After reading my article last week CD vs Bond Fund: A Case Study, reader TJ asked:

“Why does anyone hold bonds EVER, if CD’s always win?”

First, like many things in life, it’s not all-or-nothing: all bonds no CDs or all CDs no bonds. Even if CDs are strictly better than bonds, there are still reasons to hold bonds instead of CDs.

CDs are typically not available in 401k or 403b plans. If we have another stock market crash, it’s easier to sell bonds to buy stocks for rebalancing. But as I wrote in the previous article which debunked a few myths about CDs, you don’t need 100% of your fixed-income money for rebalancing. Usually you only need 1/4 to 1/3 of it. The bulk of your fixed-income money can go into CDs.

For people in a high tax bracket investing in taxable accounts, muni bonds are still a better deal than CDs.

For the moment, let’s assume it’s in an IRA and the only choices we are considering are the Vanguard Total Bond Market Index Fund and CDs. In the article last week I showed a 7-year CD bought 4 years ago is projected to be a better deal when it matures in 3 years. Similarly, a 7-year CD bought now is also projected to be a better deal in the next 7 years.

Why don’t investors realize that CDs are a better deal and move from bonds to CDs? I have a few theories, none of which I can prove definitively. They probably all have a kernel of truth. I’m offering these up as possible answers to TJ’s question.

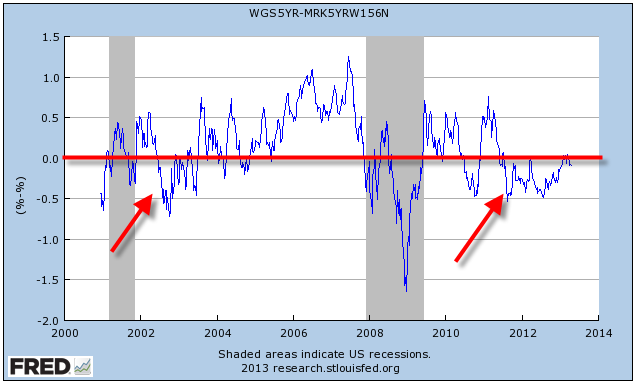

Bonds Used to Be Better

Long-term data for CDs are hard to come by. St. Louis Fed has data for 5-year CDs from Bankrate.com since December 2000. The following chart shows the yield of 5-year Treasury minus the yield of 5-year CDs since December 2000. Positive numbers above the red line indicate Treasury yields were higher than CD yields.

Except during the financial crisis when Treasury yields were very low due to flight to quality, 5-year Treasury yield were in general higher than 5-year CD yield by about 0.5%. However, I should note this hasn’t been the case since 2011.

Considering that agency and corporate bonds in a total bond market index fund usually have a higher yield than Treasury, it’s fair to say that the bond fund had a higher yield than CDs most of the time in the past. People remembered that but didn’t notice that time changed. CDs have better yield now.

Bonds Are Better Than Average CDs

The data for CDs in the chart above are for average CDs. If you just walk into a random bank, you are not going to get a rate as good as bond yields. I see Wells Fargo offers a 58-month CD paying 0.5%, a far cry from a 5-year CD from CIT Bank paying 1.75%, a 7-year CD from Discover Bank paying 1.9%, or even higher at some credit unions.

The Internet has made it much easier to find the best CD rates. It could be that the best CDs have always been better than bonds but people just didn’t know where to find them.

Mentally Associate CDs With Short-Term Savings

Bonds are a product of Wall Street. They are traded in the capital market. Bond funds buy, hold, and sell bonds. They are associated with investing. CDs are a retail product. They are associated with short-term savings. People don’t think about CDs when they are investing.

Institutional investors can’t deal with CDs. When they are talking about investing in fixed income, bonds are pretty much the only game. When they mention cash, they mean money market funds, not bank savings accounts or CDs.

In this otherwise excellent web cast from Vanguard, Ken Volpert, head of the Vanguard Fixed Income Group, made no mention of CDs as an alternative to bond funds, as if bank savings accounts and CDs don’t exist.

“And for investors who are sitting in cash, they’re basically earning zero. At least the bond market has given you a couple of percent returns. So if it takes a few years before we get back to normal, you could be losing a few percent a year relative by sitting in cash.”

Sitting in cash is not basically earning zero. If cash means bank savings account, you can get 1% or above 1% at some places. If cash means bank CDs, you can get the same “a few percent a year” or higher.

Want More Liquidity Than Necessary

Even when a bond fund is for long-term investing, in an IRA for that matter, it’s fully liquid. You can sell all of it on a whim even though people know they are not supposed to do so and they won’t do so in reality. But they still like to feel they are in control. CDs on the other hand make people feel that the money is locked up, out of their control. If you want to sell you will have to pay an early withdrawal penalty. Nobody wants to hear the word “penalty” as if they did something wrong.

The desire for utmost liquidity for 100% of the money 100% of the time is irrational. When you invest for the long term, the money is already committed. You don’t need to have it all liquid at all times. Getting paid for illiquidity is one advantage small investors have over institutional investors.

Overvalue Simplicity

Having a bond fund together with stock funds all in one account is simple. Investing in CDs would require another account.

So? What’s the matter if I have to create another entry in my Microsoft Money software? I’d rather have a few thousand dollars more in my account than make my software neat.

Unfamiliar With The Ease of Buying

Inertia is a strong force. Even if evidence suggests CDs are better, people like to find excuses saying it would be too much trouble to make the switch. If they never had CDs in an IRA before, they may erroneously think it’s not possible or there is a lot of paperwork to do the transfer. Because people haven’t done it before, they are afraid they would do something wrong. They’d rather stick to the familiar than venture out for something better.

In fact it’s very easy to buy CDs with money in an IRA at a different institution. You just fill out a form given to you by the bank or credit union. They will get the money transferred over. See the IRA transfer form from Discover Bank as an example. You do it once and you are good for 5 or 7 years. Money is not going to disappear mid-air during the transfer.

***

There you have it. Those are the reasons I can think of why people still invest in bonds, not CDs. For people who really understand what’s going on, there’s little reason not to use CDs for the bulk of fixed-income investments (except munis in taxable accounts). Even for TIPS for inflation protection, we have CD-like I Bonds as a better alternative. To recap,

- Bonds and CDs are not mutually exclusive. You can have both.

- Bonds used to be better than CDs but no longer.

- Bonds are better than average CDs but the best CDs you can easily find are better than bonds.

- CDs can be used for long-term investing as well as short-term savings.

- You don’t need to keep 100% of your money liquid 100% of the time. Don’t pay for liquidity you don’t need.

- Having another account is not going to kill you. It’s good for your bottom line.

- It’s very easy to transfer money to a bank or credit union for CDs, even in an IRA.

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

indexfundfan says

By “transfer”, do you mean the transfer of assets from one custodian to another?

On Vanguard’s brokerage in-kind transfer form, it actually states that most CDs cannot be transferred.

Harry says

No. I meant transferring some dollars from an investment account to a bank or credit union to fund the CD. The bank or credit union will give you a transfer authorization form. It will go get the dollars from your investment account. Here’s an example from Discover Bank.

foss says

I think the location issue is the main problem (and the absolute $ increase in returns).

There is no easy way for me to get my bond fund $ out of my 401k and into a CD. It is now becoming increasingly correct to say that fixed income at paltry yields should sit in taxable accts. The problem is that for those of us with large allocations to fixed income in a 401k, this would require selling the fixed income (bond fund/treasury/TIPS) buying equity funds in its place, then coming up with new $ to purchase fixed income outside of the tax deferred acct – ie in taxable. Assuming a constant portfolio size, this is possible only by selling equities in taxable accounts which then incurs more taxable loss.

For 1% (e.g) of yield net of 30-40% of taxes, this is maybe $300-$500 net/year, at best (and potentially much worse based on tax status).

Sometimes inertia makes sense, or is guided by the unknowns.

If I could relocate my fixed income I would. At this point, I max out I-bonds and dump TIPS at around the same rate (buy I-bonds in taxable, dump TIPS in tax deferred), but it has for better or worse made me save more and buy more equities.

I do think it is a bit more complicated and in many cases, not worth the time involved.

Frank says

I agree with your article Harry. Currently, the fixed income portion of my IRA consists of three individual share certificates, of equal funding, at a credit union. The average dividend rate of the combined certificates is 3%.

John says

You mentioned that “For people in a high tax bracket investing in taxable accounts, muni bonds are still a better deal than CDs.” How would I bonds compare given that you can defer all taxes till maturity (when you will be in a lower bracket)?

Harry says

John – I Bonds work just like a variable rate CD, tied to inflation, with tax deferral. Whether munis or I Bonds will have a higher return in the end is anybody’s guess. Because of the annual purchase limit, in a taxable account just buy both if you are in a high tax bracket.

Ben says

Harry, how do you compare interest rate risk between CDs and bonds of different terms? VBMFX says it maintains an average term of 5 – 10 years in the bonds it holds, and the SEC yield is 1.45%. The Discover Bank CD you mentioned has a 1.85% yield on a 7-year CD (already gone down??) Does that mean these two have comparable risk levels?

Harry says

Ben – The interest rate risk is lower in CDs because the early withdrawal penalty is fixed and because its remaining time to maturity declines over time.

Mary says

Very interesting articles about CDs vs. Bonds — it helps to clarify the decision of where to put our fixed income allocation. So, to recap:

1) I could transfer assets from a Traditional IRA at Vanguard or a 401k at Schwab into a CD at Discover Bank? The assets would still be part of the IRA or 401k but would be held at Discover in a CD?

2) How can IBonds be held in a taxable account? For instance, they could not be held in my taxable account at Vanguard, correct? They would be held at TreasuryDirect, right?

3) For muni -bonds in taxable accounts for high-tax brackets, would you recommend buying the specific state bond in which I live which is Ohio?

4) What is your opinion on CDs linked to baskets of commodities? Our former Morgan Stanley advisor has tied up $350,000 of our money in these CDS for the next 3 – 5 years….which is awesome (not).

Thank you for directing me to your website through the Boglehead board….very informative and I look forward to reading more of your blog articles!

Harry says

Mary –

(1) IRA yes, 401k no, unless you are talking about the 401k of a former employer or if you are already 59-1/2, which can be rolled over to a traditional IRA.

(2) I Bonds will have to stay at TreasuryDirect or in paper form if you already have the paper bonds.

(3) Assuming you are talking about the Vanguard Ohio Long-Term Tax-Exempt Fund, that’s fine.

(4) Depending on the specific offer. See A Case Study On An Index Linked CD. If you are already in them, just hang on until they mature.

Mary says

Thank you, Harry. Interesting article about the Index linked CD, too. One more new Boglehead question:

What is the best way to perform rebalancing asset allocation with money tied up in 5 year CDs vs. something like the Total Bond Fund?

Harry says

Mary – As mentioned at the beginning of the article, it’s not all or nothing. You leave 10% of your portfolio in bond funds. That’ll be enough for rebalancing. The rest can go into CDs. See previous articles Diversify Bond Funds with CDs and +/- 5% Rebalancing Bands.

TJ says

Do you feel like today CD’s are still a better deal than bonds?

That Discover CD is up to 2.18% for a 7 year, BTW.

Harry Sit says

I do, for the same reasons in this article. You can get a 5-year CD at Synchrony Bank at 2.25% APY, with a 6-month early withdrawal penalty. Allan Roth wrote about it in Wall Street Journal in November 2014: A Low-Risk Route to High Yields on Savings.

Jim Pelluso says

Nice article. I think you have summed up most of the reasons why CDs are underutilized. I think the fixed income side of investing has always been a bit of an after thought – just buy a decent intermediate bond fund. That used to be pretty much true. The real excitement and sales pitch was what are you doing with the stock side? Also, brokers/brokerage firms don’t make money on CDs.

Another subtle bias is that CDs were for unsophisticated investors like grandma. Buying a CD is like having a rotary phone.

Finally, recommended allocations used to be categorized as stocks, bonds and cash. The last decade or so “they” have dropped the “cash” part.

Vic says

Not feeling confident in the Fixed Income side of my portfolio. Up until now it’s all been in FSITX. I’m consider moving some of it into CDs – but for simplicity I would likely purchase them through Fidelity as I’m not inclined to manage a lot of accounts.

Right now I can get 2.25 or 2.3 on new issues. Do I compare this to the 5 year treasure at 1.83% and say I’m good to go. The SEC 30 day yield on my bond fund is 2.36.

It’s the comparison – I’m feeling shaky about.

Thanks.

Harry Sit says

By choosing the simplicity of brokered CDs you give up a major benefit of having CDs — the ability to withdraw early at a fixed early withdrawal penalty in case interest rates go up a lot. There’s still a yield advantage over Treasuries but you also have less liquidity and no state income tax exemption in a taxable account. I wouldn’t bother at the rates you stated for brokered CDs.

James says

Through Schwab IRA accounts, since 2011 our family has constructed ladders of CDs with weighted average yields of approximately 3%. This has worked well, providing FDIC Insurance and management convenience inside the Schwab accounts. As CDs mature (and hopefully rates rise), new CDs are selected at the “end of the ladder” to lock down relatively higher interest rates.

Allan Roth says

Nice piece Harry. There is a chapter in my now 10-year old book called “Better than Bonds” which is a strategy of direct CDs with low early withdrawal penalties.

George says

Although is an old article, you recently linked to it, and I found it insightful.

I have purchased bank CDs in and out of IRAs for my cash ladder and everything you said agrees with my experience. I would add that I have found the transfer (rollover process), while not difficult, to take longer than I had thought. I did a rollover from a Schwab IRA to an IRA CD at Capital One, and it took almost a month. Fortunately the 3.1% rate for a 5 year CD didn’t go down until after the funds got there, but I was sweating it. I also more recently did a rollover from Schwab to Ally Bank IRA CD (2.85%). That was a little smoother. Once I got an email from Schwab confirming that they would accept a fax from Ally of the transfer request, Ally accepted the transfer request through their secure message system and the process took almost 2 weeks. Ally says that they will give you the higher of the rate at the time you opened the CD or the rate in effect when the funds are received (within 90 days). Also, in both cases, Schwab assessed a $25 fee for the IRA transfer. Since the rates I got were %0.3-0.4% higher than the best Schwab had to offer, the $25 is money well spent.

JK says

Having lost almost 55% of my taxable brokerage equity portfolio in the crash a decade ago, I liquidated my portfolio at the worst time and converted funds to CDs in Ally bank savings acct. They are in a regular savings acct. I have gone back to work since then.

When I do my taxes, the HRB tax software tells me that I should consider buying state munis to reduce my taxes. How should I go about buying them? Through a Bond Fund? I am a NC resident. I just googled and found one (Nuveen North Carolina Municipal Bond Fund). Have never heard of them before.

Do the munis offer similar safety and protection that CDs do? Are they not volatile unlike CDs? Nuveen bond fund FCNRX (67065P816 CUSIP), for example, has 52 WEEK HIGH/LOW of $11.33/$10.44 and a net & gross expense ratio of 0.62%. How does one evaluate that? Is that great, OK, or terrible?

Can you shed some light please? Thank you in advance.

Harry Sit says

Munis are only guaranteed by their issuer. They are not like FDIC-insured CDs. It’s difficult to get a diversified portfolio of individual munis except through a fund. The cost of buying and selling individual munis is very high. For a smaller state like North Carolina, it’s also difficult to get a fund that only invests in munis from that one state. I would say a 0.62% expense ratio on a muni bond fund is terrible. If you want munis, instead of buying a state-specific muni fund, consider buying a fund that invests in munis from many states, such as Vanguard Intermediate-Term Tax-Exempt Fund (VWIUX), with an expense ratio of only 0.09%. The interest from a national muni bond fund is still tax exempt for federal income tax. It’s just not tax exempt for North Carolina state income tax.

JK says

And how would I evaluate when/if any munis I buy are furthering my goal of tax reduction and corpus protection?

Thanks again-

Harry Sit says

A starting point is to compare the after-tax yield. If a CD pays 3%, and you pay 24% federal income tax plus 5.5% NC state income tax, your after-tax yield is 3% * (1 – 0.24 – 0.055) = 2.115%. When muni yield is less than that, yes munis will reduce your tax, but they will also put less money in your pocket. Sometimes you are better off paying more taxes when you still end up keeping more after paying the taxes.

Allan Roth says

Yes often people forget the goal-it’s better to earn more money after taxes than to pay less in taxes.

AngryLawyer says

Love your content…I was spending hours reviewing your site when I came across this gem. I am extremely risk averse (I am a 2x cancer survivor and do not want to risk principal…especially because I trade my time for money) and am trying to build a version of a Permanent Portfolio (Harry Browne came up with a portfolio allocation of Gold, ST Bonds, LT Bonds, and stocks with equal weighting and periodic rebalancing). Since I foresee inflation being elevated going forward, I do not think that LT Bonds are a good investment and was thinking about replacing them with CDs. What are your thoughts on this today? What are your thoughts on the ideal portfolio allocation?

Thanks!

Harry Sit says

CDs don’t offer inflation protection either. Consider TIPS and I Bonds if you’re concerned about inflation. See How to Buy I Bonds and Inflation Protection with TIPS.

An ideal portfolio allocation is one that you can stay with through thick and thin. There will be times when your version of a Permanent Portfolio does poorly relative to some other allocations. This applies to any allocation. Everyone must find something they won’t abandon when it doesn’t do well.