[The next update will be on August 12, 2026, when the government publishes the CPI data for July 2026.]

Seniors 65 or older can sign up for Medicare. The government refers to people who receive Medicare as “beneficiaries.” Medicare beneficiaries must pay a premium for Medicare Part B, which covers doctors’ services, and Medicare Part D, which covers prescription drugs. The premiums paid by Medicare beneficiaries cover about 25% of the program costs for Part B and Part D. The government pays the remaining 75%.

What Is IRMAA?

Medicare imposes surcharges on higher-income beneficiaries. The theory is that higher-income beneficiaries can afford to pay more for their healthcare. Instead of doing a 25:75 split with the government, they must pay a higher share of the program costs.

The surcharge is called IRMAA, which stands for Income-Related Monthly Adjustment Amount. This applies to both Traditional Medicare (Part B and Part D) and Medicare Advantage plans.

According to a Medicare Trustees Report, less than 10% of Medicare Part B beneficiaries paid IRMAA. The extra premiums they paid reduced the government’s share of the total Part B and Part D expenses by two percentage points. Big deal?

History of IRMAA

IRMAA was added to Medicare by the Medicare Prescription Drug, Improvement, and Modernization Act of 2003. The Republican Congress under President George W. Bush passed it in November 2003.

IRMAA started with only Part B. The Patient Protection and Affordable Care Act, passed in 2010 by the Democratic Congress under President Obama, expanded IRMAA to also include Part D.

The Bipartisan Budget Act of 2018, passed by the Republican Congress under President Trump, added a new tier for people with the highest incomes.

IRMAA has been the law of the land for over 20 years. Different congresses and administrations from different parties made small tweaks, but its structure hasn’t changed much since the beginning. IRMAA has become a bipartisan consensus. There’s no impetus for major changes.

MAGI

The income used to determine IRMAA is your Modified Adjusted Gross Income (MAGI) — which is your AGI plus tax-exempt interest and dividends from muni bonds — from two years ago. Your 2024 MAGI determines your IRMAA in 2026. Your 2025 MAGI determines your IRMAA in 2027. Your 2026 MAGI determines your IRMAA in 2028.

There are many definitions of MAGI for different purposes. The MAGI for ACA health insurance subsidies includes 100% of the Social Security benefits. The MAGI for IRMAA includes taxable Social Security benefits, but not untaxed Social Security benefits. If you read somewhere else that says that untaxed Social Security benefits are included in MAGI, they’re talking about a different MAGI, not the MAGI for IRMAA.

You can use Calculator: How Much of My Social Security Benefits Is Taxable? to calculate the taxable portion of your Social Security benefits. The new 2025 Trump tax law didn’t change how Social Security is taxed. It didn’t change anything related to the MAGI for IRMAA. See Social Security Is Still Taxed Under the New 2025 Trump Tax Law.

As if it’s not complicated enough, while not moving the needle much, IRMAA is divided into five income brackets. Depending on the income, higher-income beneficiaries pay 35%, 50%, 65%, 80%, or 85% of the program costs instead of 25%. As a result, they pay 1.4, 2.0, 2.6, 3.2, or 3.4 times the standard Medicare premium.

The threshold for each bracket can cause a sudden increase in the monthly premium amount you pay. If your income crosses into the next bracket by $1, your Medicare premiums can suddenly jump by over $1,000 per year. If you are married and filing a joint tax return, and both of you are on Medicare, $1 more in income can make Medicare premiums jump by over $1,000/year for each of you.

* The last bracket on the far right isn’t displayed in the chart.

If your income is near a bracket cutoff, try to keep it low and stay in a lower bracket. Using the income from two years ago makes it more difficult to manage.

2026 IRMAA Brackets

The standard Part B premium in 2026 is $202.90 per person per month. The income on your 2024 federal tax return (filed in 2025) determines the IRMAA you pay in 2026.

| Part B Premium | 2026 Coverage (2024 Income) |

|---|---|

| Standard | Single: <= $109,000 Married Filing Jointly: <= $218,000 Married Filing Separately <= $109,000 |

| 1.4x Standard | Single: <= $137,000 Married Filing Jointly: <= $274,000 |

| 2.0x Standard | Single: <= $171,000 Married Filing Jointly: <= $342,000 |

| 2.6x Standard | Single: <= $205,000 Married Filing Jointly: <= $410,000 |

| 3.2x Standard | Single: < $500,000 Married Filing Jointly: < $750,000 Married Filing Separately < $391,000 |

| 3.4x Standard | Single: >= $500,000 Married Filing Jointly: >= $750,000 Married Filing Separately >= $391,000 |

Source: CMS news release

Higher-income Medicare beneficiaries also pay a surcharge for Part D. The IRMAA income brackets are the same for Part B and Part D. The Part D IRMAA surcharges are relatively lower in dollars.

I also have the tax brackets for 2026. Please read 2026 Tax Brackets, Standard Deduction, Capital Gains, QCD if you’re interested.

2027 IRMAA Brackets

We have nine data points right now out of the 11 needed for the IRMAA brackets in 2027 (based on 2025 income).

If annualized inflation from July through August 2026 is 0% (prices staying flat at the latest level) or 3% (approximately a 0.25% increase every month), these will be the 2027 numbers:

| Part B Premium | 2027 Coverage (2025 Income) 0% Inflation | 2027 Coverage (2025 Income) 3% Inflation |

|---|---|---|

| Standard | Single: <= $112,000 Married Filing Jointly: <= $224,000 Married Filing Separately <= $112,000 | Single: <= $112,000 Married Filing Jointly: <= $224,000 Married Filing Separately <= $112,000 |

| 1.4x Standard | Single: <= $141,000 Married Filing Jointly: <= $282,000 | Single: <= $141,000* or $142,000 Married Filing Jointly: <= $282,000* or $284,000 |

| 2.0x Standard | Single: <= $176,000 Married Filing Jointly: <= $352,000 | Single: <= $176,000* or $177,000 Married Filing Jointly: <= $352,000* or $354,000 |

| 2.6x Standard | Single: <= $211,000* or $212,000 Married Filing Jointly: <= $422,000* or $424,000 | Single: <= $211,000* or $212,000 Married Filing Jointly: <= $422,000* or $424,000 |

| 3.2x Standard | Single: < $500,000 Married Filing Jointly: < $750,000 Married Filing Separately < $388,000 | Single: < $500,000 Married Filing Jointly: < $750,000 Married Filing Separately < $388,000 |

| 3.4x Standard | Single: >= $500,000 Married Filing Jointly: >= $750,000 Married Filing Separately >= $388,000 | Single: >= $500,000 Married Filing Jointly: >= $750,000 Married Filing Separately >= $388,000 |

Some of the projected 2027 brackets are the same for 0% inflation and 3% inflation due to rounding. The unrounded numbers for 3% inflation are higher, but not high enough to break into the next level after rounding.

If you’re married filing separately, you may have noticed that the 3.2x bracket goes down with inflation. That’s not a typo. If you look up the history of that bracket (under heading C), you’ll see it went down from one year to the next. That’s the law. It puts more people married filing separately with a high income into the 3.4x bracket.

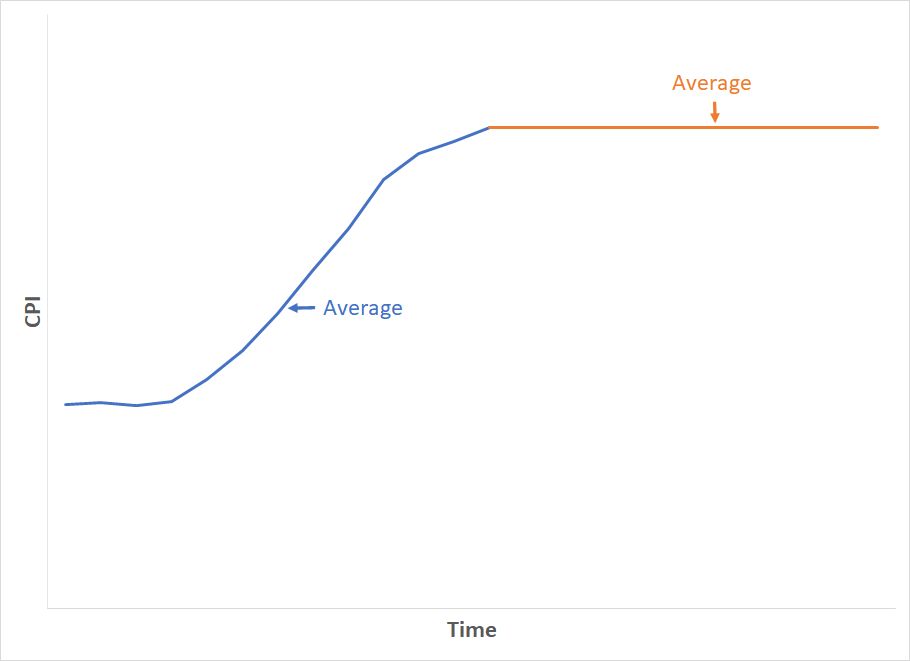

Because the formula compares the average of 12 monthly CPI numbers over the average of 12 monthly CPI numbers in a base period, even if prices stay the same in the following months, the average of the next 12 months will still be higher than the average in the previous 12 months.

To use exaggerated numbers, suppose gas prices went up from $3/gallon to $3.50/gallon over the last 12 months. The average gas price in the last 12 months was maybe $3.20/gallon. When gas price inflation becomes 0%, it means it stays at the current price of $3.50/gallon. The average for the next 12 months is $3.50/gallon. Brackets based on an average gas price of $3.50/gallon in the next 12 months will be higher than brackets based on an average gas price of $3.20/gallon in the previous 12 months.

If you really want to get into the weeds of the methodology for these calculations, please read this reply on comment page 2 and this other comment on page 4.

The Missing October 2025 CPI

The government did not and will not publish the CPI number for October 2025 because it didn’t collect the necessary price data during a government shutdown. It’s unclear how the Social Security Administration will calculate the 12-month average with only 11 data points.

The Treasury Department used 325.604 as the October CPI to calculate interest on inflation-indexed Treasury bonds. The Social Security Administration won’t necessarily use the same number for IRMAA. I calculated the projected 2027 brackets in two ways: (a) using a straight average of the projected 11 monthly data points, omitting October 2025; and (b) using 325.604 for October 2025. The projected 2027 brackets are largely the same under the two methods due to rounding. I put an asterisk on the number calculated by method (b) where they differ.

2028 IRMAA Brackets

We have no data point right now out of the 12 needed for the IRMAA brackets in 2028 (based on 2026 income). We can only make preliminary estimates and plan for some margin to stay clear of the cutoff points.

If annualized inflation from July 2026 through August 2027 is 0% (prices staying flat at the latest level) or 3% (approximately a 0.25% increase every month), these will be the 2028 numbers:

| Part B Premium | 2028 Coverage (2026 Income) 0% Inflation | 2028 Coverage (2026 Income) 3% Inflation |

|---|---|---|

| Standard | Single: <= $114,000 Married Filing Jointly: <= $228,000 Married Filing Separately <= $114,000 | Single: <= $116,000 Married Filing Jointly: <= $232,000 Married Filing Separately <= $116,000 |

| 1.4x Standard | Single: <= $143,000 Married Filing Jointly: <= $286,000 | Single: <= $146,000 Married Filing Jointly: <= $292,000 |

| 2.0x Standard | Single: <= $179,000 Married Filing Jointly: <= $358,000 | Single: <= $183,000 Married Filing Jointly: <= $366,000 |

| 2.6x Standard | Single: <= $214,000 Married Filing Jointly: <= $428,000 | Single: <= $219,000 Married Filing Jointly: <= $438,000 |

| 3.2x Standard | Single: < $507,000 Married Filing Jointly: < $760,500 Married Filing Separately < $393,000 | Single: < $517,000 Married Filing Jointly: < $775,500 Married Filing Separately < $401,000 |

| 3.4x Standard | Single: >= $507,000 Married Filing Jointly: >= $760,500 Married Filing Separately >= $393,000 | Single: >= $517,000 Married Filing Jointly: >= $775,500 Married Filing Separately >= $401,000 |

Effect of the Iran War

The CPI numbers in recent months were affected by the volatile energy prices due to the Iran war. The most recent data point reflects the market’s hope that the war would end following a ceasefire and a preliminary deal. The 0% inflation numbers assume that prices will stay at the current level. Energy prices can rise sharply if the war drags on. If that happens, CPI numbers in the upcoming months can escalate beyond the 3% inflation estimate, which may push the IRMAA numbers above the projections.

Roth Conversion Tools

When you manage your income by doing Roth conversions, you must watch your MAGI carefully to avoid accidentally crossing one of these IRMAA thresholds by a small amount and triggering higher Medicare premiums.

I use two tools to help with calculating how much to convert to Roth. I wrote about these tools in Roth Conversion with TurboTax What-If Worksheet and Roth Conversion with Social Security and Medicare IRMAA.

Nickel and Dime

The standard Medicare Part B premium is $202.90/month in 2026. A 40% surcharge on the Medicare Part B premium is $974/year per person or $1,948/year for a married couple both on Medicare.

In the grand scheme, when a couple on Medicare has over $218,000 in income, they’re already paying a large amount in taxes. Does making them pay another $2,000 make that much difference? It’s less than 1% of their income, but nickel-and-diming just makes people mad. People caught by surprise when their income crosses into a higher bracket by just a small amount are angry at the government. Rolling it all into the income tax would be much more effective.

Oh well, if you are on Medicare, watch your income and don’t accidentally cross a line for IRMAA.

IRMAA Appeal

If your income two years ago was higher because you were working at that time, and now your income is significantly lower because you retired (“work reduction” or “work stoppage”), you can appeal the IRMAA initial determination. The “life-changing events” that make you eligible for an appeal include:

- Death of spouse

- Marriage

- Divorce or annulment

- Work reduction

- Work stoppage

- Loss of income from income producing property

- Loss or reduction of certain kinds of pension income

You file an appeal with the Social Security Administration by filling out Form SSA-44 to show that although your income was higher two years ago, you have a reduced income now due to one of the life-changing events above. For more information on the appeal, see Medicare Part B Premium Appeals.

Not Penalized For Life

If your income two years ago was higher and you don’t have a life-changing event that makes you qualify for an appeal, you will pay the higher Medicare premiums for one year. The IRMAA surcharge goes into the Medicare budget. It helps to keep Medicare going for other seniors on Medicare.

IRMAA is re-evaluated every year as your income changes. If your higher income two years ago was due to a one-time event, such as realizing capital gains or taking a large withdrawal from your IRA, your IRMAA will decrease automatically when your income comes down in the following year. It’s not the end of the world to pay IRMAA for one year.

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.

The Wizard says

Doing Roth conversions early in the year gets the money out of tax-deferred sooner and allows growth for the rest of the year to happen in your Roth, assuming same investments.

Problem for me at age 75 is that I want to avoid having my AGI get me into the next higher IRMAA tier. So I do my annual Roth conversion in December after I have a good estimate of all my other income…

Mike W says

Jeff,

Some philosophy mixed with opinion.

Barring other reasons to convert at the beginning of the year, or end, or monthly, I think statistically the market will go up in any given year. My rationale is that we are at new highs right now and that means that anyone who invested at any time in the past 50 years made money. It does not matter how much, only that the prior 49 years were good years to invest in if you are alive today.

The next question to ask is which month or quarter is the best to invest in and my opinion is that it may be slightly better to buy in May (because some pundits say to sell in May so there may be a slight statistical effect that increases the chances of buying in a buyer’s market).

Since 1960, so my research with AI bots tells me, there have been more up markets than down. Many more. So to save a lot of time and work, any year you decide to invest in has a good chance of being an up year. Some may not but look at those down years. Like a year in which a bear market went down 30%. On average it has taken 2 1/2 years to recover from a bear market and in the 31st month after you are at a new high for you, and you are an example of why buy and hold has worked out.

I am bullish on the United States. I have never sold in a bear market. And today I’m paying for that bullheadedness by having no way to avoid increasingly higher IIRMA’s. Though that also means I have no worry about having to eat cat food.

All the rest is trying to find tweaks to increase your gains from, lets say 18% annually, to 19%, or whatever number you have achieved so far.

For me personally I invest when my cash on hand exceeds the level of cash I want to have available to buy good stocks that have had a bad time.

Lynne says

I’d love to do Roth conversions at the beginning of the year but don’t know what my financial situation will be until near the end of year. Hopefully in future years it’s not so unpredictable so I can do at least some of it in January, then do the remainder near year’s end. In the past few years, the market has increased so much that with conversions I’m somewhat treading water where the pretax funds are at least not getting higher than the year before, in spite of conversions. No doubt this will change soon.

Robin says

We do our Roth IRA conversions once or twice a month all year long, dripping out in the same way we dripped into the 401ks. We convert the equivalent of $1500-2000 in shares for each of us, saving the last 25-30% of the total annual conversion to do on the last business day of the year. That way we get the advantage of growth in the Roth IRA, and yet don’t go over the IRMAA cliff. This year, with the market down, we’re having to hold ourselves back from doing more sooner!

Bev L says

Lou –

I feel your pain. Calculating income brackets for IRMAA is a nightmare. The system is convoluted. One never knows the true tier number until one year hence. And while I am expressing frustration, Social Security has already been taxed once and paid to the government. Since 1993, 85% of SS can be included in income. It is retaxed along with the additional social security revenue source of IRMAA penalties (uh, they call it an adjustment), basically another tax on social security. A 2.9% Medicare tax on earned wages is shared by the employee and employer on all wages. There is no wage limit for this Medicare tax.

We have lived frugally and tried to save wisely. Our income is from social security and investments. The investment piece could be gone tomorrow. Initially, Social Security was funded with 1% from the employee and 1% from the employer on income up to $3000. In my view, Social Security has been mismanaged along with federal budget.

Ken says

Imagine what your SS income would be today if it were still based on 1%-employee/1%-employer up to $3000.

Mike W says

I don’t have a problem with increases in taxes. Costs rise because we want and need improvements in products, or we want new products. Imagine living in the years before there were ways to deal with Glaucoma, clogged arteries, cataracts, etc. People just went blind or died. But, what I object to is cutoff points for tax deductions or any other trigger points that are not adjusted for inflation. Our governments know that it is dishonest and sneaky robbery but they still allow it when they write new laws as well as allow old laws to exist. There is no excuse, absolutely none, to have any fixed trigger level that does not adjust to inflation. It is not OK to say that you can deduct up to $3,000 in loss carryover situations and leave that stay in effect for 30 years. That’s just an example. When I started working hitting a salary of $10,000 was an accomplishment. Today its $100,000 and more. My first apartment in New York City was $150 a month. I don’t know what it is now but I’m sure it’s over $1000. But for years on end my loss carry over has stayed at $3,000 and the calculation for when 85% of my Social Security is taxed has never changed either.

Gary says

Mike, I am with you on the need to inflation-index all provisions of the tax code. I do have moments of frustration and stress in things like estimating my yearly income and IRMAA brackets. However, I may be one of the lucky ones who is living a fairly easy retirement and should not worry about every dollar (or thousand dollar of costs). Wonder what Rockefeller would have paid to live my life today?

My secret is that I love working with spreadsheets, so it is a kind of a game to optimize my net worth this year and the next 27 (he says hopefully at age 73).

The ones I feel sorry for are less fortunate folks, for which this is not a game, but food on the table and heat in the house.

Mike W says

Gary, when I look at the income distribution stats and the estimated average Joe’s IRA balance I am reminded how fortunate I am and cannot understand how 50% of the population can look forward to an easy retirement.

As for 73 just keep fit and calm. I celebrate 85 in March and the divisor then will be 16. And when I reach 110 (I tell my wife I want to celebrate her 100th with her. We’re 10 years apart.) it will be 6.4. The really good thing about a 6.4 divisor is it signals that pretty soon my RMD will be zero. There’s always a silver lining.

My spreadsheets do run out to 2051. It’s my way of keeping a positive mental attitude.

The Wizard says

I’m just glad that I’m a wealthy bastard at age 75.

My QCDs for this year will be roughly double what they were for 2025, so that’s good…

Gary says

Just keep in mind to reflect in your spreadsheets the possibly for assisted living or nursing home costs. They are tax deductible (over 7.5% AGI threshold), so your RMDs might have a big offset. If you are still healthy, you can pay more tax but are still ahead of the game by keeping the rest of your RMD. 😀

Bev L says

Just wondering if the IRMAA subsidy paid is deductible under medical costs when itemizing rather than taking a standard deduction?

Mike W says

They are considered a premium payment so yes as long as you meet the normal requirements for deducting, like over 7.5% of AGI etc. Just query your friendly AI.

LiftLock says

IRMAA surcharges can be claimed as an itemized deduction on IRS Form 1040 Schedule A for medical expenses that exceed 7.5% of AGI. However, a reduction in a taxpayer’s taxable income only occurs for the amount of itemized deductions of all types that are in excess of the taxpayers standard deduction.

BobbyW says

Thanks for providing the IRMAA estimates and the explinations in the comments about how increases are calculated. Using this information, I created a spreadsheet so I could make estiamtes on different inflation projections. All worked fine until the October 2025 gap. After that, the CPI numbers are lower than the September values. I don’t understand this. Can you explain some details on how the projections are calculated with the numbers for November and December being lower? I am using https://www.bls.gov/regions/mid-atlantic/data/consumerpriceindexhistorical_us_table.htm .

Jeff Enders says

BobbyW – without seeing your spreadsheet, hard to respond.

CPI numbers being lower than than prior month just means month over month there was in month deflation. But year over year, CPI is up 2.7% (324.054 / 315.605) which doesn’t matter much for IRMAA calculations since IRMAA is based on average of one year divided by average for the prior year – see Harry’s explanation at the top of this page.

Tom P says

Jeff, IRMAA is not “based on average of one year divided by average for the prior year.” It’s based on the average of the current Sep-Aug numbers divided by the base Sep-Aug 2017-2018 CPI-U average (249.280), then all the single income brackets are adjusted from the base year brackets using this muliplier.

Lou says

The CPI 0.3% month-to-month increase in Dec 2025 was seasonally adjusted but the index as Bobby said was actually lower than what was reported in Nov 2025. Since IRMAA doesn’t use seasonally adjusted numbers (is that correct?). there was actually month-to-month deflation in December, which will keep the 2027 MAGI thresholds artificially lower than they should be. This govt manipulation of the numbers is outrageous and screwing people who have to contend with IRMMA.

Jeff Enders says

Tom P – are we getting too technical? what i wrote was the shorthand way of stating it and aligns with my suggestion to read Harry’s detailed explanation where he includes the impact of averages in a year over year analysis of how this works. “one year” can begin on any day and end 365 (or 366) days later; it does not necessarily define a Jan 1 – Dec 31 period. A year” is the time it takes for the earth to orbit the sun, regardless of the date the measurement begins. Can we all get some sleep?

Bill says

I see that the estimated 2027 IRMAA with 0 percent inflation for Married Filing Jointly: <= $222,000 but estimated 2028 IRMAA with 0 percent inflation for Married Filing Jointly: <= $220,000.

Question: I know there are no data points for 2028 IRMAA estimate, but why is it lower than the 2027 estimate?

Harry Sit says

There’s a short explanation immediately below the 2028 table.

Rob I says

There is some historical seasonality with the raw CPI number dropping in November and/or December looking back over the last few years of data. This is not the case for the annual change as it averages out in the year to year comparisons.

https://www.bls.gov/regions/mid-atlantic/data/consumerpriceindexhistorical_us_table.htm

Vince says

Next year we will have to start RMDs and we will probably be over the $220k. Hopefully young people examine the benefits of Roth investments. Seems like government statistics

have always been a little inaccurate the past few decades so maybe we will improve our

inflation calculations for IRMAA going forward and fewer people will be affected.

Lynne says

A few years ago I realized my RMDs plus SS were going to push me dangerously close to IRMAA threshold, so I started a plan of annual Roth conversions. I’ve done 2 thus far.

The crazy part is that the conversions have just allowed me to basically tread water with regard to total pretax savings, thanks to generous market returns. But I’d be in much worse shape had I not done this, so no regrets. Obviously, a conversion in a down market would pay off even more since the recovery would be in the Roth, not the taxable account.

Richard says

Your 2027 standard numbers make no sense. They are the same for 0% and 3% inflation.

Jeff Enders says

Richard – with an understanding of the mechanics, it makes perfect sense.

Using the standard single number of $111,000, this number is rounded to the nearest thousand as prescribed by the law.

At an expected inflation rate of zero, the unrounded forecasted number would be $110,522 which rounds to $111,000.

At an expected inflation rate of 3%, the unrounded forecasted number would be $111,421, which also rounds to $111,000.

the two unrounded numbers will continue to converge as the measured year progresses.

now does it make sense?

Mike Kurz says

I see the 2 differences in IRMAA for 0% and 3%. Is there a chart for the case if inflation is2%? I can see that it most likely wouldn’t be zero, but what if it is 2.2%? Or is it zero or 3 and that’s it?

Mike

Jeff Enders says

Mike – what is your objective and for what year? the 0% projection and the 3% projection will continue to converge as the measured year plays out. for 2027, there is not much you can do with the information since your 2025 MAGI is effectively “locked in”. For 2028, as long as inflation exceeds 0% and doesn’t exceed 3%, a 2.2% estimate would be somewhere between the already narrow 0% projection and 3% projection.

Mike Kurz says

I didn’t ask my question correctly. I am looking at the 2028 estimates (so this years income) and for my situation I need to be below $278,000 or $288,000, depending on 0% or 3% inflation. My question is, if inflation is 1.5%, does the bracket go to $283,000? Or is it either 278,000 or 288,000? Another way to ask is if inflation is 0%, the bracket is $278,000. If inflation is 0.1% or 2.9%, what is the bracket?

Mike

Harry Sit says

It will be somewhere in between if inflation is 1.5%, but only in $2,000 increments for married filing jointly. It won’t be $283,000, but can be $282,000 or $284,000.

Mike Kurz says

Thanks, that is exactly what I was asking. I guess if inflation is between 0% and .75% it goes up to $280,000, and so on, something like that. I would say the chance of 0% inflation is very low, and I’m pretty sure my number will be closer to $288,000, especially since January, 2026 inflation was 2.6%, and they are predicting 3.1% for the year. That for the clarification

GeezerGeek says

I created a CSV file to import the 2026 CPI release dates into my Google calendar. If you want the release dates on your Google calendar, paste the following into a text file and give it a CSV file extension. You can then import it in the Google calendar settings.

Subject,Start date,Start time,End date,End time,All Day Event,Description,Location,Private

CPI Announcement,02-13-2026,7:30 AM,02-13-2026,7:30 AM,FALSE,CPI For Jan-2026 ,,TRUE

CPI Announcement,03-11-2026,7:30 AM,03-11-2026,7:30 AM,FALSE,CPI For Feb-2026 ,,TRUE

CPI Announcement,04-10-2026,7:30 AM,04-10-2026,7:30 AM,FALSE,CPI For Mar-2026 ,,TRUE

CPI Announcement,05-12-2026,7:30 AM,05-12-2026,7:30 AM,FALSE,CPI For Apr-2026 ,,TRUE

CPI Announcement,06-10-2026,7:30 AM,06-10-2026,7:30 AM,FALSE,CPI For May-2026 ,,TRUE

CPI Announcement,07-14-2026,7:30 AM,07-14-2026,7:30 AM,FALSE,CPI For Jun-2026 ,,TRUE

CPI Announcement,08-12-2026,7:30 AM,08-12-2026,7:30 AM,FALSE,CPI For Jul-2026 ,,TRUE

CPI Announcement,09-11-2026,7:30 AM,09-11-2026,7:30 AM,FALSE,CPI For Aug-2026 ,,TRUE

CPI Announcement,10-14-2026,7:30 AM,10-14-2026,7:30 AM,FALSE,CPI For Sep-2026 ,,TRUE

CPI Announcement,11-10-2026,7:30 AM,11-10-2026,7:30 AM,FALSE,CPI For Oct-2026 ,,TRUE

CPI Announcement,12-10-2026,7:30 AM,12-10-2026,7:30 AM,FALSE,CPI For Nov-2026 Last for 2026 tax estimate,,TRUE

Tom P says

Or if you don’t use a calendar, you can just go to https://www.bls.gov/schedule/news_release/cpi.htm to see the release dates, which can be copied and pasted into an Excel file, etc. for tracking. You can also subscribe to email alerts on the top right so you’ll get an email the morning the new cpi is released.

Mike Kurz says

OK, so now to clarify something else: My 2026 MAGI will be used to determine if I am above or below $278,000 (or $288,000, depending on the inflation numbers) for my Medicare premium in 2028. Am I reading it correctly when it says the CPI numbers for each month, beginning September of 2026 and ending August of 2027 will determine what the inflation rate was, and will be announced in November of 2027? So I really won’t know until November of 2027 if the bracket is $278,000 or $288,000 for Medicare premium in 2028?

Jeff Enders says

Mike – your understanding is correct. You are “locked in” to your MAGI in December 2026, but won’t know with certainly what the bracket will be until August, 2027. that is why this site exists!

The best you can do is manage your MAGI (think Roth conversions) in December, 2026…. at that point, there are only 8 datapoints left to fill in; currently, there are 20!

The bookends that Harry quotes will continue to converge until they meet no later than August, 2027. You’ll note that the range has now tightened to $280,000 – $288,000, so if the inflation rate continues to stay within 3%, the final number in August, 2027 will be somewhere between $280,000 and $288,000.

Becky Mc says

If someone is widowed and does not experience a reduction in income, what happens? Example: mfj income 2026 below the IRMMA MFJ threshold. Spouse dies 2027. Income stays the same. 2028 tax return looks at 2026 income, two year look back, right? Taxpayer files as single but the 2 year lookback is from 2026 so NOW the threshold is as a single person, so the widow is likely to hit Irmma surcharges? it makes sense because that’s how tax rates work but that is not a two-year look back. But if that’s how it works, it also makes doing Roth conversions impossible to factor in because who knows when you might be widowed.

The Wizard says

You might get a one year free pass via SSA-44.

But after that, you’ll be treated as all other single people are…

LIftLock says

Becky Mc,

This widow penalty is a reason to consider doing Roth IRA conversions before the death of a spouse to avoid the potentially higher taxes generally paid by single taxpayers with the same income as married taxpayers who file jointly. It is often that case that the only reduction in a widow’s income will be limited to the loss of Social Security Income of the lower earning spouse. When I look at my own situation, the last to die spouse to is likely to experience a multiple bracket increase in IRMAA along with a 20% increase in income tax. The only consolation is that IRMAA will only be paid by one spouse. An interesting exercise for married couples is to calculate what taxes will be for the surviving spouse.

Nancy Memmel says

Also, you cannot file an appeal unless you first have been assessed IRMAA charges, so if you fall under the threshold based on your 2 year ago MAGI there really is nothing you can do.

Nancy Memmel says

If you aren’t filing for an appeal based on “death of spouse ” you will continue to be assessed IRMAA based upon your 2-years ago return, so it should take 2 years for you to be assessed as a single, since the SSA knows what the IRS forwards on to them, and that would be your MFJ returns.

Jim M says

You can build a spreadsheet and/or use financial planning software (I recently started using Boldin) to get a good estimate on current year income. Start with your tax data from last year, inputting the info into rows for interest, dividends, LTCG, SS, pensions, Roth conversions, RMDs, rental income, etc. You can also build sections for calculating estimated income taxes, and for IRMMA taxes based on this website’s projections. Once satisfied with the data, plan to do 75-80% of your conversions early in the year and especially if a dip occurs (like occurred in April, ’25 and temporarily yesterday). You can easily obtain YTD interest and dividends from your brokerage account in December and estimate what isn’t shown that will hit before year end. You should also be able to obtain in mid-December any LTCG from mutual funds you may own. The spreadsheet can provide you with a good idea of you expected AGI. Knowing what tax / IRMMA bracket you wish to avoid, you can make a final conversion in mid/late December. I leave a $5K cushion in case of a miscalculation.

If you do build a spreadsheet, you can also factor in social security colas as well as income tax and IRMMA brackets creep using average percentages of increase. While rough, doing so works very well for projections.

In my situation, I’ve found that I will save considerably in overall lifetime taxes, both income and IRMMA, by converting into the 2.6x IRMMA bracket. Paying a bit more today is saving me quite a bit overall.

Irmaa Dodger says

Harry, I see in the 2028 Coverage IRMAA table that the Single income breakpoints for the 3.2x and 3.4x have exceeded $500,000. It seemed that these were “fixed” at $500,000 for many previous years. I’m not close to this income, but I’m just curious about whether the law changed to push these brackets up.

Thanks very much for making these projections! I haven’t seen them anywhere else.

Harry Sit says

A law froze that limit for some years. The freeze is scheduled to end. It will start adjusting in 2028.

lzee says

Harry, does the rule/law change in 2028 affect the other Income breakpoints as well? I’m seeing variation in the 3.2x Standard at the 3.0% inflation rate (as well as the 3.4x Standard breakpoint). Could you reference a URL for the rule/law change?

Harry Sit says

It doesn’t affect the other brackets. The History of IRMAA section links to Bipartisan Budget Act of 2018. That law added the highest bracket and made it start adjusting in 2028.

TIm O. says

The 2.0x Standard for MFJ on the 2027 IRMAA Brackets shows $350,000 maximum MAGI for both the 0% and the 3% inflation assumptions. Is that correct? Usually the 3% inflation MAGI is higher than the 0% inflation MAGI. Thank you for this great resource.

Jeff Enders says

Tim O. – it’s correct – it’s a function of the rounding requirements. The 3% forecast is higher than the 0% forecast.

The 0% and 3% forecasted numbers (unrounded) are currently $174,573 and $175,412, respectively. These two numbers will continue to converge as we get closer to the August reporting.

These two numbers are rounded to the nearest $1,000 and then doubled to achieve the the Joint estimate that Harry publishes. Hence, they are both currently at $350,000.

Jason Hanson says

The 1.4x Standard Premium for Married Filing Jointly in the 2027 IRMAA Brackets reflects $280,000 and $282,000 maximum MAGI for the 0% and 3% inflation assumptions, respectively. On what current unrounded forecasted numbers are these dollar amounts based?

Secondly, if there was zero inflation from March through August, is it correct to assume that the $280,000 figure would remain?

Thanks.

Jeff Enders says

Jason – the unrounded forecasted numbers are currently $139,920 (0%) and $140,593 (3%). Both number are rounded to the nearest $1,000 and then doubled for the Joint results of $280,000 and $282,000, respectively.

The two unrounded numbers will continue to converge over the coming months as the actuals become known. Assuming inflation exceeds 0% but does not exceed 3%, the $139,920 will increase and the $140,593 will decrease and eventually meet.

Yes, if inflation was zero from now until August, the 2027 number would be $280,000.

Ed Humphrey says

Someone above talked about making monthly Roth conversions while taking RMDs. IRS rules that I read about on Ed Slott’s website indicated that FULL RMD must be taken before any Roth conversions are allowed [ https://irahelp.com/new-rule-all-ira-rmds-must-be-satisfied-prior-to-doing-a-roth-conversion/ ]. Further I noted somewhere that QCDs must be taken BEFORE completing RMDs.

I’m not sure how that can be checked since 1099-R reporting to IRS isn’t time-phased, but would not want to be in violation.

Harry Sit says

There are two general rules around RMD, QCD, and Roth conversions. All other rules you hear about are applications of these two general rules:

(1) When you’re subject to the RMD, all distributions during a year count toward the RMD first.

(2) RMD can’t be converted to Roth.

Suppose your RMD this year is $50,000. You take $5,000. That counts toward the RMD (Rule #1). It can’t be converted to Roth (Rule #2). Then you do $20,000 QCD. It also counts toward the RMD (Rule #1). Now you take another $25,000. It counts toward the RMD (Rule #1). It can’t be converted to Roth (Rule #2). Now your RMD is satisfied. You can do additional QCD or Roth conversion.

Therefore, you can do QCD at any time. It counts toward the RMD before you’re done with the RMD. Post-RMD QCD still isn’t taxable (up to the maximum allowed QCD). You do QCDs before satisfying the RMD only when you want to minimize distributions. Some people need or want to withdraw more than the RMD for living expenses. Suppose your RMD is $50,000 and you want $80,000 for living expenses and $10,000 for QCD. It doesn’t matter whether you do QCD before or after you satisfy the RMD. If you do it before, you have $10,000 QCD, $40,000 RMD, and $40,000 additional withdrawal for living expenses. You’re taxed on $80,000. If you do it after, you have $50,000 RMD, $10,000 QCD, and $30,000 additional withdrawal for living expenses. Either way, $90,000 comes out of your IRA and you’re taxed on $80,000.

It makes a difference only when you don’t need money from the IRA for living expenses. In the above example, you’ll have $40,000 RMD if you make QCD count toward RMD or $50,000 RMD if you do it after, but then you’re short $10,000 for living expenses, and that $10,000 has to come from somewhere else.

LiftLock says

Ed Humphrey,

I believe QCDs can be taken before or after RMDs are taken. But QCDs would need to be taken before the RMD is completed if the taxpayer wants the QCD to count as satisfying part their RMD and limit their IRA distribution to the RMD amount.

I have often wondered whether the IRS cares whether the RMD is taken before or after a Roth Conversion is made, as long a the RMD is taken and the RMD amount is not converted to a Roth IRA. The last time I checked, I could not find any language in IRS Publication 590 that addressed the sequence, even though I am told there is language somewhere in the tax code about it. An IRS audit of taxpayer or an IRA custodian might be the one way the IRS might learn about the sequence.

The Wizard says

Most times, the IRS isn’t going to know or care if you do a Roth conversion before completing your RMD. But technically, that’s the rule.

At age 76, I have RMDs from both my 403(b) and my tIRA. I take the former quarterly and the latter I do QCDs from.

It works for me…

Ken says

My only IRA and the Roth I later started with my first conversion in 2019 are at Vanguard and I do everything online. Vanguard keeps tabs on my annual RMD amount and won’t let me do a Roth Conversion until after I take the total RMD out.

GeneL says

Thank you for this. I’m also at VG. Good to know.

GeezerGeek says

Schwab provides warnings that you have to take the total RMD out before you do a Roth conversion, but they don’t prohibit it because for all they know, you may have satisfied your RMD with a withdrawal from an IRA that is held at another broker. RMDs are not specific to an IRA account. You can take your total RMD for all accounts out of one account and not make any withdrawals in any other IRA account.

RobI says

@GeezerGeek from what I’m reading on IRS web site you cannot combine RMD’s from Different types for retirement account. IRA, 401K and 403B would each have to have their own withdrawal. Do I have this correct?

GeezerGeek says

@Robl, I don’t know what the rules are for 401k and 403B. I rolled my 401k to an IRA so the IRS doesn’t care which IRA I use to take the RMDs. Schwab also only calculates my total RMD and considers it met regardless of what account is used.

Last year, I learned that Schwab can provide checks that you can use for writing QCD checks to charities. That makes QCDs a lot simpler. I got my checks last week.

JoeTaxpayer says

To Geezer Geek,

I saw the note regarding QCD checks. Just got off a chat with Schwab and this was the reply to my request –

“Understood! So if you were to request a checkbook, the checks would be considered a normal distribution- Code 7 and you would want to keep a receipt to properly code the QCD for the tax filing year.

We also have a QCD form that can be filled out so it is coded properly as a QCD and no need for reporting updates come tax filing. This option would require a form each time you want to request a QCD.”

I read that as meaning the IRA checkbook is for any distributions, not just QCD. And a t tax time, I’d be looking at Code 7 on the 1099. I see you just got the checks, so I can’t ask how you reconciled this on the tax return. Just sharing this, and asking if you were aware.

(I need to go back to the tax software and see how simple/tough it is to make the declaration for the partial QCD vs total withdrawal.)

Jeff Enders says

JoeTaxpayer – and note that the new 2026 tax reporting requirements are that firms are to use a code “Y” in box 7 of form 1099-R to indicate a QCD. It was optional in 2025. The purpose is to increase accuracy.

So I suspect it could be challenging to self-report a QCD going forward. The IRS would expect the impact on the tax return to reflect what form 1099-R reports.

GeezerGeek says

@JoeTaxpayer,

I was unaware of the new 1099-R reporting requirements that Jeff Enders provided in his comment. Previously, the only way the IRS knew it was a QCD was that the QCD was reported on line 4 of the 1040, the same line where nontaxable IRA rollovers were reported. I suspect that now with the new code, the QCD will be excluded from the Taxable amount box on the 1099-R, but that may have also been done previously, for all I know.

Writing checks is easier than completing a Schwab form and you get the option to directly hand the check to the charity, so I would much prefer to write checks.

An individual can still perform an indirect rollover (or “60-day rollover”) by having the former custodian issue a check in their name and depositing it into a new IRA within 60 days. That is an analogous situation to the QCD checks because the IRA distribution will be reported on the 1099-R as taxable, since the former IRA custodian has no way of knowing that the amount of the distribution was deposited in an IRA within 60 days.

I’ll research the new 1099-R reporting requirements further, but I sure hope I can use the checks for QCDs without causing problems with the IRS. It may be just like any other charitable gifts you take as tax deductions: you just have to keep records to document it. A canceled check is a pretty solid record.

Jeff Enders says

@GeezerGeek

The point of the reporting requirement is to keep people honest. If the administrator reports $X on form 1099-R, then upon audit, you are going to be pressed to prove that anything above that is truly a QCD. The first question is going to be “why didn’t your adminstrator report it?”

this of the new reporting requirement as independent verification that they money went directly from the Administrator to the charity.

Bob says

Liftlock. I recommend that you type in the question “Can an RMD be done prior to a QCD within the same tax year?” in your browser. The reply basically says that an RMD can be done prior to a QCD in a tax year, but it is generally not advisable if your goal is to use the QCD to satisfy your RMD. The IRS follows a “first-dollars-out” rule: if you take an RMD (or part of it) before doing a QCD, that distribution is taxable, and the subsequent QCD cannot retroactively offset it.

Key Considerations for Timing:

Order Matters: To satisfy your RMD with a QCD and keep the amount tax-free, the QCD must be made before the RMD.

The “First Dollar” Rule: If you take your RMD in February and do a QCD in November, the February RMD is taxable, and the November QCD is merely a tax-free donation that does not lower that year’s taxable RMD income.

Best Practice: Do the QCD early in the year to ensure it counts toward the RMD.

If RMD is Taken First: You can still do a QCD later in the year to reduce your overall tax burden, but you will still pay taxes on the RMD taken earlier.

The Wizard says

Bob is wrong.

Let’s say your total tIRA RMD number for the year is $40,000.

You can do a normal distribution of $33,000 on January 2 of that year, followed by QCDs of $7000 on December 29 of that year and be in absolutely fine shape.

Ignore all comments to the contrary…

Jeff Enders says

Wizard – I do not see that Bob is wrong. Rather, what is occuring is that prior to satisfying an RMD requirement, a distribution can serve 2 purposes: RMD and QCD. After the RMD is satisfied, QCD can’t retroactively satisfy RMD.

Let’s say on January 1, my objective is to provide my favorite charity $10,000 and I have a $50,000 RMD requirement.

1) On January 3, I have the adminstrator send $10,000 to the charity and I distribute an additonial $40,000 from my IRA. My RMD is satisfied! My QCD is satisfied!

2) On January 3 I have the administrator distribute $50,000 to me. RMD satisfied! On January 4, I have the administrator send $10,000 to the charity. Problem! I can’t retroactively adjust the RMD so only $40,000 is taxable! In effect, I’ve distributed $60,000 this year ($50,000 to satify RMD and another $10,000 for QCD, which will reduce my RMDs in future years).

tjk144 says

Jeff Enders – Bob is wrong with his statement that:

Order Matters: To satisfy your RMD with a QCD and keep the amount tax-free, the QCD must be made before the RMD.

Order does not matter and the QCD does not have to be taken before the RMD. All that matters is that the total of the QCD’s and RMD’s satisfies the required RMD.

Bob says

To: Robl. RMD requirements for IRAs and 401(k) plans are separate. While you can aggregate and withdraw the total RMD for multiple IRAs from a single IRA account, you must take RMDs separately from each individual 401(k) account you own.

Richard says

I am an IRS Enrolled Agent, although nothing here should be regarded as professional advice.

(a) As far as RMDs are concerned, each 401(k) is regarded individually, you have to calculate the RMD for every one separately and take the relevant amount from each. IRAs, on the other hand are dealt with in aggregate. You total the amount of the IRAs, calculate the total RMD and as long as you take that amount out it doesn’t matter whether you take it from one IRA or split it between them.

(b) Under the tax code the first withdrawls you take from a traditional IRA are taken as satisfying your RMD. Thus if the first thing you do is a Roth conversion then that is not treated as a conversion but rather as taking the RMD as income and then using that income to make a contribution to your Roth. However as you will not have any earned income to justify a contribution that is treated as an excess contribution and may lead to penalties if not withdrawn.

(c) Similary with QCDs. If the first amounts taken our of the traditional are direct payments to a charity then that is simply taken as saatisfying your RMD and although they are charitable distributions (and can be claimed on Schedule A) they are not *QUALIFYING* charitable distributions, they count as part of your taxable income.

In short the tax code says that if you want to take advantage of any special treatments (like QCD or conversions) you may do so only after you have already taken our your RMD.

It is up to you to sort this out at tax return time since the 1099-R will not always get correctly how much of your total distribution falls into what category.

The Wizard says

So called enrolled agent “Richard” is completely wrong regarding QCDs.

They are NOT treated as taxable income and are NOT claimed on Schedule A.

Cripes…

Richard says

I am not a so called enrolled agent, I am one. You need to read what I said, as I did not say that QCDs are taxable or claimable.

I said that direct payments to charities made before taking out your RMDS are charitable distrubtions but not Qualified Charitable distributions. They are *NOT* QCDs. Since they are not QCDs they are taken as part of your taxable income but may be claimed on schedule A.

I did not go on to say that direct payments to charities made after you have taken out your RMDs may qualify as QCDs because I thought that point obvious. If you do choose to treat them as QCDs then they do not count as part of your taxable income and so cannot take them as a deduction on Schedule A.

tjk00144 says

Richard — Your statement that direct payments to charities made before taking an RMD don’t qualify as a QCD is incorrect. As long as the total of your QCD’s and RMD’s does not exceed the required RMD, the order in which QCD’s and RMD’s are taken is irrelevant. In fact, no RMD even needs to be taken if the QCD satisfies the required RMD.

Mike W says

I have noticed something disturbing over the past number or posts. We seem to be getting comments from ‘experts’ who know many ‘facts’ that are in fact not facts. We also have many of this same ‘experts’ who, given the precision required in understanding anything the Government writes, don’t write clearly or precisely.

We have a simple question just above here. If my RMD is $100k, can I make a QCD for $100k on January 1st and then not have to take any more money out of my IRA? When I say make a QCD I mean tell my Fidelity or Schwab person in charge that I want to make a $100k QCD. The purpose of a QCD, as I understand it, is you would only do one to offset the impact of your RMN on your AGI.

tjk00144 says

Everything that you said is correct. That being said, I always wait until later in the year to decide how much of my RMD to take as a QCD in order to stay under a certain IRMAA tier.

Gary says

Mike W – Two possible expansions on your “purpose of a QCD” sentence: 1) I was taking QCDs after age 70.5 even though my RMDs did not start until age 73 and 2) My understanding is that you can take up to $100K QCD in any year irrespective of your RMD requirement (e.g. you can offset some/all of your RMD, but can also just be charitable and exceed the RMD). So in both of these situations, it can be more than just an RMD strategy, QCDs can more generally be used in a tax advantaged way for your charitable contributions, especially if you are using the standard deduction.

tjk00144 says

What is the point in taking a QCD at age 70.5? The only possible benefits that I can see are: (1) you are lowering the value of your IRA so that RMD’s are lower when you need to start taking them at age 73 and (2) you don’t have the funds in a taxable account and instead distribute them from your IRA. Am I overlooking something?

Gary says

We had historically been doing our charitable donation by giving stock shares to minimize capital gains taxes. When i turned 70.5, the math seemed to say that QCD donations was somewhat more advantageous than stock donations (especially considering potential future stock step up for a surviving spouse or children). We are standard deduction folks, and using after tax funds would not result in a tax deduction for us. However, you are correct that also lowers future RMDs.

tjk00144 says

That makes sense. I hadn’t thought of the advantage in the step up basis for assets in a taxable account vs none in an IRA.

The Wizard says

Doing QCDs prior to age 73 (or 75)has multiple advantages. It lowers your AGI and allows you to do larger Roth conversions for the year before getting into the next higher IRMAA tier…

Gary says

Can you expand on your “lowers your AGI” comment? I thought that the QCD before age 73/75, did not affect AGI. If I remember correctly, I got a 1099 for the amount, but the tax return shows this as non-taxable. So your AGI would be the same that year, whether you do the QCD or not.

Inquiring minds want to know! 😃

Richard says

The age limit for QCDs is 70½ (the original age at which RMDs kicked in). Thus as long as you make the QCD after you have turned 70½ then it does not count as part of your taxable income.

If you are below the age where you have to take RMDs but are over 70½ the only advantage is if it was a charitabale contribution you would have made anyway. If you make the contribution outside of the IRA then your AGI is what is would otherwise be and the only relief you get is if you take itemized deductions (which not a lot of people do) and can claim it on Schedule A. Even if you could go down that route you may be better off taking it as a QCD because your AGI is lower (so helping lower your social security MAGI) and if you are claiming the medical expense deduction the the 7½% threshhold is lower so you can claim a bit more.

The Wizard says

Wait.

I was wrong about that.

Sorry …

Richard says

I was wrong about the QCD treatment. The ordering rule does not apply to them.

tjk00144 says

I still do not understand how taking a QCD at age 70.5 lowers your AGI. Can someone enlighten me.

As I see it, the only way that a QCD lowers your AGI is if it replaces an RMD that would increase your AGI. Since no RMD is necessary at age 70.5, how does taking a QCD at this age lower your AGI?

MTG says

If you do a charitable contribution from a w/d from your IRA, AGI increases. With QCD, it doesn’t.

The Wizard says

Not quite true.

If you’re 71 and want to donate $5000 to a charity, a QCD is definitely better than an after tax donation of the same amount…

tjk00144 says

MTG — Yes, that would be true. Gary stated some good reasons for making a QCD at age 70.5. But other than that, IMO there is no reason to make a non required w/d from an IRA unless you need the funds to live on — certainly not to make a charitable contribution. Let the money grow tax deferred and make the contributions from a taxable account.

Richard says

As long as you are over 70½ you can make a QCD from your IRA even though you do not have to take an RMD. The ress of this discussion assumes you are over 70½ but not yet required to take an RMD.

Now if you are fortunate enough to have enough money not to have to withdraw funds from your IRA and you were not going to make a charitable contribution then there is no benefit of making a contribution just so that it would be a QCD.

If you have enough money not to need to take money from your IRAs but are going to make a charitable contribution anyway the position is more nuanced. You have the choice (assuming you are over 70½) of making the charitable contribution out of your other funds or directly from the IRA so that it can be a QCD. By making the contribution directly (a QCD) and reducing that amount that you would otherwise pay yourself from the IRA then your AGI would go down because the amount taken out as a QCD will not count towards your taxable income.

tjk00144 says

Richard — you are talking in circles. First of all, you say that if you have enough money so that you don’t need to make contribution from an IRA …… Then shortly after that, “reducing that amount that you would otherwise pay yourself from the IRA”.

If you don’t need to make a contribution from an IRA because you have sufficient outside funds, then you are not going to pay yourself from the IRA.

MTG says

wizard’s comment does not make my comment untrue. It does show the true benefit of a QCD though.

MTG says

tjk00144

I agree an IRA w/d just for a charitable contribution would not be a great plan. The non-required IRA w/d is a totally diffent conversation. QCD for the win!

tjk00144 says

Wizard — Why is making a $5,000 donation to a charity at age 71 using a QCD better than making the same donation from a taxable account? The reasons that Gary gave made sense but other than those, I can’t think of any others. I would prefer to let the $5,000 grow tax deferred in my IRA and make the donation from a taxable account.

Gary says

I guess this is a matter of perspective. For us, we start the year with say a $1K budget for charitable giving. We also know that we will be using the standard deduction on our tax return. So our hierarchical thinking for optimal giving is as follows:

1) After Tax Cash/Check – We feel good giving the $1K, but there is no tax return benefit because our AGI is unaffected with the same standard deduction. If some of you could itemize, then the $1K would reduce taxes.

2) Stock Donation – We have long term stocks with 80% of their current value being unrealized capital gains. Donating $1K of stock, does not change our AGI, nor our standard deduction. So no tax benefit on this year’s return. However, it avoids future capital gains by $800.

3) QCD – We donate $1K directly from our IRA. No change to AGI or our standard deduction, so no tax benefit this year. However, we reduce future RMDs by $1K. Our own analysis says this is slightly better than option 2, because RMDs are ordinary income versus capital gains rates.

If you are wondering about the lost future deferred capital gains (opt 2) or IRA income (opt 3), remember you would still have $1K after tax cash. Buy some new stock or an iBond, to start a new deferral clock.

Hope I wrote this clearly and that it helps someone. 😃

Richard says

tjk00144

In all cases you are over 70½ but not old enought to have to take RMDs. Take 4 different Situations.

(a) you have enough income not to need to take money from the IRA to live on

and do not intend to give to your church or any other charity.

There is no point in no point in making a QCD just for the sake of making a QCD.

(b) You have enough income not to need to take money from the IRA to live on

but do intend to give to your church or another other charity.

You might want to make the contribution from your IRA or you might want to make

it from your other income. In either case your AGI would be the same. If you take

it from the IRA as a QCD then your AGI would be unaffected. If you itemize and do

not take it from the IRA then you get to take it as a deduction. Not taking it as

a QCD would make the most sense.

(c) You do not have enough income to live without taking money from your IRA and you

do not intend to give to your church or any other charity.

There is no point in no point in making a QCD just for the sake of making a QCD.

(d) You do not have enough income to live without taking money from your IRA and you

do intend to give to your church or an other charity.

If you would normally transfer say $1,000 month from your IRA to your bank account

and you intend to give say $700 to a charity then it makes sense that for one month

you transfer only $300 to your bank account and have the IRA send $700 to the

charity as a QCD

I hope this clarifies things.

Jim M says

Also consider those with inherited IRAs who are non-spouse beneficiaries. Using QCDs in place of mandatory RMDs within the 10 year distribution period is a great tax avoidance option.

Joe Taxpayer says

I like this list, it would make a great infographic/flowchart.

And I’ll just agree, if one isn’t planning to donate to charity, they should just move on, the QCD doesn’t apply to them.

For (b) if one is taking RMDs, doesn’t the QCD help reduce AGI triggering IRMAA? Taxable line doesn’t change, but AGI line to determine IRMAA does. If not near a threshold, this is moot. But we all talk about conversions, and while on medicare I’m thinking that’s what many here are doing. (To be clear, I agree you addressed the tax issue 100% right. I’m just looking at the IRMAA effect.)

Stevea says

Good thoughts, but a couple details. The QCD (as you know) does not impact your taxes at all, but it does count as an RMD (if/when required).

For charitable giving of anything after-tax, you need to consider that there is now a 0.5% of AGI reduction in deductibility of the gift. To evaluate “saving” of an appreciated after-tax asset , you need to consider your marginal tax rate (same as ordinary income for ST.cap.gains, but 0%, 15%, 18.8% or 23.8% for LT.cap.gain), but consider that your heirs can inherit the after-tax asset at 0% tax (step up in basis). Then you get a deduction for the full value minus 0.5% of AGI *if* you itemize. Also the deduction may be reduced or eliminated by AMT.

So generally if >70.5yo, the QCD is advantageous unless you have a very high tax bracket, intend a large gift (>>0.5% of AGI) and already itemize.

Heads-up for those interested in giving, in 2027 there will ba a $1.7k/person Federal Scholarship Tax Credit. IOW you give $1.7/person to a qualifying K-12 school and you get the same $1.7k off your taxes!

Jeff Enders says

StevenA:

<>

Lots of rules: it is NOT a qualifying K-12 school. It’s donations to “Scholarship Granting Organizations” (SCOs).

Credit Amount: Individuals can receive a nonrefundable, dollar-for-dollar tax credit up to $1,700 for donations to SGOs.

SGO Requirements: SGOs must be 501(c)(3) nonprofits, certified by a state, and spend at least 90% of their revenue on scholarships.

Student Eligibility: Generally, students must be eligible for public K-12 enrollment and live in households not exceeding 300% of their area’s median income.

State Participation: States must opt into the program by providing a list of approved SGOs to the IRS.

Donations and Benefits

No Earmarking: Donors cannot specify which students receive scholarships.

Double Benefit Restriction: Taxpayers cannot claim both the federal credit and a state-level tax credit for the same donation.

Educational Use: Funds are used for tuition, fees, tutoring, special needs services, books, and technology.

Public School Funding: The program is designed to operate independently, with proponents stating it does not reduce public school funding.

Mike W says

Gary,

2) Stock Donation – We have long term stocks with 80% of their current value being unrealized capital gains. Donating $1K of stock, does not change our AGI, nor our standard deduction. So no tax benefit on this year’s return. However, it avoids future capital gains by $800.

You paid $200 for the stock so your $1,000 contribution only cost $200. But you only save 24% or so on that $800 depending on your tax bracket.

3) QCD – We donate $1K directly from our IRA. No change to AGI or our standard deduction, so no tax benefit this year. However, we reduce future RMDs by $1K. Our own analysis says this is slightly better than option 2, because RMDs are ordinary income versus capital gains rates.

You do not reduce RMD by $1000, Assuming you are 75 years old you only reduce the RMD by $43.66 ($1000/22.9 = $43.66). If you have $1000 less in your IRA then when you divide by your age divisor your RMD will be less. By the way, if you did want your RMD to be $1,000 less you would need your IRA to end the year with $22,900 less.

Gary says

Mike W

2) Stock Donation – I think you are estimating the amount of saving, but my point was that it was still better than option 1.

3) QCD – my “future RMDs” referred to all future years (i.e. the $1K comes out of the IRA sooner or later). There is a time value of money affect, but that is also true for the stock donation option (ignoring the step up possibility). Our analysis of the two options contemplated time value and option 3 was still better.

Mike W says

Gary,

I was being too precise on the explanation. I agree with your analysis of the options and how they compared to each other.

James says

Does IRMAA apply to Medicare Advantage?

I apologize if this has already been asked and answered.

Harry Sit says

It does. Otherwise it would be too easy to escape the higher charges.

Bob says

Good point re the distribution code for a QCD on the 1099-R. Code 7 on the 1099-R is a normal (taxable) distribution. Code Y is for a QCD. I recommend that the taxpayer who does a QCD contact the financial institution towards the end of the year to ensure that they indicate a Y distribution for a QCD that will be issued by late January. Box 4(b)(2) on the 1040 return is to indicate a QCD and 4(b)(3) is to indicate the QCD $ amount. This should be done whether or not the financial institution shows a Y code on the 1099-R.

LiftLock says

I suspect most IRA custodians will have difficulty identifying QCD distributions so that they can be reported with a distribution code Y on the 1099-R. For the 2026 tax year, the horse is already out of the barn.

Jeff Enders says

LIftlock – Nope. not out of the barn. The code was optional reporting in 2025 and mandatory reporting in 2026. Administrations were given over a year to put processes in place to correctly report payments they were directed to make by the IRA account owner. The Administrator has to presume the recipient is a charitable organization.

The taxpayer is still the party that has to prove that the receiver was in fact a qualified charity. That is documented by any receipt by the charity of over $250 requires them to send you a letter so indicating the amount they received and that they qualify as a charity under IRS rules. Whether the source is from an IRA, your after tax funds that you deduct on Sch A or the new $1,000 charitable cash donation available to those that do not itemize, that letter from the charity is required for any donation over $250.

Liftlock says

Jeff Enders,

From my perspective the horse has left the barn. In the fall of 2025 the IRS announced that it would not require IRA custodians to use of Distribution Code Y when filing 1099-R’s for 2025. I believe they got feedback from IRA custodians indicating they could not meet that deadline for another 12-18 months.

We are now in May 2026 and I can’t find an announcement from the IRS since last fall updating their position for 2026. In the meantime, taxpayers have making CDS since January 1 with some (many?) brokers not having implemented processes or procedures to identify QCDs as they occur so that they can be completely and accurately reported using Code Y on 1099-Rs for 2026. This is likely to be a significant challenge for IRA custodians to retroactively address.

Fidelity, is an example of one IRA custodian issued who has not issued processes or procedures for taxpayers to follow to ensure that QCDs can be accurately reported on a 1099-R for 2026. I suspect Fidelity is not the only IRA custodian in the same position. It is wishful thinking to believe that an IRA custodian will be able to successfully identify QCDs retroactively back to Jan 1 once new procedures are in place.

My best guess is that 2026 will end up being another transition year for use of code Y. QDS reported using Code Y may or may to not be complete and accurate for 2026. Some Taxpayer’s may have to report QCDs on their tax return that do not match what is reported using Code Y.

The Wizard says

For another data point on QCD implementation, I’ll mention that Vanguard formerly allowed check writing on my tIRA. I used that for QCDs in 2024 and early 2025. But they discontinued honoring those checks last summer.

To do a QCD at Vanguard now, I log into their website and get to their QCD page where I type in the charity’s name and the dollar amount. They then mail that check to me and I hand deliver or mail it to the charity.

The charity should then send you a proper acknowledgement letter for your tax folder. There’s no cancelled check involved for your records

The IRS is setting up a boondoggle with this new Y code since custodians are not responsible for determining if the recipient of a supposed QCD check is in fact a qualified charity…

The Wizard says

Also, when using the current QCD method at Vanguard, the QCD dollar amount is immediately subtracted from my tIRA settlement fund, like a certified check. There’s no waiting for the check to “clear” before debiting the funds.

The general recommendation for QCDs has been: don’t wait till late December to do one. But it doesn’t matter with Vanguard now. I could initiate a QCD on 12/31 and I’m reasonably sure it will get reported as a distribution for that year. But I’m not planning to verify that assertion…

Bob says

Correct. It’s the IRA owner’s responsibility to confirm the charity is a 501(c)(3) organization eligible to receive tax-deductible contributions, such as by using the IRS Tax Exempt Organization Search tool. The financial institution’s role is to ensure the check is made payable directly to the charity, not to the IRA owner. Starting with 2025 distributions (reported in 2026), the IRS introduced an optional Code Y for Form 1099-R to help identify QCDs, but the institution still does not verify the charity’s status.

The donor must obtain a written acknowledgment from the charity for their tax records.

This is why I indicated in my previous comment this morning for the taxpayer to check box 4(b)(2) on the 1040 tax return to indicate the QCD and show the QCD $ amount in box 4(b)(3). Then indicate the net $ taxable amount (i.e., IRA distribution minus the QCD amount) on line 4b (column) on the 1040 return. I believe this should be done whether or not the 1099-R shows a “7” or a “Y” in box 7 of the 1099-R.

Jeff Enders says

Wizard – no boondoggle. Similar to any other charitable contribution that exceeds $250, the non-profit organization must send a letter to the tax payer indicating they are a qualifying organization and detail the amount of the contribution.

The burden remains on the taxpayer that the recipient meets the IRS requirements for the donation.

Jeff Enders says

Bob

<>

Why would you do this? the IRS is receiving evidence from the Adminstrator that the money was sent directly to an organization (presumably charitable) and not to the IRA account holder. Why override that information? It’s asking for trouble.

For 2025, use of the “Y” code was optional, but for 2026 it is an IRS requirement. Administations have had 18 months to develop processes to report accurately.

The Wizard says

I agree with liftlock.

This is why I call the whole Code Y thing an IRS boondoggle…

John J Fitzsimons says

A few comments:

1. I wouldn’t wait until the year end market open date to initiate a QCD. A Vanguard rep told me it should in by 3pm on the second to last day.

2. Regarding Bob’s comments: If you are referring to the 1040 for tax year 2025, there are no boxes 4(b)2 and 4(b)3. Perhaps you meant 4(c)2 and 4(c)3. Regardless, you do not put the QCD amount in box 3 and only check box 2 if you did make a QCD(s) in 2025. Box 3 only comes into play if the distribution is a HSA funding distribution (HFD). It can actually get a little more complicated (naturally ) when you delve into the details. See pages 26-28 of the 2025 1040 instructions.

3. One last thing. We had 1099-Rs from both Fidelity and Vanguard for 2025 with distribution code 7. Neither brokerage treated them any differently than 2024 1099-Rs with the exception of adding code “Y” to the back of the 1099.

The Wizard says

I just checked the 1099-R for my Vanguard tIRA for last year. I did five or six QCDs in 2025 including two in November using their new system.

Same as John J, my 1099-R was code 7 with Taxable Amount Not Determined checked.

So basically, custodians are ignoring the new Y code and playing it safe by putting the “burden” on the taxpayer to verify the QCD claims, if audited. This is how it should be…

Bob says

John. Let me clarify line 4 for the 2025 1040 return. There are several parts to line 4. 4a represents the IRA gross distribution amount. 4b represents the net taxable amount of the distribution in the column itself. 4c shows 3 items: (a) the 4(c)(1) checkbox if it’s a tax-free rollover, (b) the 4(c)(2) checkbox if there is a QCD, and (c) the 4(c)(3) line for the QCD $ amount as well as the tax-free rollover $ amount (if any).

Therefore, if there is a QCD to a qualified 501(c)(3) organization, the taxpayer would: (a) enter the full IRA distribution in box 4a, (b) check the QCD box in 4(c)(2), (c) enter the QCD $ amount in 4(c)(3), and (d) enter the net taxable amount (i.e., total gross amount in 4a minus the QCD amount in 4(c)(3)) on line 4b in the column.

If the taxpayer also did a tax-free rollover, then box 4(c)(1) is checked and the associated $ amount is included in box 4(c)(3). Therefore, if the taxpayer has both a QCD and a tax-free rollover, those amounts are combined for 4(c)(3) and reflected in the net taxable amount in line 4b.

Jeff Enders says

John:

<>

in 2025, the use of the “Y” code was optional; in 2026 it is a requirement.