[Last updated on April 6, 2026 with all new screenshots from TurboTax Deluxe desktop software for the 2025 tax year and how the Form 8606 should look.]

You may have contributed to a Roth IRA and then realized later in the same year that you would exceed the income limit. You recharacterized the Roth IRA contribution as a Traditional IRA contribution and converted it to Roth again before the end of the year. Your IRA custodian sent you two 1099-R forms, one for the recharacterization and one for the conversion. This post shows you how to put them into TurboTax.

If you had done the recharacterizing and converting in the following year, you would have to split the tax reporting into two years by following Split-Year Backdoor Roth IRA in TurboTax, Year 1 and Split-Year Backdoor Roth IRA in TurboTax, Year 2. Now, because you caught the problem soon enough before the end of the year, you can handle all of it in the same year by following this guide.

Here’s the example scenario we’ll use in this guide:

You contributed $7,000 to a Roth IRA for 2025 in 2025. You realized that your income would be too high later in 2025. You recharacterized the Roth contribution for 2025 as a Traditional contribution. The IRA custodian moved $7,100 from your Roth IRA to your Traditional IRA because your original $7,000 contribution had some earnings. The value increased again to $7,200 when you converted it to Roth before December 31, 2025. You received two 1099-R forms, one for $7,100 and another for $7,200.

If you didn’t do any of these recharacterizing and converting, please follow our guide for a “clean” backdoor Roth in How To Report Backdoor Roth In TurboTax (Updated).

If you’re married and both you and your spouse did the same thing, you should follow the steps below once for yourself and once again for your spouse.

Use TurboTax Desktop Software

The screenshots below are from TurboTax Deluxe desktop software. The desktop software is both more powerful and less expensive than online software. If you haven’t paid for your TurboTax Online filing yet, you can buy TurboTax desktop software from Amazon, Costco, Walmart, etc., and switch from TurboTax Online to TurboTax desktop software (see instructions for how to make the switch from TurboTax).

1099-R for Recharacterization

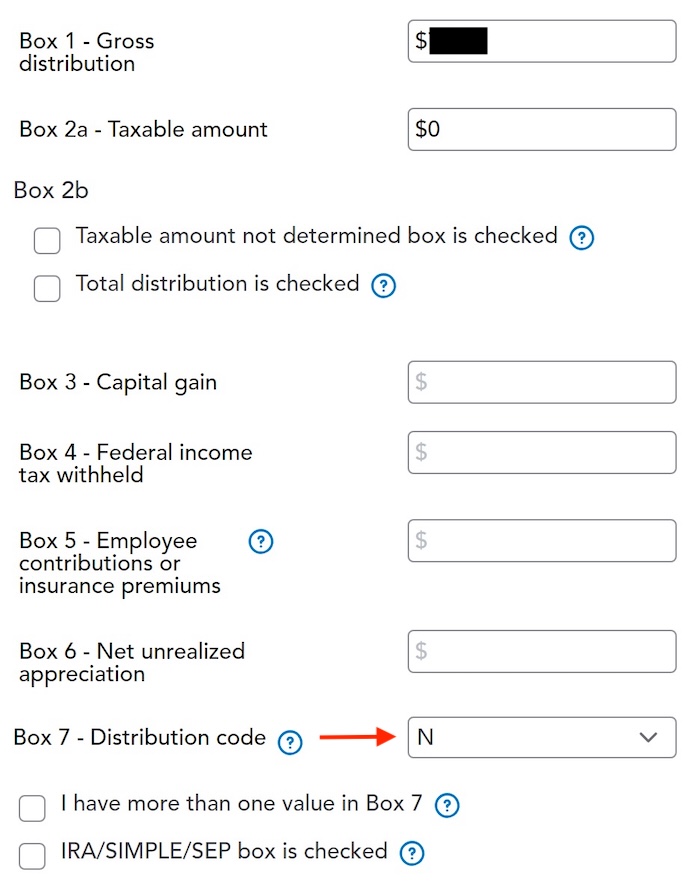

We handle the 1099-R form for the recharacterization first. This 1099-R form has a code “N” in Box 7.

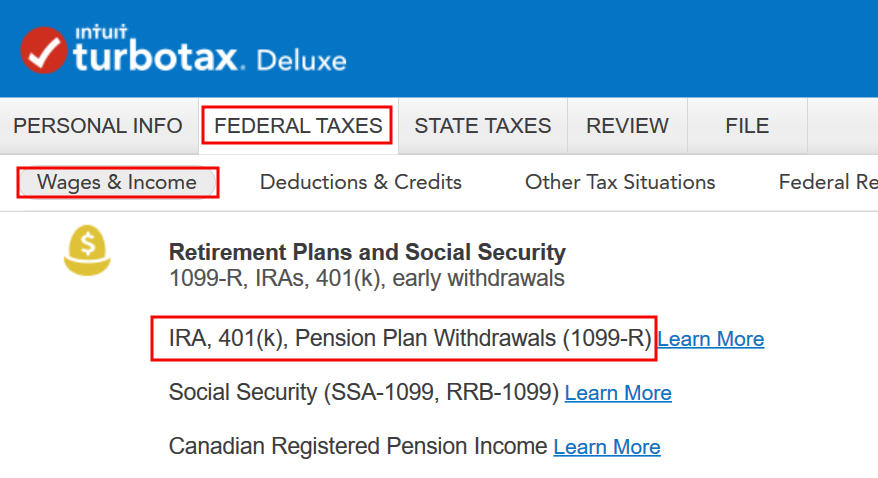

Go to Federal Taxes -> Wages & Income -> IRA, 401(k), Pension Plan Withdrawals (1099-R).

Confirm that you have received a 1099-R form. Import the 1099-R if you’d like. I’m skipping import and typing it myself.

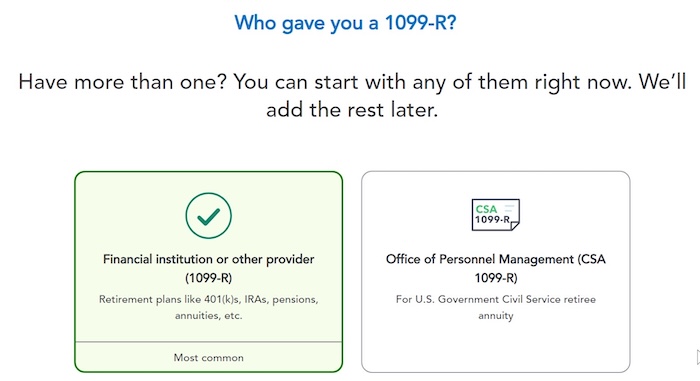

The 1099-R form came from a financial institution. Enter the payer information as it appears on your 1099-R.

The 1099-R form for the recharacterization shows the amount moved from the Roth IRA to the Traditional IRA in Box 1. It’s $7,100 in our example. The taxable amount is 0 in Box 2a, and the “Taxable amount not determined” box isn’t checked. The code in Box 7 is “N” and the “IRA/SEP/SIMPLE” box may or may not be checked. It isn’t checked in our sample form.

That box is blank in our 1099-R, and that’s OK.

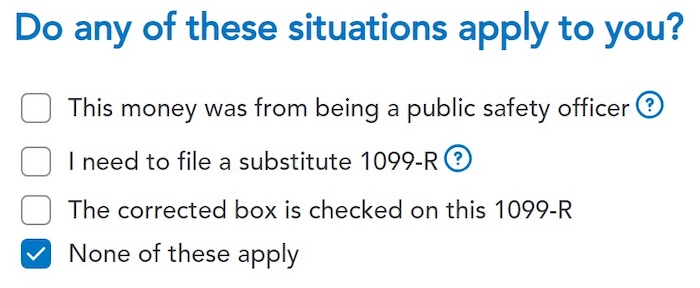

We don’t have any of these situations.

You’re done with the 1099-R form for the recharacterization. Click on “Add Another 1099-R” to add the one for the conversion if you don’t have both 1099-R forms imported already.

1099-R for Conversion

We enter the 1099-R form for the conversion now. This 1099-R form has a code “2” or “7” in Box 7.

This 1099-R form also came from a financial institution. Enter the payer information.

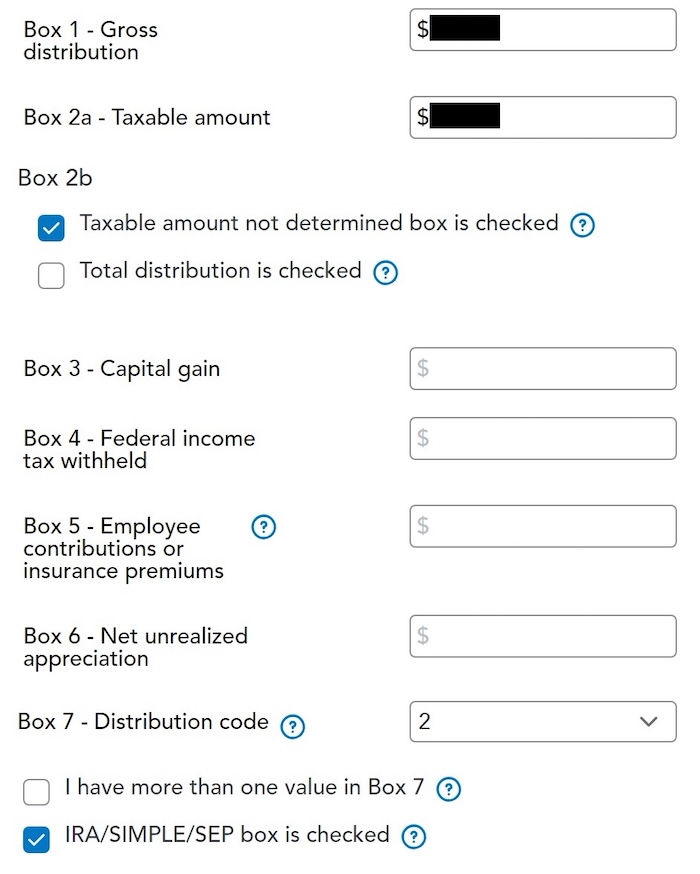

It’s normal to see the conversion reported in Box 2a as the taxable amount when Box 2b is checked to say “Taxable amount not determined.” The code in Box 7 is ‘2‘ when you’re under 59-1/2 or ‘7‘ when you’re over 59-1/2. The “IRA/SEP/SIMPLE” box is checked on this 1099-R form for the conversion.

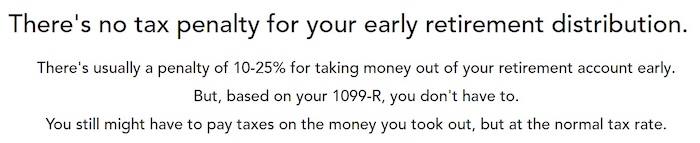

It says there’s no penalty, but your refund meter drops. Don’t panic. It’s normal and only temporary.

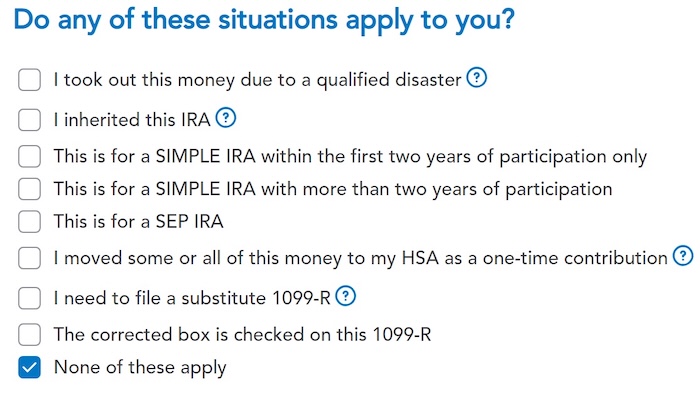

We don’t have any of these unusual situations.

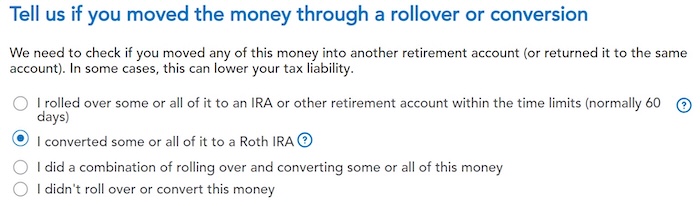

Converted to Roth

You converted to a Roth IRA. Don’t choose the “I rolled over …” option. A rollover means Traditional-to-Traditional. Converting to Roth isn’t a rollover.

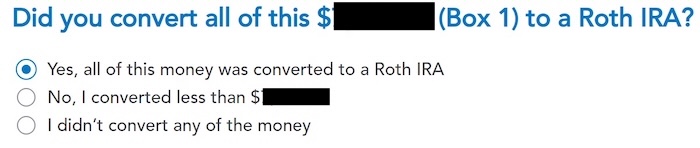

We converted all of it.

Now the 1099-R summary includes both 1099-R forms. Add more 1099-R forms if you have them. Continue by clicking on “Done.”

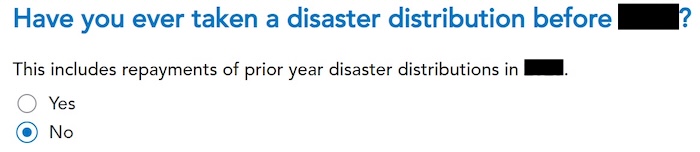

We didn’t take any disaster distributions.

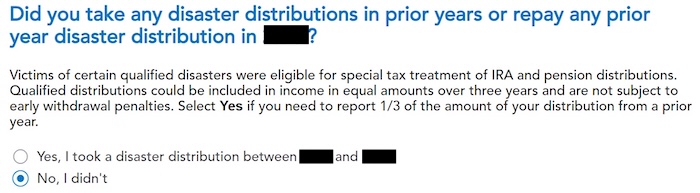

We already said no, but TurboTax wants to ask one more time.

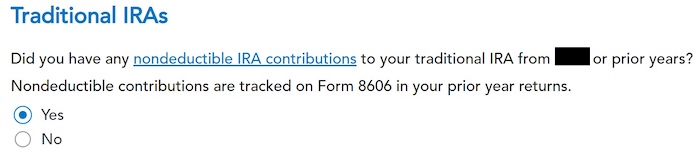

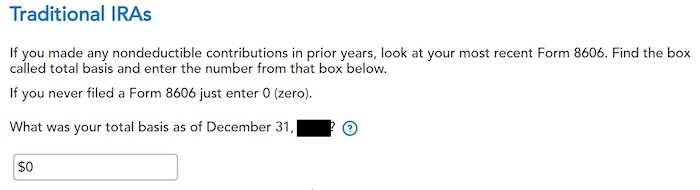

Basis

You can answer “No” here, but answering “Yes” with a 0 has the same effect, and it allows you to correct previous mistaken entries.

This should be 0 if you hadn’t made any nondeductible contribution to a Traditional IRA before. If you had, get the value from your last year’s Form 8606 Line 14.

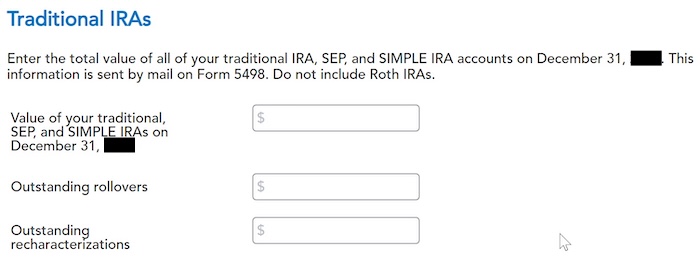

These are normally all zero if you converted everything. If you had a few dollars left in the account from earnings posted after you converted, enter the value from your year-end statement in the first box.

The refund meter is still temporarily depressed. It’ll come back only when we enter the recharacterized Roth IRA contribution.

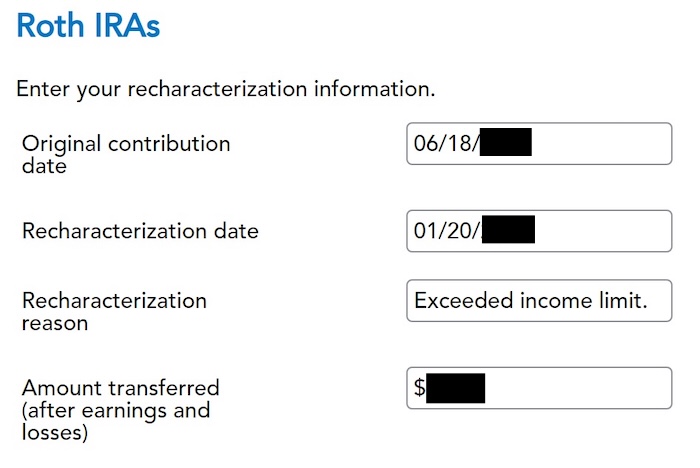

Recharacterized Contribution

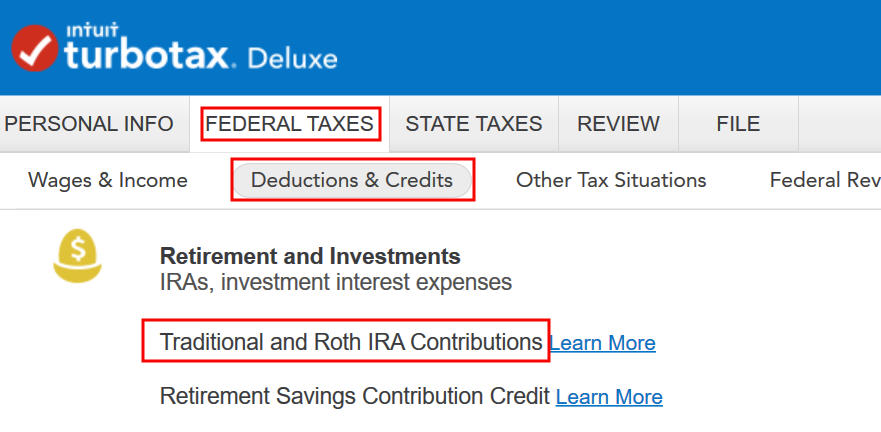

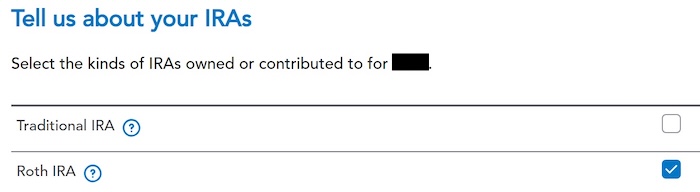

Go to Federal Taxes -> Deductions & Credits -> Traditional and Roth IRA Contributions.

Check the box for Roth IRA because you originally contributed to a Roth IRA.

We already checked the box for Roth IRA, but TurboTax just wants to make sure.

It was not a repayment of a retirement distribution.

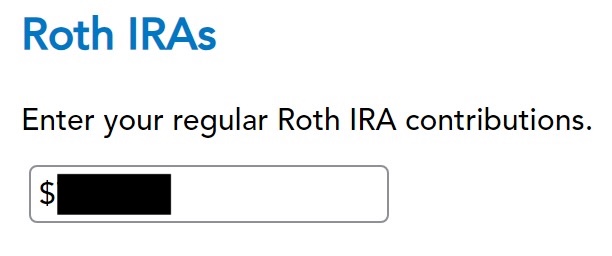

Enter the amount of your original Roth contribution. It was $7,000 in our example.

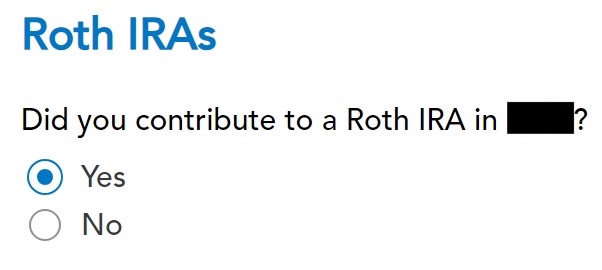

Recharacterized

Now we confess that we recharacterized the contribution as a Traditional IRA contribution. Answer Yes here.

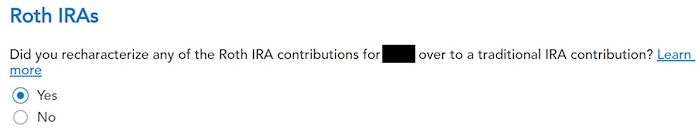

The amount here is relative to the original contribution amount. If you recharacterized the whole thing, enter $7,000 in our example, not $7,100, which was the amount with earnings that the IRA custodian moved into the Traditional IRA.

The IRS wants a statement to explain the recharacterization. Fill in the dates of your original contribution and your recharacterization. The amount in the last box includes earnings. It’s $7,100 in our example.

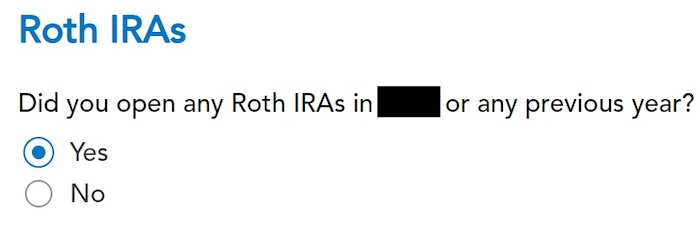

Roth Basis

Answer Yes or No, depending on your history.

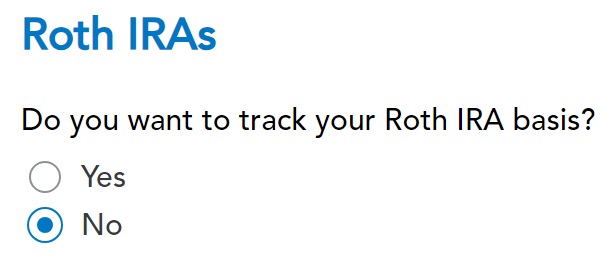

If you want TurboTax to track your Roth IRA basis, it’s going to ask you a series of questions about previous years, which is more trouble than it’s worth to me. I answered No. You don’t need to track your Roth IRA basis if you’re planning to withdraw from your Roth account only after age 59-1/2 and after you’ve had your first Roth IRA for five years. See Roth IRA Withdrawal After 59-1/2 in TurboTax.

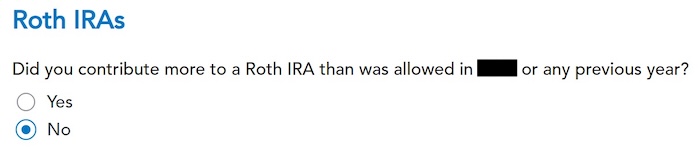

We don’t have any excess contributions.

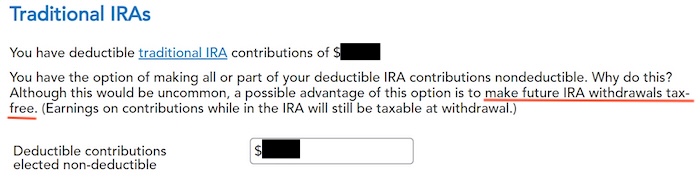

Make It Nondeductible

TurboTax shows this only when it sees that your income qualifies for a deduction. You have the option to take the deduction or decline it. Taking the deduction will make your conversion taxable, which is also OK because it creates a wash. It’s simpler if you make your full contribution nondeductible, then your Roth conversion isn’t taxable. Enter the amount TurboTax gives in the last box. It’s $7,000 in our example.

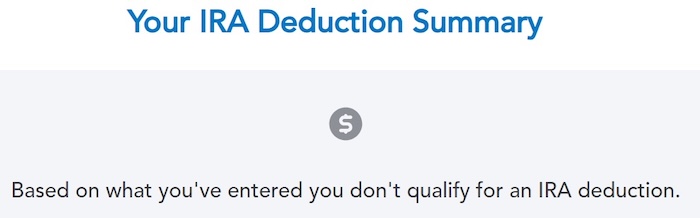

You don’t qualify for an IRA deduction, which is OK, because it makes your Roth conversion not taxable.

Taxable Income

Let’s look at how all these show up on your tax return. Click on “Forms” at the top right.

Find Form 1040 in the left navigation panel. Scroll up or down on the right to find lines 4a and 4b. Line 4a shows the sum of your two 1099-R forms. It’s $14,300 in our example. This is normal. Line 4b shows that only $200 is taxable. That’s the earnings between the time you contributed to your Traditional IRA and the time you converted it to a Roth IRA.

Form 8606

Here’s what your Form 8606 should look like. If yours looks different, it helps you pinpoint where the problem may be. If you’re married and both of you did a backdoor Roth, you’ll have two separate forms, labeled 8606-T and 8606-S.

Lines 6 through 12 may be blank if you had a zero balance in your Traditional, SEP, and SIMPLE IRAs as of December 31.

| Line 1 | The amount of the original contribution you recharacterized to a Traditional IRA, without earnings ($7,000 in our example) |

| Line 2 | The same amount from your last year’s Form 8606 Line 14 ($0 in our example) |

| Line 3 | The sum of Line 1 and Line 2 ($7,000 in our example) |

| Line 4 | blank |

| Line 5 | The same as Line 3 |

| Line 6 | The end-of-year balance of your Traditional, SEP, and SIMPLE IRAs (blank in our example) |

| Line 7 | 0 |

| Line 8 | The amount you converted to a Roth IRA ($7,200 in our example) |

| Line 9 | The sum of Lines 6-8 ($7,200 in our example) |

| Line 10 | Line 5 divided by Line 9 (0.97222 in our example) |

| Line 11 | Line 8 times Line 10 ($7,000 in our example) |

| Line 12 | 0 |

| Line 13 | Same as Line 11 ($7,000 in our example) |

| Line 14 | Line 3 minus Line 13 ($0 in our example) |

| Line 15 | Zero or blank |

| Line 16 | The amount you converted to a Roth IRA ($7,200 in our example) |

| Line 17 | The same as Line 13 ($7,000 in our example) |

| Line 18 | Line 16 minus Line 17 ($200 in our example) |

When you’re done examining the form, click on Step-by-Step on the top right to go back to the interview.

Switch to Clean Backdoor Roth

You avoided having to split your IRA contribution and Roth conversion into two different tax returns by recharacterizing in the same year and converting before December 31. Still, you had to do the extra work with your IRA custodian and follow all these steps in this guide when you do your taxes.

It’s much better to go with a “clean” backdoor Roth from the get-go. If there’s any possibility that your income will exceed the limit again, simply contribute to a Traditional IRA for 2026 in 2026 and convert it to Roth in 2026. You’re allowed to do a clean backdoor Roth even if your income ends up below the income limit for a direct contribution to a Roth IRA. It’s much simpler than the confusing recharacterize-and-convert maneuver. Then you only need to follow our guide for a clean backdoor Roth in How To Report Backdoor Roth In TurboTax.

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

Jay says

Thank you Harry for compiling this guide together. We had some additional questions while doing our taxes this year, and these step-by-step instructions were extremely informative and clear, and make the filing process smooth and simple. We very much appreciate your assistance and advice.

Di says

Hello,

Thank you so much for your guidance.

After following the step-by-step instructions, I review form 8606 and wonder why line 8 (Enter the net amount you converted from traditional, traditional SEP, and traditional SIMPLE IRAs to Roth, Roth SEP, or Roth SIMPLE IRAs in 2023. Also, enter this amount on line 16) shows nothing. It does show in Part II, line 16. Should the Roth IRA conversion amount of 6700 (using your example) also be reported on line 8?

Please advise.

Harry Sit says

The IRS allows shortcuts in certain cases. The software knows when to take one. Let the software do its thing.

Di says

Hi Harry,

I have another question.

Following the steps in Recharacterization Contribution – Go to Federal Taxes -> Deductions & Credits -> Traditional and Roth IRA Contributions, I only checked box Roth IRA. However, after finishing all steps until the end as guidance, I went back to review and saw both boxes Traditional IRA and Roth IRA checked even though I did not check box Traditional IRA at all. Is it correct?

Please advise.

Thanks.

Harry Sit says

If that’s the only thing, don’t worry about it. The critical part to check is Form 1040 Lines 4a and 4b as you see at the end of this post.

Austin says

Hi Harry,

Thanks for the helpful write-ups. I am in Year 1 of the Split-Year Backdoor Roth IRA process. While recharacterizing my 2024 contributions (Roth to Trad), I also recharacterized $2K of 2025 contributions that I had already done. I contributed the remaining $5K directly to Trad, then converted everything (2024 & 2025) back to Roth.

Thinking ahead to next year, will I need to follow this guide (Recharacterize & Convert, Same Year) for the $2K and then the “clean backdoor” steps for the other $5K (resulting in extra 1099-R entries)? Or would everything be picked up by the Year 2 Split-Year Backdoor Roth IRA guide? Thanks again for putting all of this together!

Austin

Harry Sit says

You’ll have a mixture next year:

– “Year 2” with regard to your 2024 contributions recharacterized and converted in 2025, which also covers the clean backdoor Roth on top for your $5k contributions for 2025.

– “Recharacterize & Convert, Same Year” with regard to the recharacterized $2k contributions for 2025.

The conversion part is the same between these two guides. You only do it once by following the Year 2 guide.

Kora says

Hi Harry,

Thank you for doing taking the time to post this information.

I do have a question.

I chose to import my 1099-R and Box 2a shows the same amount as in Box 1. Looking at your example, Box2a is 0. Am I supposed to change my amount to 0 on my imported form?

Harry Sit says

There are two 1099-R forms. The one for the recharacterization (code N in Box 7) has 0 in Box 2a. The one for the conversion (code 2 or 7 in Box 7) has the same amount in Box 2a as in Box 1. The import may have put the second form first. If you’re looking at the second 1099-R, click on “Back” and open the other one.