Last updated on April 7, 2026 with all new screenshots from TurboTax Deluxe desktop software for the 2025 tax year and how Form 8606 should look. If you use other tax software, see:

If you did a Backdoor Roth, which involves making a non-deductible contribution to a Traditional IRA and then converting from the Traditional IRA to a Roth IRA, you must report both the contribution and the conversion in the tax software. This post gives you a step-by-step walkthrough of how to do it in TurboTax. For more information on Backdoor Roth in general, see Backdoor Roth: A Complete How-To.

What To Report

You report on the tax return your contribution to a Traditional IRA *for* that year, and you also report your conversion to Roth *during* that year.

For example, when you are doing your tax return for 2025, you report the contribution you made *for* 2025, whether you actually did it during 2025 or between January 1 and April 15, 2026. You also report your conversion to Roth *during* 2025, whether the contribution was made for 2025, 2024, or any previous years.

Therefore, a contribution made during 2026 for the year 2025 goes on the tax return for 2025. A conversion done during 2026 after you contributed for 2025 goes on the tax return for 2026.

You do yourself a big favor and avoid a lot of confusion by making your contribution for the current year and finishing your conversion in the same year. I call this a “planned” Backdoor Roth or a “clean” Backdoor Roth — you’re doing it deliberately. Don’t wait until the following year to contribute for the previous year. Contribute for 2025 in 2025 and convert it during 2025. Contribute for 2026 in 2026 and convert it during 2026. Everything is clean and neat this way.

If you are already off by one year, it depends on whether you’re handling the contribution part or the conversion part right now. If you contributed to a Traditional IRA for 2025 in 2026 and converted in 2026, or if you recharacterized a 2025 Roth contribution in 2026 and converted in 2026, please follow Split-Year Backdoor Roth IRA in TurboTax, Year 1. If you contributed to a Traditional IRA for 2024 in 2025 and converted in 2025, or if you recharacterized a 2024 Roth contribution in 2025 and converted in 2025, please follow Split-Year Backdoor Roth IRA in TurboTax, Year 2. If you recharacterized your 2025 Roth contribution in 2025 and converted in 2025, please follow Backdoor Roth in TurboTax: Recharacterize & Convert, Same Year.

Use TurboTax Desktop Software

The screenshots below are from TurboTax Deluxe desktop software. The desktop software is both more powerful and less expensive than online software. If you haven’t paid for your TurboTax Online filing yet, you can buy TurboTax desktop software from Amazon, Costco, Walmart, etc., and switch from TurboTax Online to TurboTax desktop software (see instructions for how to make the switch from TurboTax).

Here’s the planned “clean” Backdoor Roth scenario we will use as an example:

You contributed $7,000 to a traditional IRA for 2025 in 2025. Your income is too high to claim a deduction for the contribution. By the time you converted it to Roth IRA, also in 2025, the value grew to $7,200. You have no other traditional, SEP, or SIMPLE IRA after you converted your traditional IRA to Roth. You did not roll over any pre-tax money from a retirement plan to a traditional IRA after you completed the conversion.

If your scenario is different, you will have to make some adjustments to the screens shown here.

Before we start, suppose this is what TurboTax shows:

We will compare the results after we enter the Backdoor Roth.

Convert Traditional IRA to Roth

The tax software works on income items first. Even though the conversion happened after the contribution, we enter the conversion first.

When you convert from a Traditional IRA to a Roth IRA, you will receive a 1099-R form. Complete this section only if you converted *during* 2025. If you only converted during 2026, you won’t have a 1099-R until next January. Please follow Split-Year Backdoor Roth IRA in TurboTax, Year 1. If your conversion during 2025 was against a contribution you made for 2024 or a 2024 contribution you recharacterized in 2025, please follow Split-Year Backdoor Roth IRA in TurboTax, Year 2.

In our example, we assume that by the time you converted, the money in the Traditional IRA had grown from $7,000 to $7,200.

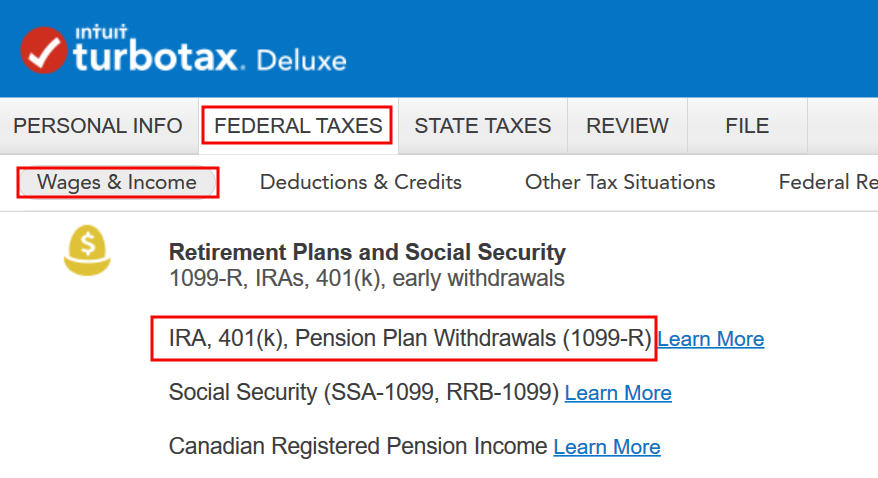

Enter 1099-R

Go to Federal Taxes -> Wages & Income -> IRA, 401(k), Pension Plan Withdrawals (1099-R).

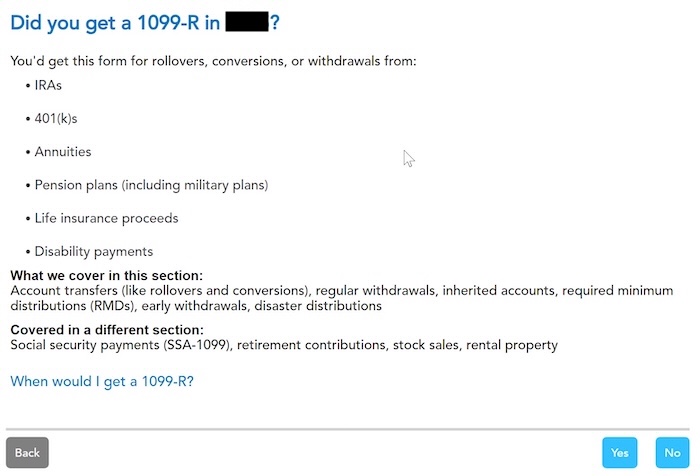

As you work through the interview, you will eventually come to the point of entering the 1099-R. Select Yes, you got a 1099-R. Import the 1099-R if you’d like. I’m choosing to skip import and type it myself.

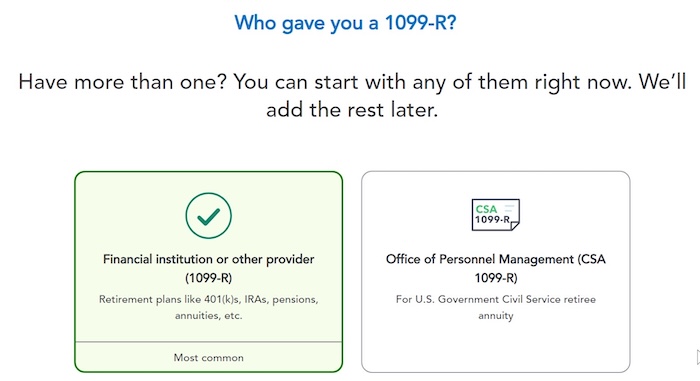

You got it from a financial institution. Enter the payer information as shown on your 1099-R.

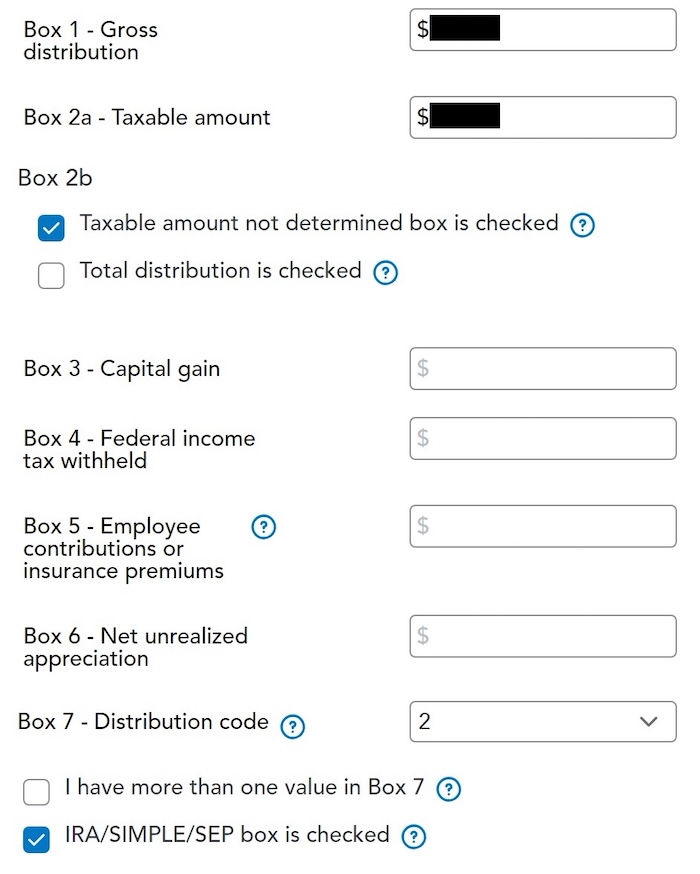

Box 1 shows the amount converted to the Roth IRA. It’s $7,200 in our example. It’s normal to have the same amount as the taxable amount in Box 2a when Box 2b is checked saying “taxable amount not determined.” The total distribution box may or may not be checked. It doesn’t matter.

Pay attention to the code in Box 7 and the IRA/SEP/SIMPLE box. Make sure your entry matches your 1099-R exactly. The code in Box 7 should be 2 if you’re under 59-1/2 and 7 if you’re over 59-1/2. The IRA/SIMPLE/SEP box should be checked.

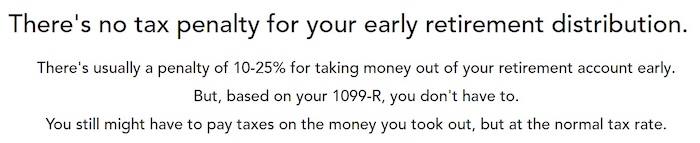

You get this Good News, but …

Your refund in progress drops a lot. We went from $2,384 down to $858. Don’t panic. It’s normal and temporary.

None of these should apply in a usual backdoor Roth.

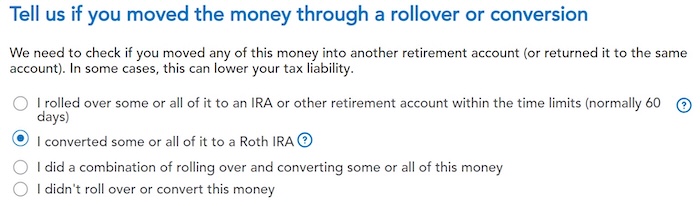

Converted to Roth

Choose “I converted some or all of it to a Roth IRA.” Don’t choose the “I rolled over …” option. A Roth conversion is not a rollover.

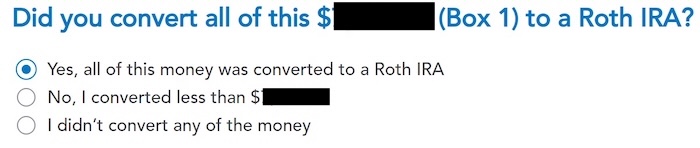

Yes, you converted all of it.

You get a summary of your 1099-Rs next. Repeat the previous steps to add another if you have more than one. If you’re married and both of you did a Backdoor Roth, enter the 1099-R for both of you, but pay attention to select whose 1099-R it is. Don’t accidentally assign two 1099-R forms to the same person.

Basis

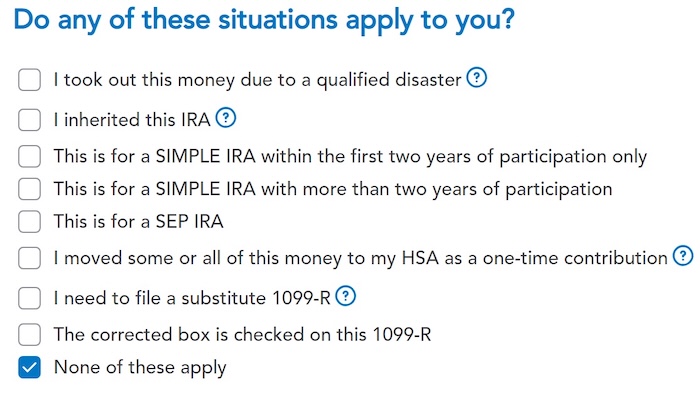

We didn’t take or repay any disaster distribution.

We already said no, but TurboTax just wants to be sure.

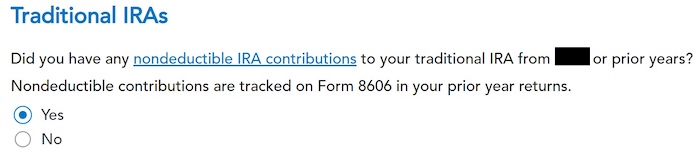

Here it’s asking about the carryover from the prior year. When you did a clean “planned” Backdoor Roth as in our example — contributed for 2025 in 2025 and converted before the end of 2025 — you can answer No here, but answering Yes with a 0 has the same effect as answering No, and it allows you to correct errors.

If you answered Yes to the previous question and you did your previous year’s return correctly also in TurboTax, your basis from the previous year will show up here. If you did your previous year’s tax return wrong, fix your previous return first.

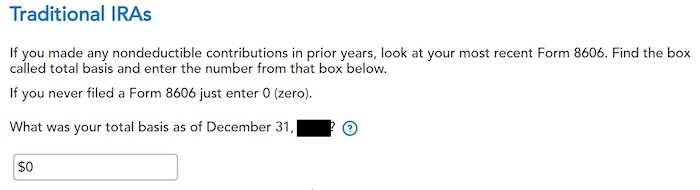

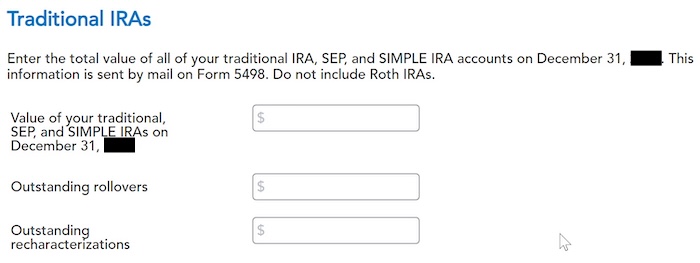

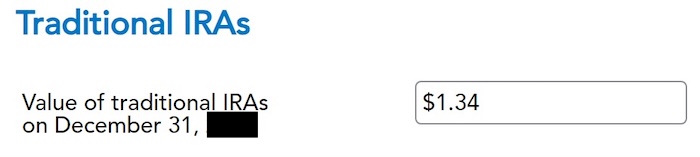

Enter the values of ALL your Traditional, SEP, and SIMPLE IRAs at the end of the year. We entered all zeros because we don’t have anything in traditional, SEP, or SIMPLE IRAs after we converted it all. If your account posted earnings after you converted and you left the earnings in the account, get the value from your year-end statement and put it in the first box.

That’s it so far on the income side. Continue with other income items. The refund in progress is still temporarily depressed. Don’t worry. It will change.

Non-Deductible Contribution to Traditional IRA

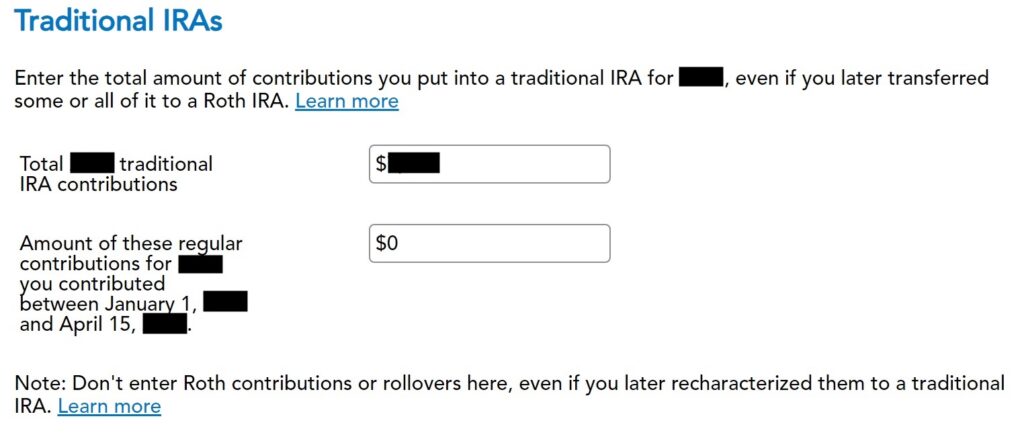

Now we enter the non-deductible contribution to a Traditional IRA *for* 2025.

If you contributed for 2025 between January 1 and April 15, 2026, or if you recharacterized a 2025 contribution in 2026, please follow Backdoor Roth in TurboTax: Recharacterize and Convert, Year 1. If your contribution during 2025 was for 2024, make sure you entered it on the 2024 tax return. If not, fix your 2024 return first by following the steps in Backdoor Roth in TurboTax: Recharacterize and Convert, Year 1.

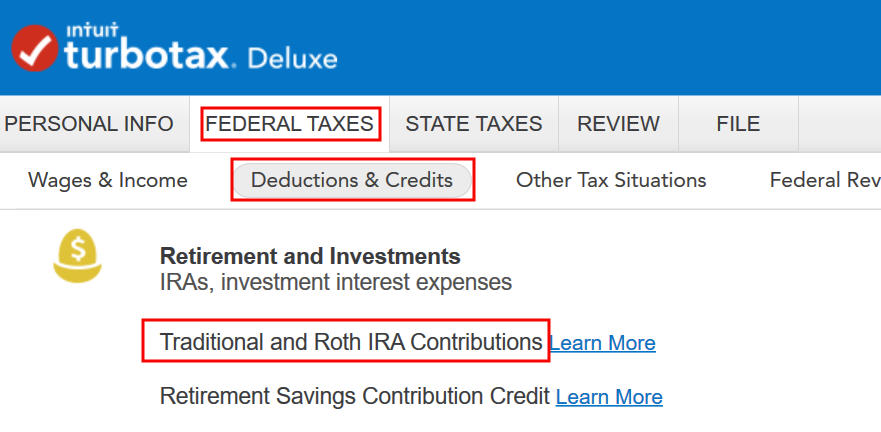

Go to Federal Taxes -> Deductions & Credits -> Traditional and Roth IRA Contributions.

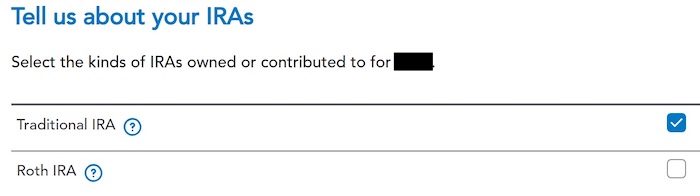

We check the box for Traditional IRA because we did a clean “planned” Backdoor Roth.

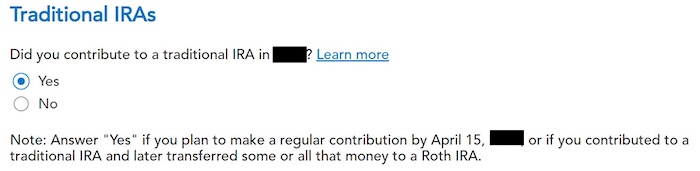

We already checked the box for Traditional but TurboTax just wants to make sure. Answer Yes here.

It was not a repayment of a retirement distribution.

Enter the contribution amount. It’s $7,000 in our example. Because we contributed for year 2025 in 2025, we put zero in the second box. If you contributed for 2025 between January 1 and April 15, 2026, include the contribution in both boxes.

Right away, our federal refund in progress goes back up! We started with $2,384. It went down to $858. Now it comes back to $2,335. The $49 difference is because we have to pay tax on the $200 in earnings when we contributed $7,000 and converted $7,200. If you had less in earnings, your refund numbers would be closer still.

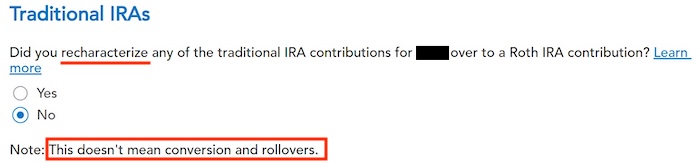

Converted, Did Not Recharacterize

This is a critical question. Answer “No.” You converted the money, not recharacterized.

You may not get this question if you already entered your W-2 and it has Box 13 for the retirement coverage checked. Answer yes if you’re covered by a retirement plan, but the box on your W-2 wasn’t checked.

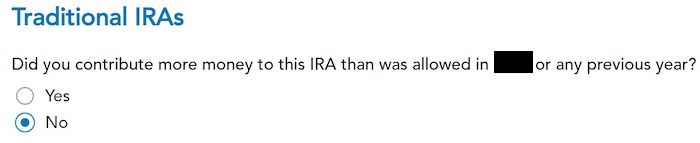

We didn’t make excess contributions.

Basis

TurboTax asks the same question it did before. For a clean “planned” Backdoor Roth, we can answer No, but answering Yes with a 0 has the same effect, and it allows you to correct errors.

If you did your taxes correctly on TurboTax last year, TurboTax transfers the number here. If you made non-deductible contributions for previous years (regardless of when), enter the number on line 14 of your Form 8606 from last year.

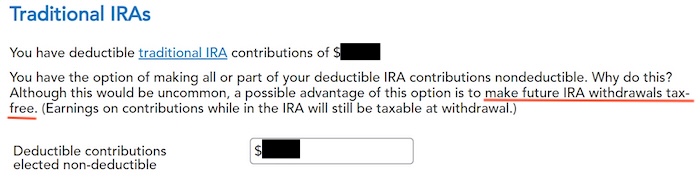

Make It Nondeductible

TurboTax shows this screen if it sees that you qualify for a deduction for the Traditional IRA contribution. If you take the deduction, it’ll make your Roth conversion taxable, which creates a wash. It’s simpler if you make your full IRA contribution nondeductible, and then your Roth conversion won’t be taxable. Enter the amount that TurboTax says is deductible.

Because we did a clean “planned” Backdoor Roth, we don’t have anything left after we converted everything before the end of the same year. If you have a small balance left because of interest posted after you converted, enter the value from your year-end statement here.

This is expected. That’s why we did the Backdoor Roth.

Taxable Income from Backdoor Roth

After going through all these, would you like to see how you are taxed on the Backdoor Roth?

Click on Forms on the top right.

Find Form 1040 in the left navigation panel. Scroll up or down on the right to find lines 4a and 4b. They show a $7,200 distribution from the IRA, and only $200 of the $7,200 is taxable in our example. That’s the earnings between the time you contributed to your Traditional IRA and the time you converted it to Roth.

Tah-Dah! You put money into a Roth IRA through the back door when you aren’t eligible to contribute to it directly. That’s why it’s called a Backdoor Roth. You pay tax on a small amount of earnings between the contribution and the conversion. That’s negligible relative to the benefit of having tax-free growth on your contribution for many years.

Form 8606

Here’s what your Form 8606 should look like. If yours looks different, it helps you pinpoint where the problem may be. If you’re married and both of you did a backdoor Roth, you’ll have two separate forms, labeled 8606-T and 8606-S.

Lines 6 through 12 are interim steps. The software decides how to fill them. It’s normal to see blanks in those lines.

| Line 1 | The amount you contributed to a Traditional IRA ($7,000 in our example) |

| Line 2 | The same amount from your last year’s Form 8606 Line 14 ($0 in our example) |

| Line 3 | The sum of Line 1 and Line 2 |

| Line 4 | blank |

| Line 5 | The same as Line 3 |

| Lines 6 through 12 | blank |

| Line 13 | Calculated by software ($7,000 in our example) |

| Line 14 | Line 3 minus Line 13 ($0 in our example) |

| Line 15 a-c | Zero or blank |

| Line 16 | The amount on your 1099-R Line 1 ($7,200 in our example) |

| Line 17 | The same as Line 13 ($7,000 in our example) |

| Line 18 | Line 16 minus Line 17 ($200 in our example) |

When you’re done examining the form, click on Step-by-Step on the top right to go back to the interview.

State Taxes

Many states use the federal AGI as a starting point. When the backdoor Roth isn’t included in the federal AGI, it’s automatically not taxed by the state.

Some states, for instance, Massachusetts and New Jersey, want to ask you whether the money had already been taxed by the state when it was originally contributed to the Traditional IRA. Your state tax refund will be lower until you go into the state portion of the software and answer yes to that question.

You’ll need to find that question in the state part if your state requires it. It’s different in each state. I don’t have screenshots for where the question is because I don’t have the state program for every state.

Troubleshooting

If you followed the steps and you are not getting the expected results, here are a few things to check.

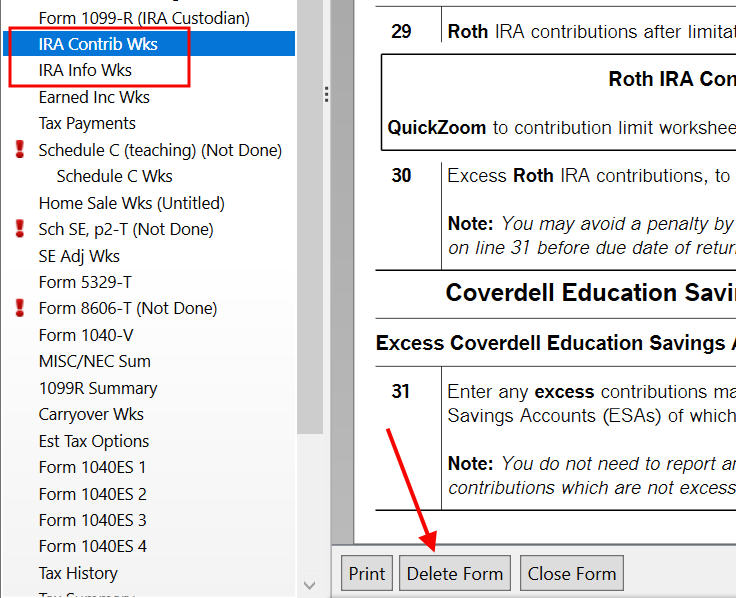

Fresh Start

It’s best to follow the steps fresh in one pass. If you already went back and forth with different answers before you found this guide, some of your previous answers may be stuck somewhere you no longer see. You can delete them and start over.

Click on Forms on the top right.

Find “IRA Contrib Wks” and “IRA Info Wks” in the left navigation pane and click on “Delete Form” to delete them. Then you can start over by following the steps above.

Conversion Is Taxed

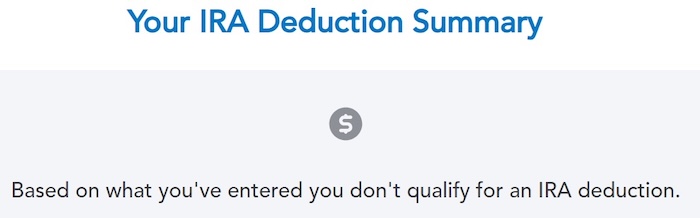

If you don’t have a retirement plan at work, you have a higher income limit to take a deduction on your Traditional IRA contribution. Taking this deduction also makes your Roth IRA conversion taxable. You can see this deduction on Schedule 1 Line 20, which reduces your AGI.

The taxable Roth IRA conversion and the deduction for your Traditional IRA contribution offset each other to create a wash. This is normal, and it doesn’t cause any problems when you indeed don’t have a retirement plan at work.

It’s less confusing if you decline the tax deduction, which also makes your conversion non-taxable. See the Make It Nondeductible section.

Self vs Spouse

If you are married, make sure you don’t have the 1099-R and IRA contribution mixed up between yourself and your spouse. If you inadvertently entered two 1099-Rs issued to you instead of one for you and one for your spouse, the second 1099-R to you will not match up with a Traditional IRA contribution made by your spouse. If you entered a 1099-R for both yourself and your spouse, but you only entered one Traditional IRA contribution, you will be taxed on one 1099-R.

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

Thomas says

Thank You, this is a great step by step guide for clean BD roth in TT. I had to do a clean start as you suggested to get it right. Another note is that on my state return it still listed it as taxable income (2025) as I normally just accept what TT has on the line while doing the State return. All I had to do was to tell TT that it was not state taxable (Alabama) by editing the Retirement entry and all was good. I went back and looked at last years (2024) return and I payed state tax on my $8K BD roth (not great) but not sure if it is worth doing an amended State return (same issue my Federal return was $0 tax but TT left it taxable for Alabama and I did not catch it)

Thomas

Grace says

How exactly did you fix the state ? I have the same issue with my NJ tax return. Please advise.

Thank you

allan says

thanks this is super helpful. in the article you mentioned that you contributed $7,000 and converted $7,200. where in turbotax/form will you enter that 7200/or 200 earnings? thanks

Harry Sit says

The $7,200 is in Box 1 of the 1099-R form. You enter it or import it into the software.

Thomas says

When it got to that part of the return in the state. I went into that form and changed the answer taxable to No.

Bill says

Awesome guide! I’ve referenced it over the years and I’m so glad you’ve updated it to keep up with the software changes. I couldn’t have done it without this. Thank you, thank you, thank you.

D says

Amazing guide. Every year you save my bacon.

Ella says

Hi, thank you so much for this post, Super helpful. But for my case, I contributed 7000 in 2025 for 2024 (filled in Form 8606 in 2024 tax return), also to your point, to have a clean back up, I contributed 7000 in 2025 for 2025 too. It turns out my 1099-R, box 1 is 14000. How to report this in Turbotax then? I put $7000 in the box of “Total 2025 contribution”. Turbotax still shows 7000 will be taxable this year. how to fix it?

Harry Sit says

Please follow Split-Year Backdoor Roth IRA in TurboTax, Year 2, all the way through the section “Clean Backdoor Roth On Top.” 2024 is Year 1. 2025 is Year 2.

EOG says

Hi – my annual visit to refer to this like others it seems. Thanks again for the resource.

re: “The refund in progress is still temporarily depressed”

In my version of TurboTax (2025 Deluxe, desktop), the refund in progress did not drop and rebound through this process like it has in other years. Though this was after I went into the section having already imported the 1099-R earlier when I batch imported all brokerage documents. So I went into the section to review it (as required by TurboTax), and the values were there but it did not know yet I had converted it to a Roth. Anyhow, just wanted to report that the refund amount may or may NOT change through the process, if you imported the 1099-R. 🙂

Liz says

Dear Harry,

Thanks a lot for the article. This is very helpful. I have a question about clean backdoor for the same year. After all the steps above, do you get a Form 8606? Same question for the article “Backdoor Roth in TurboTax: Recharacterize & Convert, Same Year”. Thank you.

Harry Sit says

Yes, you get a Form 8606, which feeds into your 1040 line 4b.

Liz says

Thank you Harry. is the form 8606 exact same for same year clean backdoor and same year recharacterization? i.e.,

1. Part I line 1, 3, 14 will be filled with original contribution.

2. Part II line 16 will be filled with amount in 1099-R coded 2. line 17 = line 3. Line 18 = line 16 – line 17.

Also, for same year clean backdoor and same year recharacterization, Form 8606 only reflects that year and nothing carryover to next year, right? Thanks again.

Harry Sit says

I added a new section in the two posts for how the Form 8606 should look. They’re not exactly the same in the middle part of the form but the bottom line is the same.

If you don’t have any balance left in your Traditional, SEP, or SIMPLE IRAs as of December 31, you have no carryover to the next year. If you had a small amount of earnings posted after the conversion and you left it in the Traditional IRA, you may have a small carryover. The software calculates the carryover and auto-populates for next year. Having a small carryover isn’t a big deal.

Livia says

Thanks for this very helpful guide.

I followed all the steps as described but for me, lines 6-8 are blank.

I had $0 in my traditional IRA after moving the money into my Roth account and did the backdoor complete all at once in 2025 for 2025.

Thanks so much for any assistance/insight you can provide.

Harry Sit says

It’s normal to see blank lines 6 through 12.

Livia says

Thank you for your prompt help and for providing this really helpful resource!

SM says

Thank you for the guide.

Did the TurboTax and backdoor last year

This year it did not ask me the make it non deductible question. Also it is asking me about prior year Roth accounts . I did not contribute other than to convert my traditional to Roth IRA. I also said no to track basis etc. it looks like it is deducting the IRA contribution. How to proceed. Should I just uncheck the Roth IRA accounts in the accounts section ? Should I say opened but did not contribute ( I only converted from my traditional) . Thank you

Harry Sit says

Follow the Troubleshooting section. Delete the two worksheets and start over if necessary. If it didn’t ask you the make it non-deductible question, it means your income is over the limit to have a choice. Then your contribution automatically isn’t deductible. If you missed that question and it’s deducting the contribution, that works too when it makes the conversion. Either way works:

A) Conversion is taxable on 1040 line 4b, and you have a deduction of a similar amount on Schedule 1 line 17. Or

B) Conversion isn’t taxable on 1040 line 4b, and you don’t have a deduction of a similar amount on Schedule 1 line 17.

Norma Castillo says

The quality team recommended this article and it was a difference in what to look for in the Turbo Tax Online.

I was able to only add the Section II for the Roth Conversion from Traditional after going into the Form View and checking the box All Was Converted to Roth and it populated the coversion amount of the $7000 for each back door roth conversion. Turbo Tax Online and software may opt to add the data input software script to be able to do this in regular input than in the Form View . It would help agents especially and customer’s if each section was outlined a bit more user friendly. This article helped save a tax return.