Fidelity Investments is best known as an administrator for workplace retirement plans and an online broker for retail investors. In addition to 401k/403b accounts, Traditional and Roth IRAs, HSAs, and taxable brokerage accounts, Fidelity also offers accounts that can serve the same purpose as checking and savings accounts.

Because Fidelity is interested in maintaining a full relationship with its customers for both banking and investing, and its primary focus is on investing, it’s in a good position to offer better rates and features on banking.

This is not a sponsored post. Fidelity isn’t paying me to promote it. I’m only writing as a satisfied customer of over 20 years. Here are two ways to use a Fidelity account to manage day-to-day spending and savings.

1. CMA as Checking

Fidelity Cash Management Account (CMA) is a separate account type from Fidelity’s regular taxable brokerage account, officially called “The Fidelity Account.” You must choose the account type when you open the account. A Cash Management Account can’t be changed to a regular taxable brokerage account after you open the account. Nor can an existing regular taxable brokerage account be changed to a CMA.

Included Features

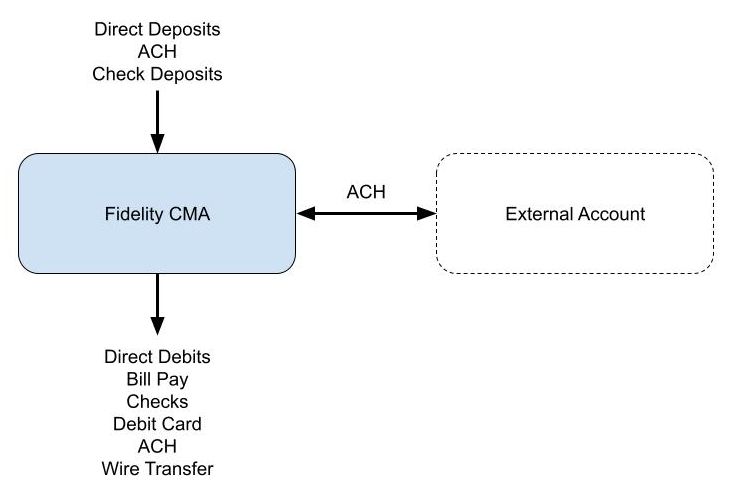

The Cash Management Account is specifically designed to meet banking needs. It has pretty much everything people need for a checking account, and nearly everything is free.

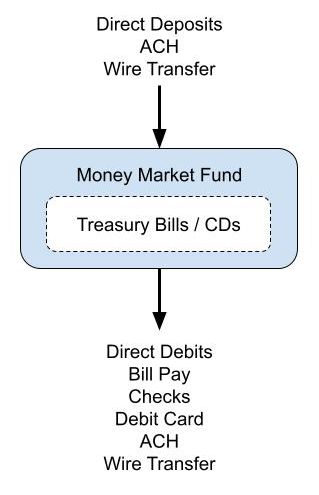

– FDIC-insured balance or a money market fund. The money market fund pays a higher yield.

– No minimum balance. No maintenance fee. It doesn’t require direct deposit.

– It provides a routing number and an account number for direct deposits and direct debits.

– It accepts check deposits by mobile app, in person at a Fidelity branch, or by mail.

– Free checkbook. No minimum amount for a check.

– Free Visa debit card for purchase, ATM withdrawal, and teller cash advance. No foreign transaction fee on the debit card when you always transact in the local currency. It doesn’t require using the debit card a minimum number of times per month.

– No fee to use any ATM worldwide. Fidelity reimburses the ATM fee charged by the machine.

– Free Bill Pay service with eBill.

– Free same-day ACH. Push up to $100,000 per business day out of Fidelity and pull up to $250,000 per business day into Fidelity by online self-service. Call customer service to transfer a higher amount.

– Free wire transfers. Up to $1,000,000 per business day by online self-service. Call customer service to wire a higher amount. You can also transfer to another person’s account by same-day ACH.

Choose Core Position

The “core position” in a Fidelity account is the default holding. Money coming into the account lands in the core position. Money leaving the account is withdrawn from the core position first.

You have a choice to keep your core position in either FDIC-insured banks or the Fidelity Government Money Market Fund (SPAXX). The money market fund isn’t FDIC-insured, but its underlying holdings are short-term government securities. I’m comfortable keeping my money in the money market fund for a higher yield. See No FDIC Insurance – Why a Brokerage Account Is Safe.

To switch the core position from the FDIC-Insured Deposit Sweep Program to the Fidelity Government Money Market Fund (SPAXX), log in to Fidelity’s website, click on the “Positions” tab, and select your cash balance. You will see a “Change Core Position” button.

Your chosen core position stays effective until you change it again. If you make Fidelity Government Money Market Fund (SPAXX) your core position, your existing core balance and all future deposits will automatically go into the money market fund.

The yield from the money market fund is comparable to the yield from many high-yield savings accounts, which don’t offer all the checking features, such as Bill Pay or ATM fee reimbursement.

Routing Number and Account Number

You see the routing number and the account number for direct deposits and direct debits when you click on the information emoji below the account name.

Choose “checking” as the account type if you’re asked to select one.

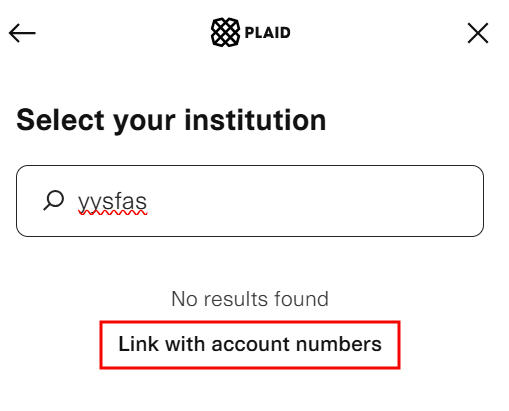

If your bank uses Plaid to link a bank account, search for a non-existent bank, and then click on “Link with account numbers.” It will make Plaid use a micro-deposit to verify your Fidelity account.

Limitations

Fidelity Cash Management Account has some limitations that aren’t a deal-breaker to me.

– It doesn’t accept deposits of physical cash or money orders.

– The check deposit limit by mobile app may be low for new accounts. The limit increases over time.

– It doesn’t support Zelle. Venmo or Cash App are better alternatives.

– It doesn’t link instantly through Plaid (see screenshots above for how to link with account numbers in Plaid using micro-deposits).

– It doesn’t offer sub-accounts for tracking separate goals.

– It doesn’t provide cashier’s checks.

– Recurring ACH pushes out of Fidelity only support monthly and annual frequencies. Recurring ACH pulls into Fidelity only support weekly, biweekly, and monthly frequencies.

– The “deposit received” alerts are sent only on the next day, and the email doesn’t include the deposit amount. Text message alerts include the deposit amount, but they’re still sent only on the next day. Debit alerts are sent in real time.

I use my otherwise dormant US Bank checking account on those rare occasions when I need to deposit physical cash, get a cashier’s check, or set up recurring transfers on an odd schedule. I don’t use sub-accounts to track separate savings goals. Deposits are usually on a fixed schedule or done by me. The “deposit received” alerts aren’t as important as debit alerts.

Transfer Money by Push

Fidelity may hold ACH pulls and check deposits for up to 7 business days. The hold period varies by account history and the amount. My most recent ACH pull of $50,000 was held for only 2 business days. The money still earns interest while on hold. It’s only not available for withdrawal or transfer to another account.

When you ask Fidelity to transfer money from your external bank account, you see a warning like this before you hit Submit:

Stop, read, and take it seriously. This applies to mobile check deposits as well. You won’t be subject to a hold if you use the right way to transfer money. When you transfer money out of Fidelity, initiate the transfer at Fidelity. When you transfer money into Fidelity, initiate the transfer at your external bank. When you have a large check to deposit, deposit it at your external bank account, and then initiate a transfer at the external bank.

I make all deposits by an ACH push. Following this one simple rule avoids holds or getting the account restricted for fraud.

Secure Your Debit Card

The account comes with an optional Visa debit card. The debit card can be used for purchases without a PIN when it’s run as a credit card. This creates a problem in case your debit card is lost or stolen. A user posted on Reddit that he or she was having a hard time getting the money back after thieves bought $6,000 worth of gift cards with the stolen debit card.

It’s better not to carry the debit card with you in your wallet. If you prefer to use a debit card for purchases, put it in Apple Pay or Google Pay and tap your phone to pay. It’s more difficult for criminals to crack a phone than to tap your lost or stolen debit card everywhere. Keep your debit card at home and only take it when you expect to withdraw cash at an ATM.

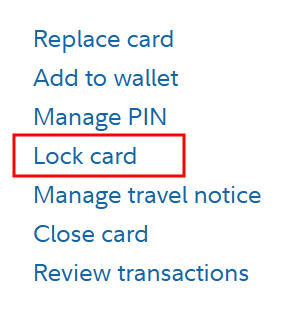

You can also lock your debit card on Fidelity’s website or in the Fidelity mobile app. Locking the card makes it decline all transactions. I previously used the debit card in Venmo to pay friends for shared expenses. Venmo also works with a bank account. I added the Fidelity account as a bank account in Venmo and removed the debit card. Now my debit card is securely locked at all times. I’ll only unlock it when I need to withdraw cash.

To lock the debit card online, open a new tab in your browser after you log in to Fidelity and go to fidelitydebitcard.com. Find your debit card and click on “Lock card.”

If you install the Fidelity mobile app on your phone, you can unlock the debit card right before you need to withdraw cash and lock it again when you’re done. Tap the head icon on the top right to find “Manage debit cards” in your profile in the Fidelity app. Tap “Lock or unlock card” on the next screen to lock or unlock the card.

Link to External Account

When you use a Fidelity CMA as your checking account, you can link it to an external account as you normally do with a checking account. For example, the settlement fund in a Vanguard brokerage account pays a higher yield. You can use Vanguard as your savings account to earn a slightly higher yield while using the Fidelity CMA as your checking account. The bulk of your cash earns the higher yield at Vanguard, while the amount you need for spending earns a slightly lower yield in the Fidelity CMA.

2. CMA as Checking/Savings Combo

Instead of linking to an external account as the “savings” part, you can keep both “checking” and “savings” in the Cash Management Account. This earns less interest, but it avoids transferring back and forth between two accounts. I do it this way because it’s simpler and it doesn’t forego that much interest.

Buy Another Money Market Fund

Although the CMA is designed for banking needs, it’s still a brokerage account. With some exceptions (no margin or options), you can buy in the CMA pretty much everything available in a regular brokerage account. This includes stocks, bonds, brokered CDs, mutual funds, and ETFs.

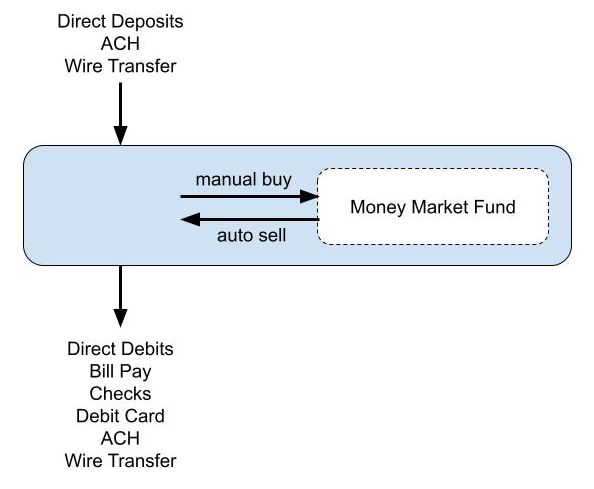

The CMA becomes a checking/savings combo when you buy a different money market fund in it. The core balance in the CMA serves as the checking part, and the manually purchased non-core money market fund serves as the savings part. Fidelity will automatically sell from the non-core money market fund when your core balance in the CMA is insufficient to cover a debit. This is like having free automatic overdraft transfers from savings to checking.

Some people prefer to buy Fidelity Money Market Fund (SPRXX) or Fidelity Money Market Fund Premium Class (FZDXX). These funds pay a slightly higher yield than SPAXX in the core position. Some people prefer to buy Fidelity Treasury Only Money Market Fund (FDLXX), which has more of its income exempt from state income taxes. None of these funds can be set as the default core position, but you can buy them manually. See Which Fidelity Money Market Fund Is the Best at Your Tax Rates.

Because Fidelity will automatically sell from the non-core money market fund to cover debits, if you’re so inclined, you can be aggressive in keeping the core balance in the CMA low while keeping the bulk of your account in a non-core money market fund earning a slightly higher yield. Or you can set a maximum target balance alert using the Cash Manager and buy more shares of the non-core money market fund when you have excess cash in the “checking” part.

Some people prefer to just keep everything in the default Fidelity Government Money Market Fund (SPAXX) because the extra yield from a non-core money market fund is quite small.

Cash Manager Not Needed

You may have seen some convoluted setups using the Cash Manager overdraft feature in the Fidelity CMA. It’s unnecessary and undesirable.

The only thing remotely useful in the Cash Manager is the maximum balance alert. An alert only tells you that your CMA core balance has exceeded the maximum target balance. It doesn’t automatically buy a non-core money market fund in the CMA for you. You still have to buy it manually if you want.

You don’t need an alert for the CMA core balance dropping below a minimum balance when you have enough savings in a non-core money market fund held in the CMA. Selling from the non-core money market fund held within the CMA to cover debits works out of the box. It happens automatically even if you don’t set up anything in the Cash Manager.

The Cash Manager has a “self-funded overdraft protection” feature to link the CMA to another Fidelity account. This is unnecessary and undesirable when you want the CMA to stand by itself. You don’t want unauthorized debits to affect your other accounts.

Add Treasury Bills or Brokered CDs

If you’d like to take it one step further, you can also buy Treasury Bills or brokered CDs in the CMA when you have money that you know you won’t need for some time. The CMA then becomes a checking/savings/CD combo. The money automatically goes into the “checking” part when the Treasury Bill or brokered CD matures. For example, the amount set aside for the next property tax bill can go into a Treasury Bill or a brokered CD. See How To Buy Treasury Bills & Notes Without Fee at Online Brokers and How to Buy CDs in a Fidelity Brokerage Account.

Please note that if you enable the “auto roll” feature when you buy new-issue Treasury Bills or brokered CDs in the CMA, the amount for the next roll reduces your “available to withdraw” number for a few days during the roll. A debit may fail if you don’t have enough available to withdraw. It’s not a problem if you don’t use auto roll or if you keep a substantially higher amount in a money market fund than the amount for the next roll.

Using a Fidelity CMA for spending and savings becomes truly set-and-forget. All deposits automatically earn a good yield in a money market fund. All debits come out of this money market fund. It’s like using a savings account as a checking account. You can buy a non-core money market fund manually, but you don’t have to. The yield on the default money market fund is close enough to that on another Fidelity money market fund.

You can still buy Treasury Bills or brokered CDs to set aside money for specific bills in the future. Please note the caveat on “auto roll” and “available to withdraw” mentioned above. It’s better to do it in a different brokerage account if you prefer to use “auto roll.”

***

The biggest draw of using the Fidelity CMA for spending and short-term reserves is the checking features. You effectively use a savings account as a checking account and earn a good yield from the first dollar. Everything is seamlessly together.

A Vanguard money market fund and some less well-known high-yield savings accounts pay more, but they don’t offer checking features. When you pair it with a checking account that pays close to zero, the blended yield on all your cash goes down. You might as well put the whole thing in a Fidelity CMA and eliminate the need to watch your checking account balance and transfer back and forth between two accounts.

Transitioning a checking account takes some time and effort. Banks know it. That’s why they pay you close to zero in checking accounts. They bet that you think it takes too much work to switch. Don’t fall for it. It’s easier than you think when you take your time to make the move.

The most frequent problem I see when people use a Fidelity CMA is an unexpected long hold on check deposits and ACH pulls. You won’t have this problem when you do all your deposits with an ACH push. In other words, initiate the transfer into Fidelity outside Fidelity. See 3 Lessons Learned From a Botched Money Transfer.

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

MR says

SPAXX has less treasury composition. So some of the states like CA will have tax. I prefer FDLXX – Full treasury Tbills. I buy it manually in my CMA. Great article. Thanks!

Art says

I do something similar in my brokerage but it seems less flexible — or maybe I just haven’t explored possibilities. Great article and very timely. Trying to figure out if I need to create a separate set of “cash management” accounts or if the mm ones I already have serve the same purpose. I believe Elan uses one of my brokerage mm accounts as “cash” to transfer. Cash back rewards. Can $ be transferred from standard brokerage mm to the CMA or dies it have to come from a bank via ACH?

Harry Sit says

Money can be transferred between two Fidelity accounts instantly.

Roland says

Hi Harry,

Is it safe to have both CMA and regular Fidelity brokerage accounts? you mentioned that “The Cash Manager has a “self-funded overdraft protection” feature to link the CMA to another Fidelity account or an external bank account. ” Is this “self-funded overdraft protection” CMA account feature the default setting or I have to activate it myself.

For security reason, I DON NOT want to link my CMA acct with my regular brokerage acct. So in case my CMA Acct Debit card is lost or compromised, my funds inside regular brokerage acct will be safe.

Harry Sit says

Everything under Cash Manager is optional, not enabled by default. It’s safe to have both a CMA and a regular brokerage account when you don’t link the two accounts in Cash Manager.

V says

@harry, CMA CM automatically tops up your CMA balance from your linked bank account when it goes below a set threshold, any specific reason you don’t like this feature?

Harry Sit says

Whatever money you use to top up the CMA balance can stay in the CMA to begin with. More movements create more chances for mishaps. The top-up transfer initiated by the Cash Manager also requires time to settle.

The SF Giants says

As of this morning on 6/19/2024, I was able to change the core position on my Cash Management Account from the FDIC-Insured Fund to the Fidelity Government Money Market Fund (SPAXX). Thanks, Harry, for the “heads up.”

Bob says

Looks like I have the same option to change my Core position on my CMA now, too. I’m going to wait and call tomorrow to make sure nothing changes as far as debit card and/or checks…or more importantly, an autopay to a credit card that happens on Sat. My luck, I’ll change it now and it will mess all the other stuff up.

Thanks for the info, Harry!!

MS says

Thank you Harry and I was able to change my core to SPAXX. I had to go through the chat bot, but it was seamless and painless.

Barbara says

How do I know if my CMA account is linked to another account? I don’t recall being asked when I set up the account last year, but if it was worded as overdraft protection, I may have. I have since opened a separate brokerage account and want to be sure it is not linked to the CMA. Thank you.

Harry Sit says

It’s not linked unless you proactively linked it. Look for the “Access cash manager tool” link on the Summary tab of your CMA. Then look under “self-funded overdraft protection.”

Stephen says

Please add one more disadvantage to the Fidelity account. Fidelity does not accept Money Orders for deposit. We had one tenant that liked to pay in money orders so we maintain an account at a local credit union for these deposits and then ACH them over to Fidelity.

Please add one more advantage to the Fidelity brokerage account. Fidelity offers a cash back credit card that offers unlimited 2% cash back that deposits automatically to the brokerage account each month.

Thank you for this update, this will mean fewer account transfers for us!

Harry Sit says

I added not accepting money orders for deposit in the limitations. The Fidelity co-branded credit card is a product from Elan (US Bank), not Fidelity. Fidelity makes some money from Elan by marketing the card. It’s an OK card but it isn’t anything special.

Harry Sit says

What used to be “3 Ways to Use Fidelity as a Bank Account” is now “2 Ways” because the previous third way has become redundant. I also added a new section on debit card security. Lock it!

RobI says

Is it now worth adding a CMA if I already use my Fidelity brokerage account with core money market fund like a savings/ checking bank account? I see the mobile check deposit as one extra feature but are there others?

Randy says

I do mobile check deposits to my Fidelity (brokerage) Account.

Harry Sit says

If you’re using a separate brokerage account for spending and short-term savings (the previous third way), it’s the same as using a CMA except that the ATM fee reimbursement in a regular brokerage account requires having Premium Services or Private Client Group. It’s not necessary to switch. Mobile check deposit also works in a regular brokerage account. If you’re using a single brokerage account for both spending and long-term investing, many people prefer to have separation between spending and long-term investing. Any hiccups in the spending account won’t affect the account for long-term investing and vice versa.

GeezerGeek says

Thanks Harry! Great article. Do you know if the Fidelity CMA “Bill Pay service with eBill” uses the customer’s account information when sending checks by mail to payees or do they issue checks from another bank account? I’ve heard some bill pay services issue customer checks while others use bank checks. Of course, the disadvantage of using the customer’s account to issue checks is that it raises the possibility of the customer’s account information being stolen while the check is in the mail. Check theft from the mail has become more common recently.

Santa Claus says

Fidelity BIllPay uses the routing number and account number of the actual account. I only use BillPay to send to TRUSTED people or businesses; the majority of my bill payments go directly to the recipient because they are “large billers” with arrangements with the Bill Payment service. (CheckFree, if I recall.)

Yes, one time mail was thefted and the thief tried to use our account for paying their phone bill and a few other services in the Chicago area. We had to do the “rotate account” business, which was a true pain because at that time (7 years ago) there wasn’t the capability to copy forward bill payment information between accounts.

At the same time, and after consultation with my local Loop Fidelity dude, we set up three accounts: one for direct debits (e.g., Mortgage and some credit cards), one for big billers like the gas and electric companies, and one for “local vendors” which were delivered via US Mail. This restricted the blast radius of purloined account information to just one segment instead of all of them.

Art C says

I wish Fidelity do something like my Citi Double Cash Credit Card would let you create a Virtual Credit Card, aka, Virtual CMA account number to you to generate for Bill Pay. Similiar to the idea of Call Forwarding, etc.

Harry Sit says

I have everything on auto pay with the billers. This guarantees that the payments are processed electronically. It avoids check theft and lost or delayed mail.

Mighty Investor says

Thanks, as always, Harry. You are like Fidelipedia!

Art says

I’m not sure if a “cash” position in brokerage is actually a CMA account. I generally send cash back and deposits via ach to it, then move $ to FDLXX. Would I need to to open a CMA account separately and duplicate Fdlxx there? Aside from protecting funds in brokerage from unauthorized w/drawal is it beneficial?

Harry Sit says

The cash position in a brokerage account is a holding in the brokerage account. The CMA is a separate account. They’re not the same. Using only the brokerage account works if you don’t mind mixing spending with long-term investing. The only benefit of having a CMA in addition to the brokerage account is to create separation. I find the separation helpful but it’s more work if you don’t want the separation.

woodstock99 says

I have a brokerage account. I am still working and have a portion of my paycheck go into that account via DD along with CD’s as my emergency/cash bucket account allocation and a separate checking/savings account with BOA. I use BOA for BillPay. I have a BOA debit card but I have the debit featured turned off – only use it for ATM withdrawals. I do have checks for and bill pay with brokerage account but have not used. I don’t recall getting a debit card. When I retire I planned to keep all as is but would it make sense to close the BOA and open CMA and do all deposits (either direct like SSA or pension or checks) and bill pay from CMA? I do not link Fidelity or BOA now. I have occasionally done ACH from one to the other as needed. Do people keep local or national bank with small balance as a backup? I also do not allow auto-draft to any payees but people say to set up Medicare and critical payments to be auto-draft just in case as we age. I had Zelle via BOA but I disabled it. I used it infrequently and now if anyone asks me I just say I do not use cash apps except for PayPay which I have used for many years with no issues. Sorry I know this is a lot and long way around to ask if I should open CMA in lieu or in addition to BOA. Thanks.

Harry Sit says

Moving Bill Pay to a Fidelity CMA will make your money for Bill Pay earn more interest. If none of the listed limitations (Zelle, cashier’s check, depositing physical cash, …) affect you, a Fidelity CMA can completely replace your B of A account. If the B of A account doesn’t require a minimum balance, you can certainly keep a small amount in it as a backup.

RobI says

I’m keeping the BOA checking open for the reasons Harry lists (Zelle and occasional Cashiers checks). To eliminate BoA fees, I’m keeping one pension payment as direct deposit and automatically move that money to Fidelity when it arrives each month. Otherwise BoA requires $1500 min balance.

GeezerGeek says

Thanks Santa! I’ve got another bank account that I have been using for paying bills. That account has a marginal balance for, as you say, “restricted… blast radius of purloined account information”.

Arsenio says

How do you guys handle personal finance apps with a Fidelity CMA? I’m using Quicken Simplifi. Obviously every time a transaction comes out it sells an equivalent of the core position. I end up with so many transactions in the account. Do you all just do manual entry?

Stephen says

I also use Quicken Simplifi. The authentication recently changed which somehow caused these hidden transactions to become visible and yes it is quite frustrating.

What I did was to create two rules to automatically categorize these into Fidelity-Core-Purchase and Fidelity-Core-Redemption and like transfers they SHOULD cancel each other out, but it really doesn’t matter because I verify the categorization to ensure that these transactions are hidden from Reports and hidden from Spending Plan. (When a transaction is categorized I mark it as cleared so I have a starting point from my last verification.) I wish I could automatically hide these too, but that seems to be too much.

Now I have read on https://community.simplifimoney.com that some people delete these transactions, but others indicate that they just come right back at the next sync. I’ve not messed with this, but it might be worth a try. This is best supported over on the https://community.simplifimoney.com support site.

Bill Cason says

This is an excellent write up. Does anything similar exist for Schwab?

TEM says

Schwab checking is a different account than brokerage, so while you can set checking overdrafts to come from brokerage, that means you need to leave cash in brokerage, at a low interest rate, Schwab will not sell MM funds to cover checks like Fido does. And Schwab does not have a decent core account. So you have to keep buying and selling MM funds to get a decent rate on cash. I used to use Schwab for checking, but the final nail in the coffin was when they started making me physically call to validate any ACH transfers to “online” (their term) banks, like Sofi and Ally.

GeezerGeek says

A couple more downsides about the Schwab CMA, which Schwab calls Schwab One.

The Schwab One account has two sets of routing numbers: one set for deposits and another entirely different set for withdrawals. Maybe some folks see that as security enhancement but it a pain to try set up transfers within another account. For example, I can a credit card account that I use with a bank for payment of credit card and for deposit of reward dollars.

The Schwab debit card is not contactless, which means you cannot set it up in Google Wallet or something similar. If you want to use the Schwab account to withdraw funds at an ATM, you have to use the card. As has been pointed out, there is a higher risk with carrying an ATM card in your wallet

Art says

I am a long time user of Fidelity CMA, and brokerage accounts, & within my CMA I do have SPAXX as my core & FDLXX as my non-core MMF. Although the yield are pretty good these days, but your readers need to understand & accept the fact that all of these MMFs do have their expense ratio at 0.42%; with exception for FZDXX at 0.36% but it has a minimum to invest at $100,000.

Thanks for the great article regarding how it can meet many of our banking & investing needs in one account. Continue your good work to inform your readers. Thanks

Harry Sit says

The higher expense ratio explains why a Vanguard money market fund of the same type pays 0.32% more (5.27% versus 4.95% as of 6/19/2024). Use the first setup if earning more interest is more important than keeping everything in the same account and avoiding transferring back and forth between the “checking” part and the “savings” part.

Steve says

Thanks for the post. Somes questions after reading it and the comments:

1. If I set up a CMA, does it provide the ability to transfer money between the holdings in the CMA by means of phone calls to automated telephone system? I use this method now with my current bank and like not having to use a computer/smart phone to make transfers and check account balances.

2. I use BillPay in a regular Fidelity brokerage account to pay a monthly bill. My belief is that the bill is paid via electronic transfer to the leasing company – not via mailed check.

Is there a security risk to my brokerage account from using Fidelity Bill Pay in this way?

3. You mentioned that CMA debit card does not require PIN when used for non-ATM purchases. No way to deactivate that “feature”? Is that typical of other debit cards? I have debit card from my bank which I use occasionally for ATM withdrawals. I have no credit accounts at the bank. I’ve never tried to make a purchase with the debit card but I assume if I did, the PIN would be required.

Harry Sit says

I used Fidelity’s Automated Service Telephone (FAST) in the 1990s before online trading came along. Apparently it’s still operating. Here’s the FAST Quick Reference Guide. If you’re thinking of buying into a non-core money market fund, it falls under “buy/sell/exchange mutual funds.” Since you already have a regular Fidelity brokerage account, you can try the automated phone service in your brokerage account now. It’ll work the same in a CMA.

If you’re sure the Bill Pay is delivered electronically, I don’t see a security risk, but you don’t have control over how the Bill Pay provider pays the bill. Electronic payments today can turn into a check in the mail next month when either the Bill Pay provider or the biller decides to make a change.

All debit cards with a Visa or MasterCard logo can be used for purchases without a PIN. The terminal may prompt for a PIN but you can hit cancel and run it as a credit card. Try it with your bank debit card next time.

Steve says

Harry: Thank you for your reply. I spoke to bank who confirmed debit card can be used for non-ATM purchases without entering a PIN. Bank said they also issue ATM-only cards.

A bit off-topic but here it goes: In case of fraud, credit cards are considered to have better recovery protection for the cardholder, compared to debit cards. If I have relatively high credit limit on my credit cards, which I use for most purchases and could draw on for an unexpected funds need when traveling (and pay back same month), is there any reason not to eliminate debit card and get an ATM-only bank card? Is there some other feature of debit card that I’d be missing?

Harry Sit says

Many banks don’t issue ATM-only cards anymore. If you can still get one from your bank, by all means get one.

Lori says

I have an atm-only card for my local bank account and would recommend it for peace of mind for everyone who never pays with their debit card. The regular debit card I have is only for travel in case I do want to withdrawal foreign currency.

Harry Sit says

Your ATM-only card may also work in another country if it has a Plus logo on the back. Plus is operated by Visa. Machines that support Visa also tend to support Plus. Try it when you travel next time.

Jen says

I don’t have a CMA account, but rather a borkerage account with Fidelity that allows me to do most of what you listed here. I can pay bills online or use a checkbook to pay. It looks like I can order a debit card for it as well.

Harry Sit says

Using a separate brokerage account used to be the third way. It’s made redundant after Fidelity added a money market fund as an option for the core position in the CMA. No need to change it when you already have it but anyone starting fresh should go with a CMA for day-to-day cash management and a brokerage account for long-term investing.

Jen says

I didn’t know you could get an atm only card instead of a debit card!

Our solution to debit cards was to not activate them when we were required to have them. That is what our banker advised. We were required to take them in order to have online access.

Harry Sit says

To be clear, it isn’t an option to get an ATM-only card from Fidelity. It may not be an option at your bank either. Some banks and credit unions still offer the option only if you know to ask for it but many places only issue “standard” debit cards.

Art says

You can lock the debit/ATM card and only unlock it as needed.

“Locking the card will prevent any new withdrawals or purchases to be made on the card while locked. You will also be unable to add the card to a digital wallet or person-to-person payment app. Recurring transactions, returns, and credit adjustments will still be allowed. You may go online to unlock your card at any time.”

jen says

Thank you for the debit card info. I checked Fidelity and none of our accounts have them. Our regional bank does not have an ATM option, but when we received the debit cards, we were told we did not have to activate them. They were required in order to have online access (no idea how that is connected). So we keep them in the safe, not activated. I will check our other financial institutions.

Mark Pugner says

Note: as of July 2024, you can set the core position of a CMA to SPAXX, which will earn a higher interest rate compared to the default FDIC Sweep.

Pete says

Great write-up. Thank you so much. Does the CMA account allow for downloads in .qif format? I download/import .qif files from various sources into an ancient free version of Quicken to aggregate transactions across accounts and do various kinds of reporting. I’ve come to rely on this facility and wouldn’t want to open an account that didn’t support it.

Harry Sit says

I only see downloads in CSV format. There may be ways to convert CSV to qif format.

GeezerGeek says

Years ago, I used Excel to manipulate data into QIP format and then pasted the reformated data into a text file with a qif file type. The format for the Quicken Interchange Format (QIF) is documented in Wikipedia. Yeah, it take some work to set it up but after creating an Excel spreadsheet with formulas to convert the data, the conversion would be a reduced to a few cut and paste operations. That isn’t as easy as directly importing a QIF file into Quicken, but it is a possible work-around.

FDIC vs SIPC says

In a financial crisis, using the Fidelity CMA rather than a regular brokerage acct could provide a valuable advantage (depending on acct balances) in that it apparently just takes a few clicks to change from the uninsured money market sweep to the insured FDIC option.

Golden says

Does it make sense to have a Fidelity CMA just as an alternate “bank” account, without having any other Fidelity account? Will Fidelity allow that?

Harry Sit says

Fidelity allows it. Everything in this post works without any other Fidelity account.

Stephen says

@Golden : You should always have a secondary bank or credit union in addition to your Fidelity transaction account as something will come up that Fidelity does not offer like Zelle.

In my case, Fidelity is my primary account and my credit union can handle all other transactions, including transfer funds to my Fidelity account via ACH.

GeezerGeek says

@Golden, another reason for having a second bank account with the Fidelity CMA, is that you can use the second bank account for Bill Pay instead of using the Fidelity Bill Pay. When it is not possible to complete a Bill Pay transaction electronically, Fidelity mails a check that is written on the customer’s account. By doing that, there is a risk of exposing the customer’s account information to fraud if the letter is intercepted in the mail. You can lower the financial risk if you use Bill Pay in an account with a low balance. Some Bill Pay services mail checks that are written on an account that is not the customer’s account but Fidelity uses the customer’s account information on mailed checks when it is necessary to mail a check for payment.

jen says

@Geezer Geek, we have 2 accounts now at banks because of check fraud. Yes, it’s extra work, but we like the extra protection it offers. We started this with our business account because we frequently had to give out our account information. It made me nervous. So our banker told us to open a second account and that it was very common for businesses to do that now. So at Fidelity, I opened a 2nd account that has not check writing enabled. We transfer money as needed to the one that has that capability. We also have a feature set up that allows no money to transfer out of Fidelity (called lockdown mode). So I can pay bills, but money cannot move money randomly to other institutions.

David Rhoades says

Harry:

FYI:

I don’t have another Fidelity brokerage account.

I just opened up a Fidelity CMA account today, and was unable to order checks for it. The reason:

“We’re sorry. You’ve requested a feature that requires a personal account (brokerage, IRA, 529, etc.).”

I’ll call Fidelity tomorrow to see what I need to do to rectify this.

Thank you,

Dave

Harry Sit says

Maybe it was just too soon. One part of the system hasn’t fully registered that you have a CMA now. I would try again in a few days. In general, it’s a good idea to slow it down when you set up a new account.

GeezerGeek says

I got the same error but if you go back to the summary page and order checks from the page with the account information on it, it will work. That is a bad link that Fideilty needs to fix.

David Rhoades says

Thank you all for your assistance, I will try GeezerGeek’s recommendation.

My credit union, San Francisco-based Patelco Credit Union, has effectively been shut down since last Friday, 6/28 due to a ransomeware attack. Go to the referenced link to see the impact on its customers”

“Please visit the dedicated webpage that will be updated daily with the latest, most pertinent information including service updates at patelco.org/SecurityUpdate.

We continue to work alongside leading third-party cybersecurity experts in support of this effort. We have also been cooperating with regulators and law enforcement.”

Arsenio Martins says

For those of you commenting about security and bill pay I’ll recommend a couple of services.

One is called privacy.com. They give you virtual cards which you can restrict to certain vendors if you want or you can restrict the card to a certain amount monthly. They can also issue one time use cards which will expire after the first charge. Great for trials in case you forget to cancel. They also have a plug in for your browser so it will auto fill a generated card for you. Works on computers and mobile phones. [referral link removed.]

Another that I use is Papaya. It’s a free bill pay service. You can connect a bank account or a debit card. You take a picture of your bill and it can automatically pull all the data from it like addresses and account numbers. Just another layer of separation.

[referral link removed.]

Hope it helps someone!

Bart says

Great article.

I am trying to help my friend to create emergency fund in addition to his Tra IRA.

I personally have brokerage account and trying to figure out what would be best for him.

Can you open CMA and ask not to issue the debit card and checks and just use transfer feature like in individual account. Because its purpose is to be an emergency account not having a card would be beneficial and money can be pulled only via transfer to regular checking in case of emergency. That can be done with individual account.

The only advantage I see is fee reimbursement and FDIC protection, yet if this is to be an emergency found it is important to have a higher yield so more money is saved. There is also cash manager that is probably of no use.

Individual account allows also to change core to FZFXX in addition to SPAXX.

Does individual FCASH have FDIC protection?

Are there any gotchas in CMA compared to Individual when it comes to trading? Can you do everything you can in individual account?

Those two are so similar yet above differences exist that are not necessary and there could be just one account with 2 cores. One for savings one for trading.

Harry Sit says

Both CMA and a regular brokerage account will work. CMA comes with a debit card by default but you can lock or close the card after you receive it. Checks aren’t enabled by default in either account. FZFXX isn’t any better than SPAXX. It isn’t a reason to favor a regular brokerage account. FCASH doesn’t have FDIC protection. CMA can do everything a regular brokerage account can do except margin, option, or foreign currency trading but it doesn’t sound like those limitations matter to your friend.

In the end, CMA is for cash management and a regular brokerage account is for investing. It’s better to use an account type for its intended purpose. Turn off or ignore features you don’t need for now and turn them on as your needs change.

Bart says

Thx Harry.

Just opened CMA and seems like Debit Card is not sent out automatically and can be order either at the time of opening or later, This will work great for my friend as there will be no temptation to use any money in CMA that is to server as Emergency fund.

I think this is the best summary of which account to use:

”

In the end, CMA is for cash management and a regular brokerage account is for investing. It’s better to use an account type for its intended purpose. Turn off features you don’t need for now and turn them on as your needs change.

“

Unmesh says

Harry,

One of your options is to use an external linked account such as Vanguard for purchased MMFs. A 0.32% yield spread can become significant though I vaguely remember Vanguard not allowing me to designate beneficiaries in the past.

How long do ACH transfers take between Fidelity and Vanguard in your experience?

Thanks

Harry Sit says

It’s been a couple of years since I closed my Vanguard taxable account. If I remember correctly, pushes out of Vanguard arrived on the next business day. I don’t know whether that’s still the case today.

RobI says

I use this approach with Fidelity and Vanguard as a bucket strategy. Vanguard money market (VUSXX) is my medium horizon savings (bucket 2). I then move the Vanguard dividends monthly to Fidelity money market for short term dividend paying cash spending (bucket 1).

Vanguard to Fidelity ACH transfers are next business day.

Vanguard brokerage account does allow for designating beneficiaries. Can’t speak to CMA

Learningeveryday says

Thanks for the write up Harry. Other sites refer to your article too! Love it. I have an existing fidelity brokerage account(s). I presently use a standard B&M bank (BOA yup!) and transfer funds manually to fidelity and vanguard but use the bank for CC and bill payments. Certainly i lose interest from moving and parking some cash in the bank. I would love to move them almost all to Fidelity with better rates. My one concern is fintech risks in accessing when needed. As an example did anyone else have an issue accessing their fidelity account two weeks ago in the first hour of trading (the yen carry trade mess or whatever meltdown monday?). I couldn’t access for the first hour. Same issue in vanguard. My bank online account and ME worked without a glitch that day. Those who had a CMA account, did you have a similar issue or was it just the brokerage accounts that had this issue. Honestly one hour isnt the end of the world but could be a sentinel event for even longer shutdowns. Do you feel this is a valid risk to include in considering Fidelity CMA accounts or as it is so rare, not one to worry about? Thanks again

Thomas Martin says

I use a Fidelity brokerage for all my bill payments. The sign-in problem (which also affected other brokerages) had absolutely NO impact on any cash payments. One to BOA was processed that day. The cash portion works just like a checking account, the fact that you can’t sign in does not affect ACH transfers usoing routing and account nos.

Harry Sit says

Using a brokerage platform raises the probability of an outage caused by the peak demand for trading. A banking platform doesn’t have such peak demand. That’s true but I don’t worry about this minor inconvenience. It doesn’t happen often, and when it happens, hardly anything mentioned in this post must be done right at that moment and can’t wait until the market is closed. As Thomas said, backend processing isn’t affected by the website or app outage. I don’t think debit card authorizations were affected either. The only thing may be if you must send a wire that morning to meet a deadline. It can be done by calling customer service or visiting a branch if you must do it in a pinch. When you use the account as a checking/savings combo (the second way in this post), you know you have enough money for all your bills. Checking the balance isn’t even that important.

Learningeveryday says

Thanks Harry and Thomas, Those are good points. There is usually no urgency that would need constant access and being able to call them to get things done is a good idea. And the backend operations are not usually (hopefully) affected in these crisis. I am probably over thinking fintechs, brokerages and their risks in becoming ones primary banker but was using the transient lack of access to describe a risk when we tie everything together. Hopefully it doesn’t happen again but I suspect it will. Another separate issue (that u may already covered in your other write ups) is the one recently with synapse and intermediaries with fintechs. Still everything in life is a balance between risks and returns. I am gradually warming up to this. As always thank you for the write ups.

Harry Sit says

Fidelity isn’t a fintech. Fidelity and fintechs both use banks to process certain things but the similarity stops right there. Fidelity is a well-established broker and fund manager. It’s a foundational function of a broker and a fund manager to track who owns how many shares in which stocks, bonds, mutual funds (including money market funds), ETFs, … and reconcile with actual assets held in aggregate by the broker and the fund manager. Fidelity has done it every day for decades. The cash management features (ACH, debit card, bill pay, …) only provide access paths to the brokerage account. After those access paths arrive at the brokerage account, they translate into buying and selling shares in a mutual fund, which Fidelity does in the same way as it does for everything else. If you have doubts in Fidelity actually having the underlying assets for the money market fund shares it shows in your account, you would have much bigger worries for the stocks, bonds, mutual funds, and ETFs people have in their brokerage accounts.

Learningeveryday says

Thanks for explaining further Harry. I have to read more on the middleware, intermediaries etc. FDIC (which doesnt apply here) for banks and the way it works is so much easier to follow than what happens at giant brokerages like Fidelity with CMA accounts. Being such a giant institution its also hopefully too big to fail so thats another reason to feel safe for now. Any resource you would recommend for more reading? On a positive change, fidelity has just updated their CMA information and now they officially say there is no FTF for their debit card including purchases. EDIT: And you have already updated that in that page of yours, wow you are fast!

Have a great week.

Harry Sit says

If the linked post No FDIC Insurance – Why a Brokerage Account Is Safe isn’t clear or detailed enough, ask ChatGPT how a brokerage account works. What happens when you buy 100 shares of Nvidia stock in your brokerage account. Who gets the money? Does Nvidia know you own 100 shares? What happens when you buy 100 shares of an S&P 500 mutual fund? Who gets the money and what do they do with it? Does the S&P 500 fund know you own 100 shares? Is it any different when you buy shares in a money market fund? Who gets the money and what do they do with it? Does the money market fund know how many shares you own?

Learningeveryday says

@Thomas martin. Thanks for adding your experience with that days brief shutdown. However what i was asking is whether you could even log into your CMA account on a browser or app that first hour. Was it the same as accessing your fidelity brokerage account. I think the answer is yes? ACH transfers and back end movement could have occur ed during that time or maybe later (the account was inaccessible to me only for an hour.. 930-1020 or so) so hard to read much into that given it was only a brief downtime. What i am getting into is by having ones checking/savings banking with the same provider, are we increasing risks of a brokerage shutdown taking down your banking accessibility. Or maybe some feel that all banks have the same issue of periodic issues. Thank you for sharing your experience. Best

Thomas Martin says

@ Learningeveryday – I guess I misunderstood your concern. No, I could not log in online and see my CMA either. But I have had an instance where Schwab was down for a little while, as well as Chase. If you are super concerned with always being able to see your money online, you would need to have multiple duplicate accounts just in case one of your banks was down for a bit. My point that the lack of me being able to log on had NO effect of the CMA making scheduled transfers and payments stands.

Craig says

For credit card payments you probably want to use ACH pull (i.e. initiated from the credit card issuer) anyway, as recommended by Harry at https://thefinancebuff.com/ach-transfer-push-pull.html#htoc-bill-payments. So you would only need to log in to Fidelity to check your available cash balance.

Pedro says

Fidelity just informed me this is not a typical brokerage account as it’s restrictive on what ETF’s I can buy. I had to open a traditional brokerage on top of the CMA. I’m not sure why Rob Berger is suggesting this is a brokerage account.

Harry Sit says

Both the Fidelity rep and Rob Berger are correct. Fidelity CMA is designed for cash management, which is the subject of this post. It is a brokerage account and you can buy every ETF in it but that doesn’t mean you should do it. It’s a good idea to open a separate regular brokerage account to buy ETFs intended as long-term investments. This creates separation between day-to-day spending and saving and investing for the long-term.

Unmesh says

The article says “You can link the debit card in the Zelle mobile app” but I can’t figure out how to do it. Directions will be greatly appreciated.

Harry Sit says

Download the Zelle mobile app. Register as a new user with a phone number and associate the Fidelity debit card with this user. Each Zelle user profile is linked to only one bank account or debit card. That’s how Zelle knows where to send the money when you receive money through Zelle. If you’re already enrolled in Zelle using the same phone number with another bank, you need a different phone number or you have to contact that bank and have them unenroll you from Zelle to free up that phone number.

Joey says

just curious , if one attempts to sign up for Zelle but the CMA debit is ‘locked’ would it fail?

or lets say signed up successfully but debit card is locked and someone transfers money to my account, does it fail ?

I have never had anyone ask or have a situation where I need to send money remotely, but I can see it could happen.

Unmesh says

I have Zelle only associated with email addresses but I could be wrong and need to check with my banks.

The Zelle app starts out by asking me “Where do you bank?” and Fidelity Brokerage is not an acceptable answer.

Harry Sit says

Tap the “Don’t See Your Bank?” button below the search results. Here’s a YouTube video on using the Zelle app with a debit card:

https://www.youtube.com/watch?v=1LOfTQ03hcc

Unmesh says

Did it, thanks!

Can one accept money through this set up or is it only usable to send money?

Harry Sit says

It should work both ways. Test it first.

TenBlinkers says

I’ve been using Fidelity’s Core account as my checking account for decades. I see no advantages in using their CMA vs the Core account. From day 1 all funds in the Core account are invested in a MM fund, you get a debit card, check book, etc. The only reason I can think of why they created the CMA is marketing. In fact the CMA suffers by comparison, since you have to manage it separately from your core investment account.

Thomas Martin says

Agreed, same here. I actually use 1 core account for checking and “savings” (MMA and T-Bills). I use a second account for investments to have a “firewall” between the account with checks and ACH activity and the account with the big bucks.

Unmesh Agarwala says

I asked my Relationship Manager why some clients had Brokerage and Cash Management accounts and he said it was to keep investments separate from expenditures even though the capabilities of the two were pretty much the same except for margining.

Steve says

I originated an EFT transfer at Fidelity to my new Fidelity CMA from my bank.

Later that same day I received email from Fidelity (below) indicating that I can withdraw within 1-6 business days.

The transferred amount is shown in my CMA balance. Activity display shows status as “Processing”.

Fidelity manage cash page shows the transferred amount as “Unavailable Balance”.

Questions:

1, When a transferred amount is displayed in my CMA balance, does that mean that the funds have been transferred from bank to Fidelity, or is that just a ‘forecast’ of funds to be transferred?

2. How many business days should I normally expect it to take for such a transfer originated on Fidelity to become available balance for withdrawal?

My experience in many years of using EFT to push funds from Fidelity to my bank is that the funds were available for withdrawal at my bank within 1 business day.

I hope I won’t have to wait 3 to 6 days to withdraw funds pulled into Fidelity from other institutions.

Fidelity email received evening of transfer request:

You can now trade your transferred money.

Originally from: My Bank

Now in: Fidelity CMA

How much: $5,000.00

When you can trade: Now

When you can withdraw: Within 1 to 6 business days

Harry Sit says

An ACH pull takes 1-6 business days to become available for withdrawal as the email said. Exactly how many business days depends on the amount pulled and your account history. My pulls are usually available for withdrawal in two business days. If you care about the availability for withdrawal, a pull is the wrong way to transfer money. You should push from your bank to Fidelity. See ACH Push or Pull: The Right Way to Transfer Money. You may have a specific reason to use pull, which is also addressed in that linked post, but then you have to accept the tradeoff of a longer hold time.

Steve says

Harry: Thanks for your reply. I have learned that the funds I pulled from bank to Fidelity have not yet been withdrawn from my bank account. So the $5000 displayed in my Fidelity CMA balance – “processing” – has not yet actually transferred.

Two business days wait to be able to withdraw with EFT pulled funds is ok. Three to six days wait is not. I will soon find out.

RayK says

Learning as a New CMA account holder and confused so have questions while lock down is enabled.

1) Are my traditional IRA and Roth IRA’s in Fidelity that hold MMF’s wall protected (separated) from my new CMAccount?

2)Dumb and confused? Is the CMA set up to be only an after tax checking account and never have auto draft protection mixing before and after tax money?

3) Is it okay if new debit card not activated yet and just might hold off and throw in a safety box?

4) Eventually will I need to open a brokerage account when doing large ira withdrawals?

Sorry, I think I see some of my confusion under my cash management account ($5.00), I also see my retirement ira’s large cash amount available.

Harry Sit says

Your CMA is a separate account from your Traditional IRA and Roth IRA. A debit against the CMA doesn’t pull from your Traditional IRA or Roth IRA. There is a self-funded overdraft protection feature and a minimum target balance feature in Cash Manager but neither feature is enabled by default. If you do enable either feature, it can’t use your Traditional IRA or Roth IRA anyway. The funding account for the self-funded overdraft protection feature or the minimum target balance feature has to be a taxable account. I don’t recommend enabling either feature (see the section “Cash Manager Not Needed”).

If you don’t intend to use the debit card ever, don’t request the debit card, or if you already have the debit card, close it. If you want to keep the option open and maybe use it one day, activate the debit card and lock it. Not activating it isn’t as clean. A never-activated card may be closed by the issuing bank after some time. It defeats the purpose of keeping the card.

If your large IRA withdrawals are for spending, you can withdraw to the CMA. You don’t necessarily need to open a brokerage account when you do large IRA withdrawals.

RayK says

Hope I have not been to much of a doofus, but you have been a blessing for me.

Thank you Harry for all your fantastic help past and present.

RayK says

Hi Harry,

Appreciate your wise opinion on questions below:

1) I am a slow mover, but leaning toward activating my debit cards and lock them as you mentioned. I possibly may use them at a later date, or can choose to cancel them. Do you think this is a reasonable path forward?

2) I also am thinking about opening up a Fidelity Visa credit card, but do have any concerns around (fraud, safety) which bank or banks that may manage this part of Fidelity’s business?

Best Regards.

Steve says

Re your question about Fidelity Visa credit card. I have had Fidelity Visa credit card from US Bank for many years. Have not had any problems or concern about fraud/safety of the card.

I did see a charge that was not authorized. Not sure because it has been long time ago, but I think US Bank may have contacted me about it. At any rate, the improper charge was promptly deleted from my account.

The Fidelity card from US Bank provides email alerts every time a transaction occurs when the card is not physically present (such as for online payment/Amazon, etc.) The alerts let me ensure that such transactions – not matter how large or small – are valid.

These alerts are not available from my other non-Fidelity credit vendors.

Steve O says

We’ve had the Fidelity Rewards Visa Signature card (its current name) for many years, and its our everyday card not only for the unlimited 2% back, but the benefits are quite good (purchase security, car rental discount, travel protections). Also, and this is relatively new, it has no foreign transaction fee. Citi’s Double Cash has a 3% foreign fee for comparison. The Fidelity Rewards Visa Signature is issued by Elan Financial Services, and I’ve only had good experiences with them. A fraud incident we had on vacation was handled as well as expected, with fraudulent charges refunded promptly. We have a Citi Double Cash as a backup, but rarely use it.

RayK says

Thank you for the comments.

I have read some negative comments regarding Elan Financial Services connected to Fidelity Acct.

Part of my thought is wanting to make sure Elan is reputable since I never heard of them?

Art says

I’ve had the fidelity visa with Elan for a number of years. I think it was FIA card before that. I don’t especially like their website ( largely because payments aren’t updated immediately) but I’ve never had any problems with the card. I don’t think I’ve ever had to contact customer service, so can’t speak to that. I hadn’t realized they’ve done away with foreign transaction fees, so that’s another plus. 2% flat cash back is fine — juggling reward quarters is almost never worth the hassle.

Art says

Ps I should add that Fidelity on Reddit does have a number of negative threads about Elan, including a recent scam. I’ve never had a problem, but… I don’t answer my phone if it’s an unknown number and my credit is frozen — best to take precautions regardless of the issuer.

JT says

Elan is owner by the 5th largest U.S. Bank by assets. My one and only CS interaction with Elan was positive.

SF Giants says

Rob Berger recently did a video confirming that his Fidelity CMA account had his check deposit limit reduced to $1,000. He found out about it from a reddit thread. Seems like it may be for newer accounts as mine didn’t change and may be related to the Chase Bank check fraud scandal. While there are workarounds (going to a Fidelity branch or using another bank and pushing to Fidelity), people may want to check to see what their current limit is.

Harry Sit says

My mobile check deposit is still $500,000 per day. I can’t remember the last time I deposited a paper check. I wrote Follow This Rule to Avoid Getting Your Account Restricted for Fraud, which Rob mentioned in his video. You have nothing to worry about if you always make deposits by ACH push.

Tom Martin says

My mobile check limit is also 500K and I do pulls into fidelity all the time including today. I thinks there’s more involved than just if you do pulls. I think it has more to do with check deposits and money movement patterns.

Harry Sit says

Some people are getting long hold times of up to 3 weeks for ACH pulls. Not all pulls get a long hold and not all check deposits trigger a fraud flag but doing ACH pushes avoids the issue altogether.

Unmesh Agarwala says

I just got my checks and there is a notification included that says there need to be sufficient funds in the core account for a check to be honored. Is it not the case that purchased money funds like FDLXX will auto-redeem for this purpose?

Harry Sit says

The balance available to withdraw includes both core and non-core money market funds. Withdrawal methods include internal transfer to another Fidelity account, check, debit card, ACH/EFT, and wire.

Tom Martin says

Yes FDLXX will auto redeem. It’s what I use since I live in CA.

john john says

oct 13 24

one thing I’ve noticed is treasury direct, despite setting the CMA as “default” on TD website, won’t deposit to the CMA, it used my backup bank.

also I have a credit union Visa, and it won’t take the routing/acct numbers to allow autopay, though the Big Bank Visa *does take the autopay setup,

has anyone TD paying out to the CMA directly successfully, maybe I’ve done something not correct ?

Harry Sit says

I redeemed some I Bonds last month at TreasuryDirect and the money came into my Fidelity account just fine. There’s a dropdown for where you want the money to go when you redeem bonds. It’s possible that the accounts are sorted alphabetically and you just didn’t pay close attention to which account was picked in the dropdown.

JT says

My guess is TD only deals with FDIC members.

Fidelity isnt and your CU is probably insured by NCUA instead.

john says

hmm , under TD->Manage Direct-> bank information, there are “radio buttons” to select the bank , (no dropdown, not alphabetical) I have 3 banks I selected fidelity cma (Primary Bank for Purchases and Payments);

but for my Bi-Annual TIPS interest it redeemed it to one of the others, unless a week or two before redemption, this Had been the primary ; there were no test deposits during adding the CMA, and I added it as “checking account”.

there is a phone number listed, however, of course one/myself am unable to edit any of the banks: “As part of our efforts to provide additional security for your investments, you must complete and mail a Bank Change Request FS Form 5512 to edit an existing bank.

You must sign the form in the presence of an authorized certifying official available at a bank, trust company, or credit union and mail it to us for processing. Certification by a Notary Public is not acceptable.

Your request will not be processed until we receive and approve your form with any necessary supporting documentation. We will notify you by e-mail when your transaction has been completed.

If you have questions, please contact us at (844) 284-2676.”

….so I was allowed to add and make a bank default (the CMA) , however TD funds the previous bank only ; wonder what trying to call might acheive if anything .

🙁

JJ says

ok please disregard, I found the drop down menus, they are only for marketable securities, not for savings bonds, fwiw, in my case , I called them they were responsive, I’m finding vs. VG, fidelity may also provide some cont’d CS, as a reason to branch out from VG a bit. 🙂

Harry Sit says

The payment destination for regular Treasuries (including TIPS) in TreasuryDirect was selected at the time of purchase. Apparently you chose the credit union account when you bought the bond. Changing which bank account is primary or default doesn’t affect existing holdings. If you’d like to change which bank account TreasuryDirect uses for payments from an existing marketable security, you can edit the payment destination for that holding under the Current Holdings menu. You’ll have to do it one holding at a time.

A Fidelity CMA works in TreasuryDirect just fine.

Fid Fan says

> You may have seen some convoluted setups using the Cash Manager overdraft feature in the Fidelity CMA. It’s unnecessary and undesirable.

I disagree on this, though the explanation is useful.

You can open as many brokerage accounts as you want, and you can select which accounts you want to include in your autodraft. Because of that, I have the following setup:

1. CMA w/ about 1 month’s normal expenses

2. brokerage account with emergency fund (t-bills) and any excess cash (MMF; usually a few thousand)

3. brokerage account with taxable investments

My paycheck hits account 2, account 2 auto-transfers into account 1, and all regular payments and transfers go out of account 1. Account 3 is not part of the autodraft at all, and account 1 drafts from account 2 if needed. I have a separate debit card and checking for account 3 (I keep it locked), just in case my CMA card is compromised (I could use it as a temporary checking until the fraud is resolved).

If I’m seeing autodrafts, then I know it’s time to review our spending. I also use the max balance as well, so if money piles up (i.e. spending goes down), it goes back into account 2. If I run into fraud, the most I’d lose is my MMF balance in account 2, which is usually a few thousand because my t-bill emergency fund wouldn’t get auto-sold.

This has no impact on total returns or anything, it’s merely a convenience that helps get insight into our cash flow (i.e. there’s no reason to check my balance until I get an alert).

In short, I found the wording here to be a little aggressive. Yeah, there’s not really an optimization angle here in regards to returns, but there are use cases for the cash flow tools.

RayK says

Hi Harry,

Just activated my new Fidelity Visa card and want to ask if I should/should not accept the Elan Electronic Document Consent for access to their website?

By reviewing and accepting the terms, you will be able to review your account digitally and we can process any service requests you make online.

I am slowly and almost fully on board with this CMA and Visa Card.

Thanks in advance.

RayK says

Hi All,

Is there any new Fidelity Visa card holders out there who are familiar with Elan Bank??

Harry Sit says

Elan is a division of U.S. Bank, which is the fifth largest bank in the country. The Fidelity Visa credit card is a product of Elan. Fidelity has little to do with it, except being paid by Elan to market the card and providing limited technology integration to show transactions, make payments, and receive cashback rewards. Your relationship with regard to this credit card is with Elan. You should create a login with Elan and accept its terms. See The Anatomy of a Co-Branded Credit Card for more on how a co-branded credit card works in general.