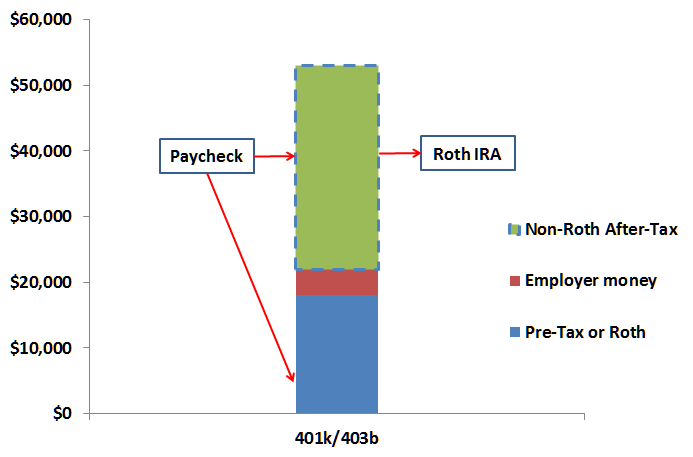

Suppose you get lucky and you score on both points. Now what? You choose to make non-Roth after-tax contributions from your paycheck. Then you request a rollover of the non-Roth after-tax money and its earnings to a Roth IRA or to the Roth 401k part of the plan. Either way works. See Mega Backdoor Roth: Convert Within Plan or Out to Roth IRA? The end result is that you have more money in your Roth IRA or Roth 401k. The maximum in 2023 is $66,000 minus your $22,500 pre-tax or Roth contributions minus your employer’s match and/or profit-sharing contributions.

If you can only do it once a year, so be it. Do it once a year. If you are able to do it more frequently and you don’t mind doing it, do it more frequently.

If you can only roll it out until you terminate or until you reach 59-1/2, which you expect to be in the next few years, it still would be worth it. Just contribute now and wait it out. See the follow-up article Mega Backdoor Roth Without In-Service Distribution.

You will pay taxes on the earnings of your non-Roth after-tax contributions between the time you contribute and the time you roll it out to your Roth IRA or Roth 401k. So be it. Pay taxes on the earnings. You can get fancy and have the earnings go to a traditional IRA or even maneuver to roll the earnings back into the plan. I won’t bother unless the earnings are substantial. You already got lucky with being able to do the mega backdoor Roth, which many can’t do. You don’t have to push it further. The earnings usually won’t be much anyway.

Some say keep the non-Roth after-tax contributions in a money market fund before you take it out. I disagree. Not only is it difficult to do, because plans typically don’t allow you to designate funds by contribution type, but it’s also unnecessary. Paying taxes on earnings is better than not having earnings to begin with.

Discrimination Test

Plans that allow non-Roth after-tax contributions must go through a discrimination test to make sure they don’t disproportionately benefit highly compensated employees. If you are a highly compensated employee and your plan fails the test, the plan will have to return some of your contributions and earnings thereon to you the next year. If by that time you already took the money out, it can become a tax mess.

If you are not a highly compensated employee, you don’t have to worry about this. If you are not sure whether you are a highly compensated employee, ask your HR.

Your plan may or may not be at risk to fail the test. However, if you want to avoid this possibility altogether, wait until October 31 the next year to request your distribution for the previous year’s contributions. October 15 is the extended deadline for a plan to file its report to the IRS. By that time it should be clear whether the plan passed or failed the test for the previous year. You can also ask your HR whether the plan passed the test. Once you know it passed, you are clear to request your distribution.

Self-Employed

What if you are self-employed? No mainstream solo 401k providers such as Vanguard, Fidelity, Schwab, TD Ameritrade, or E*Trade allow non-Roth after-tax contributions in their plans. You can pay a service provider a modest fee for a custom plan that allows it. I hope the publicity on the mega backdoor Roth will prompt the mainstream solo 401k providers to add this feature, but I’m not holding my breath. I went ahead and got my own plan. See Mega Backdoor Roth In Solo 401k: Control Your Own Destiny.

Priorities

If you are able to do this, where does it stand in terms of priorities? I see it this way:

- Max out pre-tax or Roth 401k/403b, including age-50 catch-up contributions if applicable

- Max out deductible traditional IRA or Roth IRA

- Max out non-Roth after-tax 401k/403b rolled over to Roth IRA (“mega backdoor Roth”)

- Regular taxable account

If you are not maxing out the first two items yet, don’t worry about this mega backdoor Roth. If you are in a position to max out all three, take full advantage before you mess with regular taxable accounts.

Let’s just say I’m jealous of you if you are able to do the mega backdoor Roth.

For more on mega backdoor Roth, please read:

- Mega Backdoor Roth Without In-Service Distribution

- Mega Backdoor Roth Without a Big Paycheck

- Mega Backdoor Roth and Access To Your Money Before 59-1/2

- Mega Backdoor Roth In Solo 401k: Control Your Own Destiny

- Mega Backdoor Roth: Convert Within Plan or Out to Roth IRA?

Say No To Management Fees

If you are paying an advisor a percentage of your assets, you are paying 5-10x too much. Learn how to find an independent advisor, pay for advice, and only the advice.

Patrick Aw-Young says

Hi Harry,

Where should I put my non-Roth aftertax contribution before I take the balance out and roll it over to a Roth IRA? I usually do my rollover once a month. We’ve had a volatile stock market last year (with 10 months being down and only two months being up) and you’ve mentioned in your article that there’s no need to put our contribution in a money market fund.

Thanks,

Patrick

Harry Sit says

I just invest it as I normally would. Trying to prevent the value from going down only in that one month doesn’t help because it will still go up or down afterward.

RH says

Any chance you could update the helpful chart image in article with current 2024 limits? Great tool to visualize the buckets.

The IRS limits have fortunately become much more generous than when first published, looks like that is showing just ~$53k total (vs $69k allowed 2024) and sub-$20k pre-tax (vs $23,000 for 2024), thanks.

Joe says

Thanks for all the great info! I switched jobs and my new 401k allows after-tax contributions. I had also contributed to my previous 401k during the first few months of the year and I also received some company matching (the plan had no after-tax option). I understand that I can only contribute up to $23k combined across pre-tax or Roth in both of the 401k plans for the year, so I will adjust my new 401k contributions to take into account what I already contributed.

In terms of deciding how much to contribute to my new 401k plan after-tax option, does the $69k aggregate total allowed include any company contributions in my previous 401k as well? Or is the employer contributions that get factored into the $69k cap separate for each plan, even if the $23k pre-tax/Roth contribution limit get combined for plans? I was not sure how the old plan affects the contribution room for the pre-tax/Roth portion, the after-tax portion, and the employer contribution portion. Thanks!

Harry Sit says

The $69k total doesn’t include contributions made to your previous employer’s plan from either yourself or your former employer. Assuming these are your only two plans:

– Your pre-tax or Roth contribution to the new plan: $23k – your contribution to the previous plan

– Your current employer’s contribution: whatever the matching or profit sharing formula from the employer

– Your after-tax contribution: $69k minus the two contributions above